También podría gustarte

- Banking Law Notes PDFDocumento64 páginasBanking Law Notes PDFsoumya100% (2)

- Derek Byerlee, Walter P. Falcon, Rosamond L. Naylor - The Tropical Oil Crop Revolution - Food, Feed, Fuel, and Forests (2016, Oxford University Press)Documento305 páginasDerek Byerlee, Walter P. Falcon, Rosamond L. Naylor - The Tropical Oil Crop Revolution - Food, Feed, Fuel, and Forests (2016, Oxford University Press)Dan MuntoiuAún no hay calificaciones

- Regional Rural Banks of India: Evolution, Performance and ManagementDe EverandRegional Rural Banks of India: Evolution, Performance and ManagementAún no hay calificaciones

- 2010 Succul Plant CatalogueDocumento7 páginas2010 Succul Plant CataloguesangoneraAún no hay calificaciones

- A Cowboys LifeDocumento19 páginasA Cowboys LifeDucThinhNguyenAún no hay calificaciones

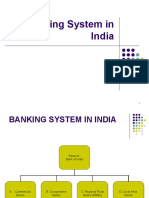

- 2 - Banking System in India - May06,'09Documento9 páginas2 - Banking System in India - May06,'09bishnoimAún no hay calificaciones

- A Presentation On Financial Market Structure: Presented By: Hanmesh (06/MBA/37) Sandeep (06/MBA/38) Sneha (06/MBA/39)Documento36 páginasA Presentation On Financial Market Structure: Presented By: Hanmesh (06/MBA/37) Sandeep (06/MBA/38) Sneha (06/MBA/39)sageesnehaAún no hay calificaciones

- Banking StructureDocumento18 páginasBanking StructureMathangiAún no hay calificaciones

- SBI Banking Products Awareness Study ChartDocumento4 páginasSBI Banking Products Awareness Study ChartJiby JohnAún no hay calificaciones

- Mission Vission and ValuesDocumento8 páginasMission Vission and ValuesJiby JohnAún no hay calificaciones

- The Structure of Indian Banking SectorDocumento1 páginaThe Structure of Indian Banking SectorSAún no hay calificaciones

- Indian Banking StructureDocumento5 páginasIndian Banking StructurevivekAún no hay calificaciones

- Banking Industry Overview: History, Structure and Current ScenarioDocumento77 páginasBanking Industry Overview: History, Structure and Current Scenarioprashant mhatreAún no hay calificaciones

- Indian Banking System StructureDocumento13 páginasIndian Banking System StructureNandhini VirgoAún no hay calificaciones

- Indian Banking StructureDocumento24 páginasIndian Banking StructureRENUKA CHAUHANAún no hay calificaciones

- Banking Structure in IndiaDocumento1 páginaBanking Structure in IndiapnrkumarAún no hay calificaciones

- Types of banks and offshore bankingDocumento14 páginasTypes of banks and offshore bankingsnehalakhadeAún no hay calificaciones

- Banking Management: Presented by C. KavyaDocumento27 páginasBanking Management: Presented by C. KavyaKaviya KaviAún no hay calificaciones

- Indian Banking Mission and VisionDocumento10 páginasIndian Banking Mission and VisionkarthickkrishnanmbaAún no hay calificaciones

- Chapter 2Documento18 páginasChapter 2ShivuPannurAún no hay calificaciones

- Scheduled and Non-Scheduled Banks: Key DifferencesDocumento25 páginasScheduled and Non-Scheduled Banks: Key DifferencesMoncy Idicula MathaiAún no hay calificaciones

- Indian Organised Money Market Institutions and Their FinancialDocumento20 páginasIndian Organised Money Market Institutions and Their FinancialSikander KalraAún no hay calificaciones

- Banking Structure in IndiaDocumento24 páginasBanking Structure in Indiasandeep95Aún no hay calificaciones

- 08 Chapter 1Documento48 páginas08 Chapter 1SanjidaAún no hay calificaciones

- SelvakumarDocumento14 páginasSelvakumarSelvakumarAún no hay calificaciones

- 4 Banking LawDocumento85 páginas4 Banking LawRamesh BuridiAún no hay calificaciones

- Et of NstructionsDocumento460 páginasEt of NstructionsMokshita VajawatAún no hay calificaciones

- Scheduled Bank Non Scheduled Bank PDFDocumento6 páginasScheduled Bank Non Scheduled Bank PDFSelvaraj Villy100% (1)

- 6 Ispes Fy 2020 FinalDocumento25 páginas6 Ispes Fy 2020 FinalDhruti GuptaAún no hay calificaciones

- Banking Structure in IndiaDocumento9 páginasBanking Structure in IndiaDhanu BhardwajAún no hay calificaciones

- List of BanksDocumento6 páginasList of Bankslucky1142Aún no hay calificaciones

- Structure of The Indian Banking Industry: Commercial BanksDocumento2 páginasStructure of The Indian Banking Industry: Commercial BanksMayank AhujaAún no hay calificaciones

- Banking Sector OverviewDocumento34 páginasBanking Sector OverviewteckdivAún no hay calificaciones

- Banking Types ExplainedDocumento0 páginasBanking Types Explainedsundeep_100Aún no hay calificaciones

- The Following Are The Scheduled Banks in India (Public Sector)Documento2 páginasThe Following Are The Scheduled Banks in India (Public Sector)deependrakuril55Aún no hay calificaciones

- Banking in India: Bank of Bengal (HQ)Documento16 páginasBanking in India: Bank of Bengal (HQ)Kiran GireeshAún no hay calificaciones

- Banking StructureDocumento3 páginasBanking StructureMayank AhujaAún no hay calificaciones

- Structure of the Indian Banking System Sem IDocumento2 páginasStructure of the Indian Banking System Sem IAshitosh ChavanAún no hay calificaciones

- 1.) Banking Overview and RegulationsDocumento69 páginas1.) Banking Overview and RegulationsAnisha SapraAún no hay calificaciones

- Typesofbanks Unit 1Documento14 páginasTypesofbanks Unit 1VINAYKUMAR H RAún no hay calificaciones

- Presentation Type of Banking 1527319172 147767Documento13 páginasPresentation Type of Banking 1527319172 147767Vinita PattanshettiAún no hay calificaciones

- Economy Banking System in IndiaDocumento21 páginasEconomy Banking System in Indiakrishan palAún no hay calificaciones

- Origin of Banking and Banking Structure in IndiaDocumento32 páginasOrigin of Banking and Banking Structure in IndiaShashank TiwariAún no hay calificaciones

- Origin of Banking and Banking Structure in IndiaDocumento32 páginasOrigin of Banking and Banking Structure in IndiaShashank TiwariAún no hay calificaciones

- Types of Banks: Presented By: Roll NoDocumento22 páginasTypes of Banks: Presented By: Roll NosnehalakhadeAún no hay calificaciones

- Unit - 1Documento93 páginasUnit - 1Suji MbaAún no hay calificaciones

- A.2 AssignmentDocumento5 páginasA.2 AssignmentNijiraAún no hay calificaciones

- Banking Structure in IndiaDocumento31 páginasBanking Structure in IndiaRishabhShuklaAún no hay calificaciones

- Unit I The Indian Financial SystemDocumento21 páginasUnit I The Indian Financial SystemGreeshma ChittilappillyAún no hay calificaciones

- Lead Bank SchemeDocumento3 páginasLead Bank SchemeKarthik VinnakotaAún no hay calificaciones

- Banking Management: Presented by C. KavyaDocumento28 páginasBanking Management: Presented by C. KavyaKaviya KaviAún no hay calificaciones

- Chapter 2. Lecture 2.1 Kinds of Banks and Its FunctionsDocumento7 páginasChapter 2. Lecture 2.1 Kinds of Banks and Its FunctionsvibhuAún no hay calificaciones

- Structure of Commercial BanksDocumento4 páginasStructure of Commercial BanksMunish PathaniaAún no hay calificaciones

- Indian Banking Sector-An IntroductionDocumento16 páginasIndian Banking Sector-An Introductionbando007Aún no hay calificaciones

- Chapter 3Documento93 páginasChapter 3Shifali ShettyAún no hay calificaciones

- BankingDocumento85 páginasBankingZeel kachhiaAún no hay calificaciones

- Assessments of BanksDocumento94 páginasAssessments of Bankskavita.m.yadavAún no hay calificaciones

- Project Report)Documento38 páginasProject Report)Swathi JAún no hay calificaciones

- BankingDocumento74 páginasBankingAbhishek DubeyAún no hay calificaciones

- Types of BanksDocumento5 páginasTypes of BanksAsif AliAún no hay calificaciones

- Financial Soundness Indicators for Financial Sector Stability in BangladeshDe EverandFinancial Soundness Indicators for Financial Sector Stability in BangladeshAún no hay calificaciones

- Banking India: Accepting Deposits for the Purpose of LendingDe EverandBanking India: Accepting Deposits for the Purpose of LendingAún no hay calificaciones

- Kerala Agro Machinery Corporation Internship ReportDocumento61 páginasKerala Agro Machinery Corporation Internship ReportRoshni100% (1)

- Kerala Agro Machinery Corporation Internship ReportDocumento61 páginasKerala Agro Machinery Corporation Internship ReportRoshni100% (1)

- Organizational Study at Kamco-RaheesDocumento59 páginasOrganizational Study at Kamco-RaheesRAHEES100% (3)

- Organizational Study at Kamco-RaheesDocumento59 páginasOrganizational Study at Kamco-RaheesRAHEES100% (3)

- Antony Kolanchery Faculty of Management: E-BankingDocumento19 páginasAntony Kolanchery Faculty of Management: E-BankingRoshniAún no hay calificaciones

- 5) JournalDocumento24 páginas5) JournalRay ChAún no hay calificaciones

- Kamco Website Tender KC TDR 76 3 DT 05-07-2011Documento13 páginasKamco Website Tender KC TDR 76 3 DT 05-07-2011RoshniAún no hay calificaciones

- Group Activity - Sustainable - Mangyans of MindoroDocumento14 páginasGroup Activity - Sustainable - Mangyans of MindoroK CastleAún no hay calificaciones

- Connectors Multiple Exercises AnswersDocumento14 páginasConnectors Multiple Exercises AnswersIrene SánchezAún no hay calificaciones

- 46th Croatian & 6th International Symposium On AgricultureDocumento5 páginas46th Croatian & 6th International Symposium On AgriculturevikeshchemAún no hay calificaciones

- Phillipine PresidentsDocumento15 páginasPhillipine PresidentsJulius BeraldeAún no hay calificaciones

- Sharad PawarDocumento5 páginasSharad PawarAnjali KhannaAún no hay calificaciones

- A Brief Presentation On Seed Quality and Seed Development ProgrammesDocumento21 páginasA Brief Presentation On Seed Quality and Seed Development Programmesc.k.nivedhaAún no hay calificaciones

- Teaching About Invasive Species TocDocumento2 páginasTeaching About Invasive Species Tocapi-279273216Aún no hay calificaciones

- South Korea's Industrial Development and Role of GovernmentDocumento24 páginasSouth Korea's Industrial Development and Role of GovernmentKamrul MozahidAún no hay calificaciones

- Handout-3 On Env & Ecology by Mrs. Vaishali Anand PDFDocumento13 páginasHandout-3 On Env & Ecology by Mrs. Vaishali Anand PDFSk ShuklaAún no hay calificaciones

- CIDAM Group 1 Origin and Subsystem of The Earth (FINAL)Documento12 páginasCIDAM Group 1 Origin and Subsystem of The Earth (FINAL)Venoc Hosmillo0% (1)

- 34-Husk MulchingDocumento2 páginas34-Husk MulchingFrank Dagohoy0% (1)

- List of Indian Plantation CompaniesDocumento318 páginasList of Indian Plantation CompaniesNikita Parekh100% (1)

- Vegetative ReproductionDocumento19 páginasVegetative ReproductionJane Sandra LimAún no hay calificaciones

- ICID - WEF Nexus Model - IcidtemplateDocumento30 páginasICID - WEF Nexus Model - Icidtemplatekrishnamondal160Aún no hay calificaciones

- Thesis On Food Security PDFDocumento8 páginasThesis On Food Security PDFbsrf4d9d100% (2)

- Neonicotinoid: Neonicotinoids (Sometimes Shortened To NeonicsDocumento21 páginasNeonicotinoid: Neonicotinoids (Sometimes Shortened To NeonicsMonica DiazAún no hay calificaciones

- DRR-CCA EIA Technical GuidelinesDocumento385 páginasDRR-CCA EIA Technical GuidelinesMabelGaviolaVallenaAún no hay calificaciones

- Brand Book 2019Documento60 páginasBrand Book 2019Avinash DekaAún no hay calificaciones

- Keragaman Jeruk Fungsional Indonesia Berdasarkan Karakter Morfologis Dan Marka RAPDDocumento10 páginasKeragaman Jeruk Fungsional Indonesia Berdasarkan Karakter Morfologis Dan Marka RAPDUlfahAún no hay calificaciones

- Interview SultonDocumento4 páginasInterview SultonSulton Okta MaulanaAún no hay calificaciones

- PREPARING SALADS AND DRESSINGSDocumento61 páginasPREPARING SALADS AND DRESSINGSAnna Christina YpilAún no hay calificaciones

- Mountains and PlateausDocumento7 páginasMountains and PlateausRodrigo LabitoriaAún no hay calificaciones

- Tractor FORD 4000 4Documento5 páginasTractor FORD 4000 4Alex CastilloAún no hay calificaciones

- World06 24 15Documento39 páginasWorld06 24 15The WorldAún no hay calificaciones

- ANT A01. Introduction To Anthropology - Becoming Human (Winter 2021) Essay - Review of The Archaeological Evidence For Crop DomesticationDocumento9 páginasANT A01. Introduction To Anthropology - Becoming Human (Winter 2021) Essay - Review of The Archaeological Evidence For Crop DomesticationWonder LostAún no hay calificaciones

- Agricultural Dependence of 18th Century FranceDocumento12 páginasAgricultural Dependence of 18th Century FranceSudhanshu kalekingeAún no hay calificaciones

- 2288 7485 1 PB PDFDocumento7 páginas2288 7485 1 PB PDFrajashekhar asAún no hay calificaciones