También podría gustarte

- Taller de prácticas fiscales 2016: ISR, IVA, IMSS, INFONAVITDe EverandTaller de prácticas fiscales 2016: ISR, IVA, IMSS, INFONAVITCalificación: 4.5 de 5 estrellas4.5/5 (3)

- Taller de prácticas Fiscales 2022: ISR, IVA, IMSS, InfonavitDe EverandTaller de prácticas Fiscales 2022: ISR, IVA, IMSS, InfonavitAún no hay calificaciones

- Anexo 15 Formato Rendicion Tecnica Financiera IFI Impacto EstrategicoDocumento11 páginasAnexo 15 Formato Rendicion Tecnica Financiera IFI Impacto EstrategicoLasbandurriasAún no hay calificaciones

- Administracion PresupuestariaDocumento27 páginasAdministracion PresupuestariajuanapilarAún no hay calificaciones

- Tema 4 Ingresos, Gastos y ResultadoDocumento21 páginasTema 4 Ingresos, Gastos y ResultadomonicaborrallopAún no hay calificaciones

- FinanzasDocumento5 páginasFinanzasNicely Carrero MontenegroAún no hay calificaciones

- DecmultDocumento6 páginasDecmulteduardoesquivelAún no hay calificaciones

- Wuolah Free Tema 3 y 4Documento277 páginasWuolah Free Tema 3 y 4anAún no hay calificaciones

- Balance GeneralDocumento1 páginaBalance GeneralMiguel Orlando IrahetaAún no hay calificaciones

- Decisiones FinancierasDocumento4 páginasDecisiones Financierasjulian castañoAún no hay calificaciones

- Soluciones TP Cuentas FiscalesDocumento71 páginasSoluciones TP Cuentas FiscalesTomás GimenezAún no hay calificaciones

- Tema 4Documento10 páginasTema 4Borja lopez ruizAún no hay calificaciones

- 01 NIF Postulados BasicosDocumento1 página01 NIF Postulados BasicosHabib HernándezAún no hay calificaciones

- Tema 4 EvDocumento42 páginasTema 4 EvPaula García GilAún no hay calificaciones

- Eeff - Casuistica Nic NiifDocumento5 páginasEeff - Casuistica Nic NiifLinda Garcia MejiaAún no hay calificaciones

- Balance General en EXCELDocumento2 páginasBalance General en EXCELANDRESAún no hay calificaciones

- Formato Del IsrDocumento5 páginasFormato Del IsrKimkum YumAún no hay calificaciones

- Flujo de CajaDocumento22 páginasFlujo de CajaYesenia Aldave MoraAún no hay calificaciones

- Formulación y Evaluación Presupuestal S-11 PREG - UTP-2024-1 - CDocumento16 páginasFormulación y Evaluación Presupuestal S-11 PREG - UTP-2024-1 - CpriscilaalaniayupariAún no hay calificaciones

- Tarea 08 Formato Pagos Provisionales ISRDocumento2 páginasTarea 08 Formato Pagos Provisionales ISRJose LavanaAún no hay calificaciones

- Evaluación Estado de Situacion FinancieraDocumento3 páginasEvaluación Estado de Situacion FinancieraANGIE NATALIA BENITEZ ALVARADOAún no hay calificaciones

- 23-24 Tema 4.1 DficoDocumento21 páginas23-24 Tema 4.1 DficoNoelia Medina OrtizAún no hay calificaciones

- Clase 5 T ASA DE COSTO DE CAPITALDocumento28 páginasClase 5 T ASA DE COSTO DE CAPITALDylan HirakAún no hay calificaciones

- Análisis de BalancesDocumento5 páginasAnálisis de BalancesJavier141075Aún no hay calificaciones

- Formato CGDC N°018 - PacDocumento1 páginaFormato CGDC N°018 - PacmasterAún no hay calificaciones

- Plan de Cuentas (Cuentas de Balance)Documento1 páginaPlan de Cuentas (Cuentas de Balance)Gladis GutiérrezAún no hay calificaciones

- Empresas InmobiliariaDocumento37 páginasEmpresas InmobiliariaArquivanna GrupoAún no hay calificaciones

- Mapeo Vbles P1Documento10 páginasMapeo Vbles P1Luz JanethAún no hay calificaciones

- Plan Contable Gubernamental 2018Documento74 páginasPlan Contable Gubernamental 2018EMILIO AUGUSTO PALACIOS MARTINEZAún no hay calificaciones

- Siaf RPDocumento10 páginasSiaf RPSegundo Manuel Diaz VasquezAún no hay calificaciones

- Determinacion de Coeficiente Se UtilidadDocumento28 páginasDeterminacion de Coeficiente Se UtilidadAlan PolvonAún no hay calificaciones

- Haciendo El FEAIDocumento5 páginasHaciendo El FEAIAntonio Domínguez CarrascoAún no hay calificaciones

- Grupo 8 y 9 InefaDocumento53 páginasGrupo 8 y 9 InefaSabina QuintoAún no hay calificaciones

- Estado Patrimonial ProyectadoDocumento2 páginasEstado Patrimonial ProyectadoArnaldo GarinAún no hay calificaciones

- FORMATO 7 - Deter MODLODocumento10 páginasFORMATO 7 - Deter MODLOSharay SaavedraAún no hay calificaciones

- Contabilidad General TareasDocumento31 páginasContabilidad General TareasKelly Baidal SantosAún no hay calificaciones

- Tema 2Documento24 páginasTema 2Lisbeth Eunice EncarnaciónAún no hay calificaciones

- UntitledDocumento3 páginasUntitledJonathan RiveraAún no hay calificaciones

- Presupuesto Gastos Indirectos de Fabricación: Técnica PresupuestalDocumento13 páginasPresupuesto Gastos Indirectos de Fabricación: Técnica PresupuestalJhadira Lucia Orbezo QuijadaAún no hay calificaciones

- Balance General de La PrimaveraDocumento6 páginasBalance General de La PrimaveraHeydi VásquezAún no hay calificaciones

- Balance General en EXCELDocumento2 páginasBalance General en EXCELGLORIA MOYA VASQUEZAún no hay calificaciones

- Monografía Desarrollada de Contabilidad Gubernamental Iuigv 2018-1Documento44 páginasMonografía Desarrollada de Contabilidad Gubernamental Iuigv 2018-1Wendy100% (2)

- Laboratorio No. 1Documento7 páginasLaboratorio No. 1HORNOS EQUIPOSAún no hay calificaciones

- Esan - DIGEC - Análisis y Estimación de Costos - Ses. 3ADocumento35 páginasEsan - DIGEC - Análisis y Estimación de Costos - Ses. 3AFrank RuedaAún no hay calificaciones

- Informe Actividad 10Documento7 páginasInforme Actividad 10Zharick BerruecosAún no hay calificaciones

- Diapositiva N 05 Ejecucion Presupuestal Cpc. Jobvito Flores MarinosDocumento38 páginasDiapositiva N 05 Ejecucion Presupuestal Cpc. Jobvito Flores MarinosMagaly Del Carpio HuarcayaAún no hay calificaciones

- Condori Maria Gabriela TP #2Documento2 páginasCondori Maria Gabriela TP #2Gabriela CondoriAún no hay calificaciones

- Tasa Costo Capital Patrimonial y WACC 1 498072Documento5 páginasTasa Costo Capital Patrimonial y WACC 1 498072Francisca Lopez ValdebenitoAún no hay calificaciones

- 2-El Sistema de Presupuesto en El SiafDocumento19 páginas2-El Sistema de Presupuesto en El SiafHELFER BAUTISTA ALARCONAún no hay calificaciones

- Balance GeneralDocumento2 páginasBalance Generalk7hw8hkhmrAún no hay calificaciones

- Estado de Situación FinancieraDocumento10 páginasEstado de Situación FinancierarodolfoAún no hay calificaciones

- Ejercicio de CostosDocumento7 páginasEjercicio de CostosLUISA FERNANDA SAMBONI IMBACHIAún no hay calificaciones

- Semana 7 PresupuestosDocumento35 páginasSemana 7 PresupuestosJroamsfmAún no hay calificaciones

- Infografia de PresupuestoDocumento3 páginasInfografia de PresupuestoYIRA MAYERLY MENDIVELSO HERNANDEZAún no hay calificaciones

- ACT8 Foro de TrabajoDocumento2 páginasACT8 Foro de TrabajoJhoseline HernándezAún no hay calificaciones

- M. Administrativo SiafDocumento40 páginasM. Administrativo Siafelizabeth100% (1)

- Preparacion para El CursoDocumento37 páginasPreparacion para El CursoRICARDO LUMBRE GUTIERREZAún no hay calificaciones

- 5 IeDocumento30 páginas5 IeRuth CatuntaAún no hay calificaciones

- CT en Clase UNIDAD 2Documento55 páginasCT en Clase UNIDAD 2Nicole CheroAún no hay calificaciones

- Esquema Liquidación CompletoDocumento1 páginaEsquema Liquidación CompletoJuan Carlos GRAún no hay calificaciones

- Real Cvu - Punto de Equilbrio y Planeación de UtilidadesDocumento28 páginasReal Cvu - Punto de Equilbrio y Planeación de UtilidadesANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Presentación - Cuenta General de La RepúblicaDocumento55 páginasPresentación - Cuenta General de La RepúblicaANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Caratula Tarea 1+Documento1 páginaCaratula Tarea 1+ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Semana 02Documento7 páginasSemana 02ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Cuenta General Republica 2022Documento476 páginasCuenta General Republica 2022ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Semana 2 - Auditoria IiDocumento43 páginasSemana 2 - Auditoria IiANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Métodos Pert - CPMDocumento51 páginasMétodos Pert - CPMANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Impuesto de AlcabalaDocumento1 páginaImpuesto de AlcabalaANGEL REY MARTINEZ CASTILLO100% (1)

- Importaciones - Conectando Al Mundo A Travès Del ComercioDocumento21 páginasImportaciones - Conectando Al Mundo A Travès Del ComercioANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Grupo Tributosaurios - Tarea 5Documento59 páginasGrupo Tributosaurios - Tarea 5ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Impuesto A Las No DeportivasDocumento1 páginaImpuesto A Las No DeportivasANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

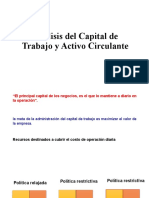

- Análisis Del Capital de TrabajoDocumento9 páginasAnálisis Del Capital de TrabajoANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- G5 - T9 - Auditoria IDocumento27 páginasG5 - T9 - Auditoria IANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Tarea Semana 9 - Auditoria IDocumento15 páginasTarea Semana 9 - Auditoria IANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Casos Prácticos NIC 19 - SoluciónDocumento4 páginasCasos Prácticos NIC 19 - SoluciónANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Casos Prácticos - NIIF 15 (Solución)Documento6 páginasCasos Prácticos - NIIF 15 (Solución)ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Casos Prácticos - NIC 20 (Solución)Documento5 páginasCasos Prácticos - NIC 20 (Solución)ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Impuesto A Los JuegosDocumento1 páginaImpuesto A Los JuegosANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Universidad Nacional de Trujillo: Facultad de Ciencias Económicas Escuela Profesional de Contabilidad y FinanzasDocumento109 páginasUniversidad Nacional de Trujillo: Facultad de Ciencias Económicas Escuela Profesional de Contabilidad y FinanzasANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Tarea Nic 29Documento18 páginasTarea Nic 29ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- CUL tVCqCsEm5yX2LJfQxOBTUADocumento2 páginasCUL tVCqCsEm5yX2LJfQxOBTUAANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Impuesto A Las ApuestasDocumento1 páginaImpuesto A Las ApuestasANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Mi ParteDocumento5 páginasMi ParteANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Clase Semana 12Documento19 páginasClase Semana 12ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- CUL-B2ZIb5 Oa4fx dXxgfC-uL12uqQDocumento2 páginasCUL-B2ZIb5 Oa4fx dXxgfC-uL12uqQANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Clips de FreefireDocumento1 páginaClips de FreefireANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- CLASE SEMANA 13 BonosDocumento24 páginasCLASE SEMANA 13 BonosANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Clase Semana 11Documento22 páginasClase Semana 11ANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Work Book: Como Facturar 6 CifrasDocumento5 páginasWork Book: Como Facturar 6 CifrasANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Estudio Adminastrativo Ultimo TrabajoDocumento2 páginasEstudio Adminastrativo Ultimo TrabajoANGEL REY MARTINEZ CASTILLOAún no hay calificaciones

- Gestionar El Cambio EducativoDocumento22 páginasGestionar El Cambio EducativoMiryam Alvarez ZegarraAún no hay calificaciones

- Manual Logística QuímicaDocumento22 páginasManual Logística QuímicaJose DiazAún no hay calificaciones

- Adecuar Area de Propagacion Vegetal Segun Criterios Tecnicos.Documento5 páginasAdecuar Area de Propagacion Vegetal Segun Criterios Tecnicos.John Frazer Lemus AsprillaAún no hay calificaciones

- 2022 06 06 Ejercicios PautaDocumento5 páginas2022 06 06 Ejercicios Pautaconstantino sabaj arzaniAún no hay calificaciones

- Descripcion de Puesto-Intendente PDFDocumento8 páginasDescripcion de Puesto-Intendente PDFAndrea Santos SantanderAún no hay calificaciones

- Escritura PublicaDocumento6 páginasEscritura PublicaALICIA BEATRIZ ACEVEDO CERNAAún no hay calificaciones

- Reglamento para La Administración de Las Áreas de Parqueo de La Universidad de San Carlos de GuatemalaDocumento14 páginasReglamento para La Administración de Las Áreas de Parqueo de La Universidad de San Carlos de GuatemalaEstudiantes por Derecho100% (9)

- Estatuto Regimen Académico de La Universidad Autónoma Tomás FríasDocumento14 páginasEstatuto Regimen Académico de La Universidad Autónoma Tomás FríasWilbert Rivera Muñoz100% (1)

- Admin. Operaciones Linea Del TiempoDocumento6 páginasAdmin. Operaciones Linea Del TiempoGreyman RufinoAún no hay calificaciones

- Ejercicios Grado 3 Contabilidad y Administraci NDocumento12 páginasEjercicios Grado 3 Contabilidad y Administraci NJose Andres Orrala DueñasAún no hay calificaciones

- Adam SmithDocumento3 páginasAdam SmithSergi David ConstanteAún no hay calificaciones

- 1 - Informe Defensoría Del Pueblo PDFDocumento147 páginas1 - Informe Defensoría Del Pueblo PDFAnonymous 7vX01XUMYAún no hay calificaciones

- Cochinilla EmbalajeDocumento3 páginasCochinilla EmbalajeManuel MoraAún no hay calificaciones

- Lic. Víctor Hugo Mejía Illanes: Gestión 2015Documento7 páginasLic. Víctor Hugo Mejía Illanes: Gestión 2015Mateo Arroyo CortesAún no hay calificaciones

- Revista Axel OchoaDocumento8 páginasRevista Axel OchoaAxel OchoaAún no hay calificaciones

- Manual de Perfiles de PuestosDocumento6 páginasManual de Perfiles de PuestosWilfredo CamposAún no hay calificaciones

- CARTA N.001-Solicitud de Pago 2022 - ROGER BENITO SANCHEZ MONTERODocumento3 páginasCARTA N.001-Solicitud de Pago 2022 - ROGER BENITO SANCHEZ MONTERORosmery LopezAún no hay calificaciones

- MACROENTORNODocumento6 páginasMACROENTORNOrocio1412100% (1)

- Fundo LeticiaDocumento25 páginasFundo LeticiaJulyAún no hay calificaciones

- COM00004 - Derecho Societario Peruano (Enrique Elias)Documento33 páginasCOM00004 - Derecho Societario Peruano (Enrique Elias)SANCHEZ ARANDA & ABOGADOS80% (10)

- La Discriminación A Los Consumidores Extranjeros en Un Caso Colectivo - Por Alejandro Perez HazañaDocumento12 páginasLa Discriminación A Los Consumidores Extranjeros en Un Caso Colectivo - Por Alejandro Perez HazañavaporesoyoAún no hay calificaciones

- Ejercicio Estados Financieros Marcar Con Una XDocumento3 páginasEjercicio Estados Financieros Marcar Con Una XDaniel PalmerAún no hay calificaciones

- Hacia Una Nueva Gestion EscolarDocumento12 páginasHacia Una Nueva Gestion EscolarDaniela Pacheco HernándezAún no hay calificaciones

- Notas de Metodos Cuantitativos 2014Documento63 páginasNotas de Metodos Cuantitativos 2014Carlos Ernesto Isaza Carvajal100% (1)

- Modelo - Contrato Salario Integral Enero 2018Documento5 páginasModelo - Contrato Salario Integral Enero 2018Jose Rafael Ripoll ParejoAún no hay calificaciones

- 2015 05 14 Propiedad Horizontal KiperDocumento34 páginas2015 05 14 Propiedad Horizontal KiperPablo Di Iorio100% (1)

- GRUPO 1 - VOP - Segmento de Mercado y Propuesta de ValorDocumento5 páginasGRUPO 1 - VOP - Segmento de Mercado y Propuesta de ValorIván Rugel CoronelAún no hay calificaciones

- Anatomía de Una Llamada Telefónica A Un ProspectoDocumento7 páginasAnatomía de Una Llamada Telefónica A Un ProspectojavierbattilanaAún no hay calificaciones

- Malla de Estudio Ingenieria en Informatica INACAPDocumento1 páginaMalla de Estudio Ingenieria en Informatica INACAPFélix ValdésAún no hay calificaciones

- EnvasesDocumento5 páginasEnvaseschristian harbauer santosAún no hay calificaciones