También podría gustarte

- Perspectiva de Valores InternosDocumento4 páginasPerspectiva de Valores InternosMandi SummersAún no hay calificaciones

- Asignación de Equipos Aplicando Ing de MétodosDocumento3 páginasAsignación de Equipos Aplicando Ing de MétodosMandi SummersAún no hay calificaciones

- Trabajo - Modelo Canvas de Una Empresa Navideña - Julio - VincentiDocumento2 páginasTrabajo - Modelo Canvas de Una Empresa Navideña - Julio - VincentiMandi SummersAún no hay calificaciones

- Diseño de Plachas Bases de Columnas AnclajeDocumento142 páginasDiseño de Plachas Bases de Columnas AnclajeMandi Summers100% (1)

- Análisis Mediante Arbol de Fallas Por Eduardo ContrerasDocumento10 páginasAnálisis Mediante Arbol de Fallas Por Eduardo ContrerasMandi SummersAún no hay calificaciones

- Trabajo - Diagnóstico de Las Causas Que Condujeron A La Condición Actual dePDVSA - Julio - VincentiDocumento4 páginasTrabajo - Diagnóstico de Las Causas Que Condujeron A La Condición Actual dePDVSA - Julio - VincentiMandi SummersAún no hay calificaciones

- MÉTODOS GEOFÍSICOS - Julio VincentiDocumento18 páginasMÉTODOS GEOFÍSICOS - Julio VincentiMandi SummersAún no hay calificaciones

- Curso BID. Nuevas Tendencias en Tratados ComercialesDocumento57 páginasCurso BID. Nuevas Tendencias en Tratados ComercialesMandi SummersAún no hay calificaciones

- Sistema de Información GerencialDocumento4 páginasSistema de Información GerencialMandi SummersAún no hay calificaciones

- Ruidos en La ComunicaciónDocumento8 páginasRuidos en La ComunicaciónMandi SummersAún no hay calificaciones

- Aristoteles - Onasis - Ejemplos - Comparativos de Su Éxito - Julio - VincentiDocumento3 páginasAristoteles - Onasis - Ejemplos - Comparativos de Su Éxito - Julio - VincentiMandi SummersAún no hay calificaciones

- Formación Docente en IberoaméricaDocumento102 páginasFormación Docente en IberoaméricaMandi SummersAún no hay calificaciones

- Nuevo Grid Gerencial. Blake y MoutonDocumento32 páginasNuevo Grid Gerencial. Blake y MoutonMandi SummersAún no hay calificaciones

- Informe Técnico Hacia La Toma de Decisión para La Aplicación de La Gestión Financiera Del Activo Circulante de La Empresa.Documento6 páginasInforme Técnico Hacia La Toma de Decisión para La Aplicación de La Gestión Financiera Del Activo Circulante de La Empresa.Mandi SummersAún no hay calificaciones

- Examen Práctico de Simulación de Sistemas Julio VincentiDocumento6 páginasExamen Práctico de Simulación de Sistemas Julio VincentiMandi SummersAún no hay calificaciones

- Especializacion Gerencias de Proyecto - CompressedDocumento7 páginasEspecializacion Gerencias de Proyecto - CompressedMandi SummersAún no hay calificaciones

- República: Evolucion Del Pensamiento Administrativo. LaDocumento7 páginasRepública: Evolucion Del Pensamiento Administrativo. LaMandi SummersAún no hay calificaciones

- Informe Técnico Hacia La Toma de Decisión para La Aplicación de La Gestión Financiera Del Activo Circulante de La Empresa Grupo Abstracto Plus, C.A.Documento48 páginasInforme Técnico Hacia La Toma de Decisión para La Aplicación de La Gestión Financiera Del Activo Circulante de La Empresa Grupo Abstracto Plus, C.A.Mandi SummersAún no hay calificaciones

- La Organización en La IndustriaDocumento22 páginasLa Organización en La IndustriaMandi SummersAún no hay calificaciones

- Analisis Inferencial de Los Activos de Las Cuentas Contables de Tres EmpresasDocumento17 páginasAnalisis Inferencial de Los Activos de Las Cuentas Contables de Tres EmpresasMandi SummersAún no hay calificaciones

- Administración de Recursos Humanos de Cara Al Fenomeno Globalizador en El Proceso de Reclutamiento y SelecciónDocumento14 páginasAdministración de Recursos Humanos de Cara Al Fenomeno Globalizador en El Proceso de Reclutamiento y SelecciónMandi SummersAún no hay calificaciones

- Entorno Global y El Comercio InternacionalDocumento2 páginasEntorno Global y El Comercio InternacionalMandi SummersAún no hay calificaciones

- Analisis Del Control Interno de Un Sistema Contable para La EmpresaDocumento8 páginasAnalisis Del Control Interno de Un Sistema Contable para La EmpresaMandi SummersAún no hay calificaciones

- Informe Inicial de Pasantias. Banco ExteriorDocumento5 páginasInforme Inicial de Pasantias. Banco ExteriorMandi SummersAún no hay calificaciones

- Plan Doctorado Indivializado Facultad de Ingeniería UCVDocumento1 páginaPlan Doctorado Indivializado Facultad de Ingeniería UCVMandi SummersAún no hay calificaciones

- Clases de Acueductos y Cloacas Parte II. Prof FariasDocumento108 páginasClases de Acueductos y Cloacas Parte II. Prof FariasMandi SummersAún no hay calificaciones

- Clases de Acueductos y Cloacas Parte I. Prof FariasDocumento94 páginasClases de Acueductos y Cloacas Parte I. Prof FariasMandi SummersAún no hay calificaciones

- Clase Especial (Redes de Distribución) 2010 IIIDocumento20 páginasClase Especial (Redes de Distribución) 2010 IIIMandi SummersAún no hay calificaciones

- Cuestionario Medios de PagoDocumento8 páginasCuestionario Medios de PagoJose Zavala PinillaAún no hay calificaciones

- Taller Anualidades y Liquidación de Instrumentos de InversiónDocumento12 páginasTaller Anualidades y Liquidación de Instrumentos de InversiónYulieth Zuleta50% (2)

- Cuestionario de Los Títulos de CréditoDocumento3 páginasCuestionario de Los Títulos de CréditoMarcos LoconAún no hay calificaciones

- Taller 2 Conciliacion BancariaDocumento7 páginasTaller 2 Conciliacion BancariaANA SHIRLEY PINEDA ANGELAún no hay calificaciones

- ContratosFORM UNICO DE VINC DE PER FISDocumento19 páginasContratosFORM UNICO DE VINC DE PER FIShirari -chanAún no hay calificaciones

- Chinchina - Listado Pagos 5 y 6 BancarizadosDocumento76 páginasChinchina - Listado Pagos 5 y 6 Bancarizadoshanner aragonAún no hay calificaciones

- Tarea Contabilidad IIDocumento15 páginasTarea Contabilidad IIAngela PeraltaAún no hay calificaciones

- Excel Alfa TrabajoDocumento3 páginasExcel Alfa Trabajoderly solisAún no hay calificaciones

- Modulo Estudiante Pedagogia Ludica FinancieraDocumento148 páginasModulo Estudiante Pedagogia Ludica FinancieraAlgemiro Leonidaz75% (4)

- Solucion Clase 51A Excel Avanzado 2007 - Ejercicios de Algunos Temas AnterioresDocumento33 páginasSolucion Clase 51A Excel Avanzado 2007 - Ejercicios de Algunos Temas AnterioresJhon Mabesoy JimenezAún no hay calificaciones

- Tarea S3 Introduccion A La ContabilidadDocumento6 páginasTarea S3 Introduccion A La ContabilidadElenaSantanaAún no hay calificaciones

- AMORTIZACIONESDocumento16 páginasAMORTIZACIONESABEL C.tAún no hay calificaciones

- Jamn Servicios Generales S.A.C.: Factura Electrónica RUC: 20601320127 E001-8Documento1 páginaJamn Servicios Generales S.A.C.: Factura Electrónica RUC: 20601320127 E001-8Andrew Kalef Monzon MedinaAún no hay calificaciones

- Formato de Pago Universal With PrimefacesDocumento1 páginaFormato de Pago Universal With PrimefacesChubeMexAún no hay calificaciones

- Historia de Crédito - Datacredito CREDIYES SAS: Ultima Consultas RealizadasDocumento6 páginasHistoria de Crédito - Datacredito CREDIYES SAS: Ultima Consultas RealizadasAlejandro Alzate MosqueraAún no hay calificaciones

- Sesion #01 - Indice - Conciliaciones - Bancarias (Parte 1) - Actualzado Al 28.06.21Documento55 páginasSesion #01 - Indice - Conciliaciones - Bancarias (Parte 1) - Actualzado Al 28.06.21Najib AlanyaAún no hay calificaciones

- Cuenta de Ahorros2396 - Abril-2019Documento2 páginasCuenta de Ahorros2396 - Abril-2019Felipe IbarraAún no hay calificaciones

- Fuentes de Préstamos A Corto Plazo Sin GarantíaDocumento2 páginasFuentes de Préstamos A Corto Plazo Sin Garantíamalibu yariAún no hay calificaciones

- Act. 5 Conciliacion Bancaria - Galvan - Sosa - Armando FidelDocumento15 páginasAct. 5 Conciliacion Bancaria - Galvan - Sosa - Armando FidelArmando Galvan SosaAún no hay calificaciones

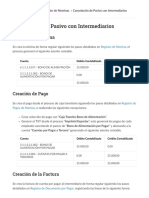

- CONTABILIDAD - 79 - Cancelación de Pasivo Con IntermediariosDocumento2 páginasCONTABILIDAD - 79 - Cancelación de Pasivo Con IntermediariosEdwin ReynaAún no hay calificaciones

- Comportamiento: Libretón Básico Cuenta DigitalDocumento7 páginasComportamiento: Libretón Básico Cuenta DigitalJahir MedinaAún no hay calificaciones

- Banco Azteca 2Documento2 páginasBanco Azteca 2Keila GorostietaAún no hay calificaciones

- 2.semana 3 Guion Oferta MonetariaDocumento2 páginas2.semana 3 Guion Oferta MonetariaJuan de la cruz olivosAún no hay calificaciones

- El Terror ContableDocumento15 páginasEl Terror ContableisraipnunamAún no hay calificaciones

- Mell Napa - Grupo 01Documento5 páginasMell Napa - Grupo 01Romina Gonzales MenesesAún no hay calificaciones

- Universidad Salesiana de Bolivia: Contaduría PúblicaDocumento8 páginasUniversidad Salesiana de Bolivia: Contaduría Públicacarla quspeAún no hay calificaciones

- TUYaDocumento2 páginasTUYaArmando SanchezAún no hay calificaciones

- Inclusion FinancieraDocumento363 páginasInclusion Financieramandrake1233Aún no hay calificaciones

- Practica 5 y 6 ECONOMICADocumento5 páginasPractica 5 y 6 ECONOMICAKevin Dueñas Porras100% (1)

- Relación de Cobro 20230802190155Documento3 páginasRelación de Cobro 20230802190155Alex MirosAún no hay calificaciones