También podría gustarte

- Fema 2000Documento31 páginasFema 2000Manpreet Kaur SekhonAún no hay calificaciones

- Presented By: Adnan AliDocumento22 páginasPresented By: Adnan AliAdnan AliAún no hay calificaciones

- Foreign Exchange Management Act (FEMA)Documento8 páginasForeign Exchange Management Act (FEMA)sudheer1000Aún no hay calificaciones

- Foreign Exchange Regulation ActDocumento3 páginasForeign Exchange Regulation ActHIMANSHU DARGANAún no hay calificaciones

- Prof. Gurpartap SinghDocumento27 páginasProf. Gurpartap Singhlali62Aún no hay calificaciones

- FEMA-Foreign Exchange Management ActDocumento4 páginasFEMA-Foreign Exchange Management ActAVINASH SINGHAún no hay calificaciones

- Switch From FERA: Act Parliament of IndiaDocumento4 páginasSwitch From FERA: Act Parliament of IndiaVipul GhoghariAún no hay calificaciones

- Presented By: S.Vignesh First Year MBA National Institute of Technology Karnataka SurathkalDocumento27 páginasPresented By: S.Vignesh First Year MBA National Institute of Technology Karnataka SurathkalsneyadavAún no hay calificaciones

- FemaDocumento25 páginasFemaSKSAIDINESHAún no hay calificaciones

- Foreign Exchange Management ActDocumento27 páginasForeign Exchange Management ActLokamAún no hay calificaciones

- Foreign Exchange Management Act 1999Documento13 páginasForeign Exchange Management Act 1999Abhisek SwainAún no hay calificaciones

- FEMA (LawDocumento27 páginasFEMA (LawMihir PanchalAún no hay calificaciones

- FemaDocumento7 páginasFemaNeha KhandoojaAún no hay calificaciones

- Fema NotesDocumento12 páginasFema NotesRishabh Dubey100% (3)

- Chapter 1: Introduction.: 1.1: Foreign Exchange Management ActDocumento31 páginasChapter 1: Introduction.: 1.1: Foreign Exchange Management ActHarikrishnan NairAún no hay calificaciones

- Balkar Singh, 8Documento29 páginasBalkar Singh, 8Balkar SinghAún no hay calificaciones

- Fema PresentationDocumento75 páginasFema Presentationnd4dadhichAún no hay calificaciones

- Foreign Exchange Management Act.: Name Roll No ContributionDocumento25 páginasForeign Exchange Management Act.: Name Roll No Contributiondenmax4uAún no hay calificaciones

- Foreign Exchange Management ActDocumento4 páginasForeign Exchange Management ActAshutosh GuptaAún no hay calificaciones

- Foreign Exchange Management ActDocumento40 páginasForeign Exchange Management ActBharat MalukaniAún no hay calificaciones

- Foreign Exchange Management Act 1999: Objectives of FEMADocumento3 páginasForeign Exchange Management Act 1999: Objectives of FEMAPriyadarshan KrishnaAún no hay calificaciones

- Foreign Exchange Management Act (FEMA) : Presented By: Ikjot Dhawan (10HM11)Documento26 páginasForeign Exchange Management Act (FEMA) : Presented By: Ikjot Dhawan (10HM11)Abhishek MishraAún no hay calificaciones

- Fera Fema Fema V/S Fera Basic Terms Regulation and Management of FemaDocumento33 páginasFera Fema Fema V/S Fera Basic Terms Regulation and Management of FemasubinAún no hay calificaciones

- National Law FEMADocumento5 páginasNational Law FEMAShayan ZafarAún no hay calificaciones

- Unit-Ii: Foreign Exchange Regulations and FormalitiesDocumento27 páginasUnit-Ii: Foreign Exchange Regulations and FormalitiesLAKSHMIKANTH.B MEC-AP/MCAún no hay calificaciones

- Law Relating To Foreign Exchange ManagementDocumento21 páginasLaw Relating To Foreign Exchange ManagementindlawyerAún no hay calificaciones

- Foreign Exchange Management Act (FEMA)Documento21 páginasForeign Exchange Management Act (FEMA)kripakaranAún no hay calificaciones

- FEMA Overview - Vijay Gupta - June 2019 PDFDocumento58 páginasFEMA Overview - Vijay Gupta - June 2019 PDFAsimAún no hay calificaciones

- Foreign Exchange Management Act (FEMA)Documento2 páginasForeign Exchange Management Act (FEMA)Vijay SisodiyaAún no hay calificaciones

- Foreign Exchange Management Act, 1999Documento15 páginasForeign Exchange Management Act, 1999Sumit KumarAún no hay calificaciones

- Foreign Exchange Management Act, 1999: Cma Ram Cost & Management AccountantDocumento16 páginasForeign Exchange Management Act, 1999: Cma Ram Cost & Management AccountantRaja NarayananAún no hay calificaciones

- Case Studies On Fema-1999Documento33 páginasCase Studies On Fema-1999Eknath Birari67% (3)

- The Foreign Exchange Management Act, 1999Documento20 páginasThe Foreign Exchange Management Act, 1999rashpinder singhAún no hay calificaciones

- Module - 7 FemaDocumento13 páginasModule - 7 FemaNAVAZTHOKURAún no hay calificaciones

- Foreign Exchange Management Act, 1999: Foreignexchangemanagementact (Fema)Documento11 páginasForeign Exchange Management Act, 1999: Foreignexchangemanagementact (Fema)Gaurang VyasAún no hay calificaciones

- Fema (Foreign Exchange Management ActDocumento25 páginasFema (Foreign Exchange Management ActMayank GargAún no hay calificaciones

- History: Indian Parliament Indira GandhiDocumento44 páginasHistory: Indian Parliament Indira GandhisangeethaAún no hay calificaciones

- Foreign Exchange Management ActDocumento2 páginasForeign Exchange Management Acta1shockAún no hay calificaciones

- BRBL CH 10 FullDocumento16 páginasBRBL CH 10 FullSaurabh SiddhantAún no hay calificaciones

- Foreign Exchange Management Act, 1999: Sec 1: Preamble, Extent, Application & Commencement of FEMADocumento14 páginasForeign Exchange Management Act, 1999: Sec 1: Preamble, Extent, Application & Commencement of FEMARaj Reddy BurujukatiAún no hay calificaciones

- The Foreign Exchange Management Act, 1999: Learning Outcomes After Reading This Chapter, You Will Be Able To UnderstandDocumento53 páginasThe Foreign Exchange Management Act, 1999: Learning Outcomes After Reading This Chapter, You Will Be Able To UnderstandgvcAún no hay calificaciones

- Foreign Exchange Management ActDocumento14 páginasForeign Exchange Management ActPruthviraj RathoreAún no hay calificaciones

- Foreign Exchange Management Act, 1999 (FEMA) : Prof. Dhaval BhattDocumento22 páginasForeign Exchange Management Act, 1999 (FEMA) : Prof. Dhaval BhattMangesh KadamAún no hay calificaciones

- Foreign Exchange Management Act, 1999Documento15 páginasForeign Exchange Management Act, 1999Yatin GuptaAún no hay calificaciones

- Presentation On FEMA and Money Laundering PGDM 13-15 Section C GROUP 1Documento34 páginasPresentation On FEMA and Money Laundering PGDM 13-15 Section C GROUP 1raushanrahulAún no hay calificaciones

- Chapter - 15 Foreign Exchange - 240111 - 123533Documento22 páginasChapter - 15 Foreign Exchange - 240111 - 123533fs3482335Aún no hay calificaciones

- Fema FeraDocumento16 páginasFema Feraprani1507Aún no hay calificaciones

- Bos 46195 Mod 3 CP 1Documento66 páginasBos 46195 Mod 3 CP 1vishwa jothyAún no hay calificaciones

- Definition of FEMA 2000Documento5 páginasDefinition of FEMA 2000Yogita SharmaAún no hay calificaciones

- Essentials of Business EnvironmentDocumento11 páginasEssentials of Business EnvironmentAnkit ModiAún no hay calificaciones

- Prestige Institute of Management and Research: Business LawDocumento25 páginasPrestige Institute of Management and Research: Business LawMurtaza RiyazAún no hay calificaciones

- Foreign Exchange Regulation Act (FERA)Documento58 páginasForeign Exchange Regulation Act (FERA)ShiviAún no hay calificaciones

- FemaDocumento50 páginasFemalulughoshAún no hay calificaciones

- Foreign Exchange Management Act, 1999Documento12 páginasForeign Exchange Management Act, 1999shubhAún no hay calificaciones

- Fema 1999Documento36 páginasFema 1999Great Inventions 2k19Aún no hay calificaciones

- Foreign Exchange Management Act, 2000: Presented By: Akanksha MalhotraDocumento19 páginasForeign Exchange Management Act, 2000: Presented By: Akanksha MalhotraGaurav KumarAún no hay calificaciones

- Foreign Exchange Transactions ActDe EverandForeign Exchange Transactions ActAún no hay calificaciones

- Business Success in India: A Complete Guide to Build a Successful Business Knot with Indian FirmsDe EverandBusiness Success in India: A Complete Guide to Build a Successful Business Knot with Indian FirmsAún no hay calificaciones

- Introduction to Negotiable Instruments: As per Indian LawsDe EverandIntroduction to Negotiable Instruments: As per Indian LawsCalificación: 5 de 5 estrellas5/5 (1)

- Personal Selling OutsourcingDocumento10 páginasPersonal Selling OutsourcingBarunjmAún no hay calificaciones

- Chap03 Ethical & Environmental IssueDocumento20 páginasChap03 Ethical & Environmental IssueBarunjmAún no hay calificaciones

- Chap 04 TargetingDocumento26 páginasChap 04 TargetingBarunjmAún no hay calificaciones

- The Negotiable Instruments Act, 1881Documento57 páginasThe Negotiable Instruments Act, 1881Barunjm100% (1)

- Business: Business Means Any Activity Performed With The Profit Objective in MindDocumento40 páginasBusiness: Business Means Any Activity Performed With The Profit Objective in MindBarunjmAún no hay calificaciones

- The Negotiable Instruments Act 1881Documento57 páginasThe Negotiable Instruments Act 1881Barunjm100% (1)

- The Buying Process and Buyer BehaviourDocumento24 páginasThe Buying Process and Buyer BehaviourBarunjmAún no hay calificaciones

- Cyber Crimes and SecuritiesDocumento51 páginasCyber Crimes and SecuritiesBarunjmAún no hay calificaciones

- What Is RISKDocumento23 páginasWhat Is RISKBarunjmAún no hay calificaciones

- SLBCDocumento1 páginaSLBCyogesh shingareAún no hay calificaciones

- Business Communication & Report Writing: Jeta MajumderDocumento87 páginasBusiness Communication & Report Writing: Jeta MajumderShahadat HossainAún no hay calificaciones

- Term Paper: Bangladesh University of Professionals (Bup)Documento5 páginasTerm Paper: Bangladesh University of Professionals (Bup)Muslima Mubashera Reza RupaAún no hay calificaciones

- Essential Leadership Lessons From Top CEOs - Lou Gerstner, Jack Welch, Sam Walton, Howard Hughes, Lee Iacocca, Phil Knight, Walt Disney, Carlos Ghosn, Andrew S.Grove PDFDocumento112 páginasEssential Leadership Lessons From Top CEOs - Lou Gerstner, Jack Welch, Sam Walton, Howard Hughes, Lee Iacocca, Phil Knight, Walt Disney, Carlos Ghosn, Andrew S.Grove PDFananth080864100% (2)

- 23.07.2022 - Updated NITDocumento2 páginas23.07.2022 - Updated NITShalini BorkerAún no hay calificaciones

- WEST COAST COLL-WPS OfficeDocumento6 páginasWEST COAST COLL-WPS OfficeJan Kryz Marfil PalenciaAún no hay calificaciones

- BCG Capillary Whitepaper SEADocumento45 páginasBCG Capillary Whitepaper SEADeepak GahlawatAún no hay calificaciones

- Brochure - We Know BioprocessingDocumento20 páginasBrochure - We Know Bioprocessingclinton ruleAún no hay calificaciones

- McrsrvsDocumento4 páginasMcrsrvssubscribe enrollAún no hay calificaciones

- Case Study 1Documento4 páginasCase Study 1Arafat SanyAún no hay calificaciones

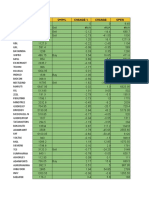

- Ticker LTP O H L Change % Change OpenDocumento22 páginasTicker LTP O H L Change % Change OpenPrasanna PharaohAún no hay calificaciones

- Project Controls Manager: Title: Role Profile ForDocumento2 páginasProject Controls Manager: Title: Role Profile ForhichemokokAún no hay calificaciones

- Data Privacy ActDocumento3 páginasData Privacy ActApril Krizzha PachesAún no hay calificaciones

- SWOT Pengembangan Udang WinduDocumento9 páginasSWOT Pengembangan Udang WinduSiska AmeliaAún no hay calificaciones

- Schwab Family ValuesDocumento18 páginasSchwab Family ValuesguingooAún no hay calificaciones

- Hei Initiative Pilot Call For ProposalsDocumento16 páginasHei Initiative Pilot Call For ProposalsSerbanoiu Liviu IonutAún no hay calificaciones

- Assignment (26 Batch)Documento6 páginasAssignment (26 Batch)Brand AtoZAún no hay calificaciones

- Mou Cum Agreement - NAPSDocumento6 páginasMou Cum Agreement - NAPSRanjit PandeAún no hay calificaciones

- Agency 2020 Mandocdoc MTDocumento8 páginasAgency 2020 Mandocdoc MTclperryAún no hay calificaciones

- Proposed Quality of An Enterprise Architecture Model: Abstract-Evaluation of EA Is Needed To Get MaximumDocumento5 páginasProposed Quality of An Enterprise Architecture Model: Abstract-Evaluation of EA Is Needed To Get MaximumpaulgAún no hay calificaciones

- Intermediate Accounting 18th Edition Stice Test BankDocumento33 páginasIntermediate Accounting 18th Edition Stice Test Bankcolonizeverseaat100% (35)

- Poppy Mirriam Mahlangu 2020-12!10!2021!03!10 StampedDocumento6 páginasPoppy Mirriam Mahlangu 2020-12!10!2021!03!10 StampedPoppyAún no hay calificaciones

- Horticulture Zimbabwe: Updated June 2012Documento8 páginasHorticulture Zimbabwe: Updated June 2012Blessmore Andrew ChikwavaAún no hay calificaciones

- Unified Opcrf For Schoolheads 2022-2023 - 012353Documento44 páginasUnified Opcrf For Schoolheads 2022-2023 - 012353Skul TV ShowAún no hay calificaciones

- Fulltext02 PDFDocumento82 páginasFulltext02 PDFKhaled ElshorbagyAún no hay calificaciones

- Technology of Machine Tools: Diamond, Ceramic, and Cermet Cutting ToolsDocumento44 páginasTechnology of Machine Tools: Diamond, Ceramic, and Cermet Cutting ToolsAnibal DazaAún no hay calificaciones

- Gender Neutral Toys DebateDocumento3 páginasGender Neutral Toys Debateapi-528782034Aún no hay calificaciones

- Database Assignment 1 Mohammed Shalabi 201810028Documento5 páginasDatabase Assignment 1 Mohammed Shalabi 201810028Mohammed ShalabiAún no hay calificaciones

- Pay Slip AugDocumento1 páginaPay Slip Augvictor.savioAún no hay calificaciones

- Answer 1 To 4Documento6 páginasAnswer 1 To 4MUHAMMAD BILAL RAZA SHAHZADAún no hay calificaciones