0% encontró este documento útil (0 votos)

77 vistas6 páginasAnálisis de Quiebre Estructural en Econometría

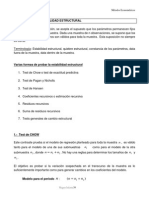

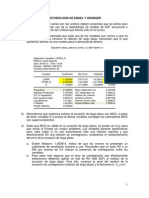

Este documento presenta un análisis de quiebre estructural utilizando diferentes pruebas como el test de Chow. Se generan variables y se estiman modelos antes y después de un posible punto de quiebre en 1998.

Cargado por

isabel blanco ibarraDerechos de autor

© © All Rights Reserved

Nos tomamos en serio los derechos de los contenidos. Si sospechas que se trata de tu contenido, reclámalo aquí.

Formatos disponibles

Descarga como DOC, PDF, TXT o lee en línea desde Scribd

0% encontró este documento útil (0 votos)

77 vistas6 páginasAnálisis de Quiebre Estructural en Econometría

Este documento presenta un análisis de quiebre estructural utilizando diferentes pruebas como el test de Chow. Se generan variables y se estiman modelos antes y después de un posible punto de quiebre en 1998.

Cargado por

isabel blanco ibarraDerechos de autor

© © All Rights Reserved

Nos tomamos en serio los derechos de los contenidos. Si sospechas que se trata de tu contenido, reclámalo aquí.

Formatos disponibles

Descarga como DOC, PDF, TXT o lee en línea desde Scribd