También podría gustarte

- MF0979_2 - Gestión operativa de tesoreríaDe EverandMF0979_2 - Gestión operativa de tesoreríaCalificación: 5 de 5 estrellas5/5 (1)

- Corralito Argentina 2001Documento9 páginasCorralito Argentina 2001Mente Millonaria lifeAún no hay calificaciones

- FOPA y Caso BancaféDocumento5 páginasFOPA y Caso BancaféPaolaMadridAún no hay calificaciones

- Baninter y Crisis Bancaria 2003, Rep DomDocumento7 páginasBaninter y Crisis Bancaria 2003, Rep DomKatherina EncarnacionAún no hay calificaciones

- Normas Generales TesoreriaDocumento23 páginasNormas Generales TesoreriaAlejandro Ortegon100% (1)

- Contabilidad de Entidades Financieras IIDocumento22 páginasContabilidad de Entidades Financieras IIChallabambinoDeCorazonAún no hay calificaciones

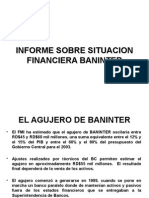

- BaninterDocumento37 páginasBaninterelduritoquiroAún no hay calificaciones

- Los fondos buitres, capitalismo depredador: Negocios y litigios financieros: de Argentina a GreciaDe EverandLos fondos buitres, capitalismo depredador: Negocios y litigios financieros: de Argentina a GreciaAún no hay calificaciones

- Baninter y Crisis Bancaria 2003Documento6 páginasBaninter y Crisis Bancaria 2003Katherina EncarnacionAún no hay calificaciones

- Por qué quebraron los bancos mexicanos y se creó el FobaproaDocumento5 páginasPor qué quebraron los bancos mexicanos y se creó el FobaproaVictor Santiago Martínez100% (1)

- Consideraciones para el cierre de estados financieros, de acuerdo con las Normas de Información Financiera mexicanas (NIF).: Contiene el impacto de la pandemia de coronavirus (COVID-19)De EverandConsideraciones para el cierre de estados financieros, de acuerdo con las Normas de Información Financiera mexicanas (NIF).: Contiene el impacto de la pandemia de coronavirus (COVID-19)Aún no hay calificaciones

- Proyecto de Aplicacion Mercado de CapitalesDocumento5 páginasProyecto de Aplicacion Mercado de CapitalesOmaira Beltran100% (1)

- Historia de La Regulación y Supervisión Financiera en Bolivia - TOMO IIDocumento169 páginasHistoria de La Regulación y Supervisión Financiera en Bolivia - TOMO IIMinisterio de Economía y Finanzas Públicas de Bolivia100% (1)

- Evaluación Parcial DF 2020-2Documento7 páginasEvaluación Parcial DF 2020-2Daniela RodriguezAún no hay calificaciones

- Nacionalización de la banca en México durante la crisis de 1982Documento3 páginasNacionalización de la banca en México durante la crisis de 1982EDGAR RUBEN CASTROAún no hay calificaciones

- Bancoldex2005 BancosDocumento31 páginasBancoldex2005 BancosElizabeth ChauccaAún no hay calificaciones

- DT Deudas y Contingencias Del EstadoDocumento122 páginasDT Deudas y Contingencias Del EstadoERIKA LUCERO TUNQUI TICONAAún no hay calificaciones

- Delitos Economicos y FinanciaerosDocumento42 páginasDelitos Economicos y FinanciaerosPERUHACKING100% (2)

- Crisis Bancaria en NicaraguaDocumento6 páginasCrisis Bancaria en NicaraguaMayraAún no hay calificaciones

- Historia y quiebra del Banco Banex en PerúDocumento15 páginasHistoria y quiebra del Banco Banex en PerúMelissaAún no hay calificaciones

- Informe en PDF de Los Peritos Del Banco de España Sobre Bankia (II)Documento212 páginasInforme en PDF de Los Peritos Del Banco de España Sobre Bankia (II)infoLibreAún no hay calificaciones

- Notas A Los EEFF 3T21Documento18 páginasNotas A Los EEFF 3T21P CentrixAún no hay calificaciones

- LECTURA 2 (C) Multa NavarreteDocumento222 páginasLECTURA 2 (C) Multa NavarreteAlejandra JimenezAún no hay calificaciones

- El Banco Latino Ó Porque Están Investigados en La Fiscalía, Fritz Du Bois y Cayetana Aljovín (PUBLICADO Hoy Viernes 16 de Noviembre en "En Sus Trece")Documento8 páginasEl Banco Latino Ó Porque Están Investigados en La Fiscalía, Fritz Du Bois y Cayetana Aljovín (PUBLICADO Hoy Viernes 16 de Noviembre en "En Sus Trece")paracaAún no hay calificaciones

- Carta de TiripishiriDocumento5 páginasCarta de TiripishiriHansth T. ArenasAún no hay calificaciones

- Fallo histórico sobre la deuda externa argentinaDocumento112 páginasFallo histórico sobre la deuda externa argentinacayu8138Aún no hay calificaciones

- Análisis jurisprudencial sobre el FOMEDocumento7 páginasAnálisis jurisprudencial sobre el FOMEPaola Andrea ArdilaAún no hay calificaciones

- DS 006 2002Documento8 páginasDS 006 2002BaltazarAún no hay calificaciones

- Carta de La Caja Metropolitana A Programa PanoramaDocumento3 páginasCarta de La Caja Metropolitana A Programa PanoramaLima Mml100% (1)

- P. Del S. 1144: Gobierno de Puerto RicoDocumento125 páginasP. Del S. 1144: Gobierno de Puerto RicoRubén E. Morales RiveraAún no hay calificaciones

- Fondo Bancario de Protección Al Ahorro (FOBAPROA)Documento5 páginasFondo Bancario de Protección Al Ahorro (FOBAPROA)MiiriiamGallegosAún no hay calificaciones

- Pumem 201012 91755000 20110421 160933Documento214 páginasPumem 201012 91755000 20110421 160933Carlos Ignacio CidAún no hay calificaciones

- PIF - DE - ESTADOS - FINANCIEROS - Niff 7Documento21 páginasPIF - DE - ESTADOS - FINANCIEROS - Niff 7Jorge HernandezAún no hay calificaciones

- Regreso al endeudamiento externo: análisis de la deuda pública argentinaDocumento37 páginasRegreso al endeudamiento externo: análisis de la deuda pública argentinaAgustin RodriguezAún no hay calificaciones

- Liquidacion Banco Continental Grupo 2Documento11 páginasLiquidacion Banco Continental Grupo 2Yenis ArgeñalAún no hay calificaciones

- Historia y funciones del Banco Central de Reserva del PerúDocumento9 páginasHistoria y funciones del Banco Central de Reserva del PerúXxcarlinxXAún no hay calificaciones

- Estudio de La Ley Bancaria en GuatemalaDocumento5 páginasEstudio de La Ley Bancaria en GuatemalaomancillaAún no hay calificaciones

- Banco de La NaciónDocumento32 páginasBanco de La NaciónGrazie del CarmenAún no hay calificaciones

- AUDITORÍA, BANCARIA, GUBERNAMENTAL Y PRÁCTICA SUPERVISADA Nelson Asig CastroDocumento6 páginasAUDITORÍA, BANCARIA, GUBERNAMENTAL Y PRÁCTICA SUPERVISADA Nelson Asig CastroMynor Leal GarciaAún no hay calificaciones

- DocDocumento2 páginasDocHernan Huaman VenturaAún no hay calificaciones

- Contabilidad BancariaDocumento26 páginasContabilidad BancariaEliu MendozaAún no hay calificaciones

- Gestión Del Sistema Financiero PeruanoDocumento12 páginasGestión Del Sistema Financiero PeruanoRick LópezAún no hay calificaciones

- Ley VII N11 LeyContabilidadDocumento29 páginasLey VII N11 LeyContabilidadCr. Santiago PalomarAún no hay calificaciones

- Memoria BCRP 1930Documento18 páginasMemoria BCRP 1930Percy MesccoAún no hay calificaciones

- Historia del sistema financiero colombianoDocumento5 páginasHistoria del sistema financiero colombianoJulio Javier Chima MaestreAún no hay calificaciones

- Normas TesoreriaDocumento15 páginasNormas TesoreriaRoloAún no hay calificaciones

- Semana 18 (2)Documento36 páginasSemana 18 (2)Ibling MarinoAún no hay calificaciones

- Actividad de Aprendizaje LuzDocumento21 páginasActividad de Aprendizaje LuzLucy SánchezAún no hay calificaciones

- 4857750-memoria-anual-fcr-2022(2)Documento55 páginas4857750-memoria-anual-fcr-2022(2)rtinocorAún no hay calificaciones

- MpaDocumento5 páginasMpaEduard SaavAún no hay calificaciones

- Entrega 1 Contabilidad de ActivosDocumento16 páginasEntrega 1 Contabilidad de Activoszamir2683Aún no hay calificaciones

- Trabajo de Inv. FByBVDocumento11 páginasTrabajo de Inv. FByBVFRANCO MONTENEGROAún no hay calificaciones

- Banco Territorial ExpoDocumento35 páginasBanco Territorial ExpoestefanialilibethperezalavaAún no hay calificaciones

- Subsector Financiero en Colombia - GestioPolisDocumento12 páginasSubsector Financiero en Colombia - GestioPolisLauraLorenaMarentesAún no hay calificaciones

- Banco Territorial ExpoDocumento35 páginasBanco Territorial ExpoDiego SalasAún no hay calificaciones

- Cartera Recomendada Marzo - Reafirma Ausol - 13032024Documento27 páginasCartera Recomendada Marzo - Reafirma Ausol - 13032024roviruzAún no hay calificaciones

- Impacto de la NIC 7 en el sector financiero colombianoDocumento25 páginasImpacto de la NIC 7 en el sector financiero colombianoCarmen Elisa Moreno CasallasAún no hay calificaciones

- INFORME ANUAL FLPYS 2021 Aprobado COSEDEDocumento15 páginasINFORME ANUAL FLPYS 2021 Aprobado COSEDEFreddyAún no hay calificaciones

- TrabajoDocumento12 páginasTrabajoEder DHAún no hay calificaciones

- NIIF 7, NIC 32 y NIC 39. Asuntos de Conversion A NIIF, InformeDocumento17 páginasNIIF 7, NIC 32 y NIC 39. Asuntos de Conversion A NIIF, InformeJesús Izquierdo DíazAún no hay calificaciones

- Guia 001 (Borrador)Documento6 páginasGuia 001 (Borrador)Nohelia PadillaAún no hay calificaciones

- Ejercicio Contabilidad Doctora NormaDocumento38 páginasEjercicio Contabilidad Doctora NormaNathalia Hernandez PulidoAún no hay calificaciones

- Caso Comportamiento de Los CostosDocumento14 páginasCaso Comportamiento de Los CostosAnita Perleche SampenAún no hay calificaciones

- ACTIVIDAD MERCANTIL-Legislacion-Grupo 4 (5)Documento7 páginasACTIVIDAD MERCANTIL-Legislacion-Grupo 4 (5)Estrella SanchezAún no hay calificaciones

- Productos Financieros de PasivoDocumento9 páginasProductos Financieros de PasivoAsunción CordónAún no hay calificaciones

- Crecimiento Económico, Desarrollo Económico y Desarrollo SostenibleDocumento27 páginasCrecimiento Económico, Desarrollo Económico y Desarrollo SostenibleCesar Augusto GAMIO MALDONADOAún no hay calificaciones

- Analisis de Precios Unitarios ApuDocumento5 páginasAnalisis de Precios Unitarios ApuBrandTeoAún no hay calificaciones

- Trabajo5 Economia LaionDocumento6 páginasTrabajo5 Economia LaionJordy RojasAún no hay calificaciones

- Administración de inventarios: Modelos de repartidor de periódicos e inventario baseDocumento17 páginasAdministración de inventarios: Modelos de repartidor de periódicos e inventario baselinacadena2594Aún no hay calificaciones

- 1002Documento1 página1002Sallua Yorgely ESTEBAN RINCONAún no hay calificaciones

- Legajo de Programacion - Seccion PermanenteDocumento140 páginasLegajo de Programacion - Seccion Permanentemaribel apaza balceraAún no hay calificaciones

- Ejercicios de Estados de ResultadosDocumento3 páginasEjercicios de Estados de ResultadosDICQAún no hay calificaciones

- Caso Practico Metodologia de Las Ochos Diciplinas 8D'S.Documento12 páginasCaso Practico Metodologia de Las Ochos Diciplinas 8D'S.LUIS ANTONIO MARTINEZ REYESAún no hay calificaciones

- Caso ZenonDocumento6 páginasCaso ZenonAbi U0% (1)

- Infografia SocialesDocumento3 páginasInfografia SocialesCarolina GómezAún no hay calificaciones

- Función BuscarV-BuscarHDocumento12 páginasFunción BuscarV-BuscarHLoraine Stefanny MolinaAún no hay calificaciones

- Qué es Aspel, la paquetería líder en MéxicoDocumento4 páginasQué es Aspel, la paquetería líder en Méxicosakura hanuroAún no hay calificaciones

- Linea Del TiempoDocumento1 páginaLinea Del TiempoDonas FrescasAún no hay calificaciones

- Guía para solicitud de código de cliente minoristaDocumento7 páginasGuía para solicitud de código de cliente minoristamerlys muñozAún no hay calificaciones

- Control Interno en El Sector HoteleroDocumento52 páginasControl Interno en El Sector HoteleroCésar Sánchez RoblesAún no hay calificaciones

- El Arancel AduaneroDocumento3 páginasEl Arancel AduaneroEstela BarretoAún no hay calificaciones

- PLANTILLADocumento4 páginasPLANTILLAjeanpier lopezAún no hay calificaciones

- HectorCobos - Tarea 2Documento11 páginasHectorCobos - Tarea 2anbago123Aún no hay calificaciones

- Flujo de FondoDocumento8 páginasFlujo de FondoHector HidalgoAún no hay calificaciones

- Cuadro Crisis 29Documento2 páginasCuadro Crisis 29FRANCISCO CADIZAún no hay calificaciones

- CONCEPTOS SEGÚN Harrington EmersonDocumento6 páginasCONCEPTOS SEGÚN Harrington EmersonCATHERINE ACOSTA CASTELLANOSAún no hay calificaciones

- Factura Debito ECOGAS Nro 0400 44809144 000021175287 CenDocumento1 páginaFactura Debito ECOGAS Nro 0400 44809144 000021175287 CendanielstrubbiaAún no hay calificaciones

- Evaluación Económica Propuestas Inversión PDVSADocumento4 páginasEvaluación Económica Propuestas Inversión PDVSAOmar GraterolAún no hay calificaciones

- ActividadDocumento10 páginasActividadzuleima guarin salazarAún no hay calificaciones