Documentos de Académico

Documentos de Profesional

Documentos de Cultura

Corporations

Cargado por

Cynthia AldayDescripción original:

Derechos de autor

Formatos disponibles

Compartir este documento

Compartir o incrustar documentos

¿Le pareció útil este documento?

¿Este contenido es inapropiado?

Denunciar este documentoCopyright:

Formatos disponibles

Corporations

Cargado por

Cynthia AldayCopyright:

Formatos disponibles

CORPORATIONS Prof.

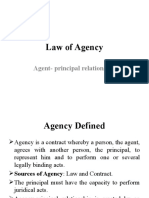

James Feinerman (Powerpoint Fall 2011) o Agency Principal and Agent Master and Servant; Independent Contractors o o o o o o o o o Agents As Fiduciaries Creation Of Authority -- General Rule Apparent Authority How Agencies Are Created Express agency Implied agency Ostensible agencies Agency by estoppel Agency by ratification Dual agency

of trust incident to that employment, even though those engaged in the practice of accountancy would regard as unusual the collecting and disbursing of a client's funds by an accounting firm. Reversed and remanded. Agent can impose liability upon his principal even where there is no actual or apparent authority or estoppel, as the agent may have an inherent agency power to bind his principal. General agent for disclosed or partially disclosed principal subjects his principal to liability for acts done on his account which usually accompany or are incidental to transactions which the agent is authorized to conduct if, although they are forbidden by the principal, the other party reasonably believes that the agent is authorized to do them and has no notice that he is not so authorized. If third person reasonably believes that service he has requested of member of an accounting partnership is undertaken as part of the partnership business, the partnership should be bound for breach of trust incident to that employment even though those engaged in the practice of accountancy would regard as unusual the performance of such service by an accounting firm. Reasonableness of third person's belief in assuming that partner is acting within scope of partnership should not be tested by profession's own description of the function of its members, but question must be answered upon basis of facts in particular case. In view of fact that it was reasonable for accounting firm client, who dealt exclusively with one partner of the firm, to assume that the added assignment she delegated to the partner of collecting and disbursing her funds delegated to the partner was an integral part of the proper functions of the partner who kept the accounts reflecting the income and disbursement of those funds, the accounting partnership was liable for the partner's breach of trust incident to that employment, even though those engaged in the practice of accountancy would regard as unusual the collecting and disbursing of a client's funds by an accounting firm. Accounting partnership client whose affairs were handled exclusively by one of the partners did not act unreasonably in trusting the partner further after learning of his unauthorized payment of the client's funds to the client's husband, and accordingly, client was not estopped from asserting against the partnership her claim for subsequent breaches of duty by the partner in paying out money to himself and to his client's husband.

Proof of Agency Authority of Agents Express authority Implied authority Delegation of agents authority Duties of an Agent Fiduciary duties Full disclosure Due care Loyalty Honesty Integrity Obedience Agents duty Fiduciary Duties Obedience Loyalty Disclosure Confidentiality Duty to Account Reasonable Care CROISANT V. WATRUD Suit in equity for an accounting brought against copartners in firm of certified public accountants and against executrix of a deceased partner. The Circuit Court rendered judgment in favor of defendants, and plaintiff appealed. The Oregon Supreme Court held that, in view of fact that it was reasonable for an accounting firm client, who dealt exclusively with one partner of the firm, to assume that the added assignment she delegated to the partner of collecting and disbursing her funds was an integral part of the proper functions of the partner who kept the accounts reflecting the income and disbursement of those funds, the accounting partnership was liable for the partner's breach

TARNOWSKI V. RESOP Action by principal against agent for damages which resulted when principal had been compelled, by agent's breach of duties, to sue third parties for rescission of sale on ground of fraud. The District Court entered judgment for plaintiff, and defendant appealed. The Minnesota Supreme Court held that election by principal to sue third parties for rescission did not bar action against agent to recover expenses and losses resulting from agent's wrongful conduct. Affirmed. All profits made by an agent in course of an agency belong to principal, whether they are fruits of performance or of violation of agent's duty, and it is immaterial that principal has suffered no damage, or even that transaction concerned was profitable to him. Where agent of buyer received secret commission from seller of business, election by buyer, upon discovery of fraud in transaction, to rescind contract of sale and recover from seller that with which he had parted, did not preclude subsequent action by buyer against his agent to recover secret commission obtained in violation of duties of agency. If agent has received benefit as result of violating his duty of loyalty, principal is entitled to recover from agent what he has so received, its value, or its proceeds, and also the amount of damage thereby caused, except that if violation consisted of wrongful disposal of principal's property, principal cannot recover its value and also what agent received in exchange therefor. A tort-feasor is answerable for all injurious consequences of his tortious act which, according to usual course of events and general experience, were likely to ensue and which, when the act was committed, might reasonably be supposed to have been foreseen and anticipated. Where violation by agent of buyer of fiduciary duties necessitated suit by buyer against sellers of business to recover amount with which buyer had parted as result of fraud, buyer was entitled to recover in separate suit against his agent, amount expended for attorney's fees and expenses of suit against seller, as well as such other expenses and losses which were direct consequence of agent's wrongful conduct. Dismissal of action by buyer against sellers for rescission of sale upon cash payment by sellers did not bar subsequent action by buyer against his agent to recover elements of damage in relation to sale transaction which were recoverable against agent and which were not involved in action for rescission. Directors and officers have a fiduciary duty to the corporation and its stockholders

Directors and officers have a fiduciary duty to the corporation and its stockholders. A mere employee of a corporation does not ordinarily occupy a position of trust or confidence, unless he is also its agent. Fiduciary duties result from the nature of the employment, and without any stipulation to that effect. No act of the directors, in violation of their own duties, and in fraud of the stockholders, will justify an officer in violating his fiduciary duties. The fiduciary duty extends to existing stockholders, but not to prospective stockholders, although, it has been held that the confidential relation extends not only to existing stockholders, but also to persons invited to purchase stock, and subscribers. The duty extends to pledgees of stock. It has been held both that directors and officers do and do not owe a fiduciary duty to individual shareholders, as distinct from the shareholders collectively. Where there is only one shareholder, a decision in the interest of that shareholder which does not harm any creditor is not a breach of the duty to the corporation. A shareholder may not complain of acts of corporate mismanagement if he acquired his shares from those who participated or acquiesced in the allegedly wrongful transactions. DUTIES -- LOYALTY In discharging their function of managing the business and affairs of the corporation, directors owe fiduciary duties of care and loyalty to the corporation. The duty of loyalty is a broad encompassing duty, that in appropriate circumstances, is capable of impressing a special obligation upon a director in any of his or her relationships with the corporation. The duty of loyalty mandates that the best interest of the corporation and its shareholders take precedence over any interest possessed by a director, officer or controlling shareholder and not shared by the shareholders generally. The duty of loyalty is fiduciary in nature, by reason of which the officer is held to something stricter than the morals of the market place. The duty obtains most directly when the officer is interested personally in a matter affecting the corporation. The concept of interest is broadly defined and includes cases where the officer has a relationship with a party to the transaction that may reasonably be expected to affect the officer's judgment or is subject to the influence and domination of such a party. Yet, the duty goes beyond this and is coextensive with the legitimate, enduring interests of the corporation. DUTIES - CARE In addition to their duty of loyalty, discussed in the previous slide, directors and officers of a corporation are required by law to perform their obligations in accordance with a minimum standard of care. Courts apply the duty of care in cases involving alleged 2

negligence, mismanagement, or intentional decisions to commit unlawful acts. Cases involving fraud, self-dealing, and conflicts of interest are covered under the duty of loyalty. The standard of care for directors and officers of business corporations is derived from common law and state business corporations codes. This standard is tempered by the business judgment rule (BJR), a common-law doctrine under which courts generally refuse to second-guess a business decision, so long as management made a reasonable effort to make an informed decision. We will examine many cases adumbrating the BJR, especially in the courts of Delaware. PARTNERSHIP Partnerships are governed both by common law and by statutory laws. Agency Concepts and Partnership Law: Each partner is deemed to be an agent of the other. There may be imputation of liability. Each partner is a fiduciary of the other. Law Governing Partnerships Partners are agents and fiduciaries of one another, but differ from agents in that they are also co-owners and share in profits and losses. Sources of Law: State common law. Uniform Partnership Act (UPA), adopted by all states in some form. Revised Uniform Partnership Act (RUPA): adopted by some states. Definition of Partnership Partnership is created when two or more persons agree to carry on business for profit as co-owners with equal right to manage and share profits (UPA). Disadvantages Partners are personally liable for all torts/contracts Dissolved upon death Difficult to raise financing

The Nature of Partnerships At common law, the partnership was not a separate legal entity from its owners. Today, partnership law in many states recognizes a partnership as an independent entity for some purposes. Partnership as an Entity Today, many states recognize the partnership as a separate legal entity for the following purposes: To sue and be sued (for federal questions, yes; for state questions, differs). To have judgments collected against its assets, and individual partners assets. Partnerships are recognized as separate legal entities (contd): To own partnership property. To convey partnership property. At common law -- property owned in tenancy in partnership, all partners had to be named and sign the conveyance. Under UPA partnership property can be held and sold in firm name. Partnership as an Entity [3] Partnerships are recognized as separate legal entities (contd): For marshaling of assets. Federal Bankruptcy changes marshaling of assets. To keep its own books. File its own federal/state tax returns. Aggregate Theory of Partnership. Partnership pays no federal income tax. MARTIN V. PEYTON Partnership results from contract, express or implied. Where contract as a whole contemplates association of two or more persons to carry on business for profit as co-owners, there is partnership, notwithstanding statement that no partnership is intended, in view of Partnership Law. A contract which, taken as a whole, contemplates anything less than an association of two or more persons to carry on as co-owners a business for profit does not create a partnership. In determining whether contract between parties creates partnership, arrangement for sharing profits should be considered and given due weight, but it is not decisive, since it may be merely method adopted to pay debt or wages, interest on loan, or for other reasons. Agreement expressed in three documents, whereby securities were loaned to partnership and lenders acquired supervisory powers with option to enter firm and to accept resignation of any member, held not to create partnership. Where written contract between parties is complete and expresses in good faith full understanding and obligation of parties, it is for court to say whether partnership exists. 3

Advantages Easy to create and maintain Flexible, informal Partners share profits and losses equally

Definition of Partnership If a commercial enterprise shares profits and losses a partnership will be inferred. Exceptions: Partnership not inferred if profits received as payment in the following situations: Debt by installments of interest on a loan. Wages of an employee. Rent to a landlord. Annuity to a widow or representative of a deceased partner. Sale of good will.

NATIONAL BISCUIT CO., INC. V. STROUD Proceeding by seller of bread against former partners who had operated food store for value of goods sold and delivered. The Superior Court rendered judgment for seller, and partner appealed. The Supreme Court majority held that purchase of bread by food store operated as going concern by two partners was an ordinary matter connected with partnership business within statute to effect that any difference arising as to ordinary matter connected with partnership business may be decided by majority of partners, and although partner told bread seller he would not be personally responsible for additional bread sold to store, partner and partnership were liable for such purchase by copartner. Affirmed. Rodman, J., dissented. At the close of business on 25 February 1956 Stroud and Freeman by agreement dissolved the partnership. By their dissolution agreement all of the partnership assets, including cash on hand, bank deposits and all accounts receivable, with a few exceptions, were assigned to Stroud, who bound himself by such written dissolution agreement to liquidate the firm's assets and discharge its liabilities. It would seem a fair inference from the agreed statement of facts that the partnership got the benefit of the bread sold and delivered by plaintiff to Stroud's Food Center, at Freeman's request, from 6 February 1956 to 25 February 1956. But whether it did or not, Freeman's acts bound the partnership and Stroud. MEINHARD V. SALMON A joint venture with terms embodied in a writing. Meinhard was to pay to Salmon half of the money requisite to reconstruct, alter, manage, and operate the property. Salmon was to pay to Meinhard 40 per cent of the net profits for the first five years of the lease and 50 per cent for the years thereafter. If there were losses, each party was to bear them equally. Salmon, however, was to have sole power to 'manage, lease, underlet and operate' the building. There were to be certain pre-emptive rights for each in the contingency of death. They were coadventurers, subject to fiduciary duties akin to those of partners. Questions What was Meinhards theory of liability? What was the basis of Salmons defense? (Hint: difference between partnership and joint venture); Why did Cardozo side with Meinhard? In particular, where did Salmon go wrong? Hypotheticals Suppose Salmon disclosed Gerrys proposal to Meinhard, but then competed vigorously with Meinhard for the contract and won. Result? Suppose the new lease was for different plot of land

and hadnt come from Gerry. Result? What if Salmon could prove that Gerry hated Meinhard, and wouldnt have dealt with him? What if the opportunity came to Meinhard (the silent partner)? What if they both managed? Rationale for the Outcome? Does this holding make sense from a property rights perspective? Does outcome support both parties investment backed expectations of their property rights? What about from a contractarian perspective? How long do you think Meinhard & Salmon envisioned their relationship lasting? Suppose M & S anticipated this potential contingency in April of 1902. Would they have favored a rule mandating disclosure by Salmon? Fiduciary Duty Judge Cardozos words Many forms of conduct permissible in a workaday world for those acting at arms length, are forbidden to those bound by fiduciary ties. A trustee is held to something stricter than the morals of the market place. Not honesty alone, but the punctilio of an honor the most sensitive, is thenthe standard of behavior. How did Salmon breach his fiduciary duty to Meinhard? Elf Atochem North America, Inc. v. Jaffari and Malek Member of limited liability company (LLC) brought purported derivative suit against LLC and its manager, alleging, inter alia, breach of fiduciary duty. The Court of Chancery dismissed suit for lack of subject matter jurisdiction. Member appealed. The Delaware Supreme Court held that: (1) limited liability company was bound by agreement defining its governance and operation, even though company did not itself execute agreement, and (2) contractual provisions directing that all disputes be resolved exclusively by arbitration or court proceedings in California were valid under Limited Liability Company Act. A limited liability company agreement will only be invalidated when it is inconsistent with mandatory statutory provisions Limited liability company was bound by agreement defining its governance and operation, and derivative claims brought on its behalf were therefore subject to arbitration and forum selection clauses of the agreement, even though the agreement was only signed by the members and not by the company, itself. In the corporate context, the derivative form of action permits an individual shareholder to bring suit to enforce a corporate cause of action against officers, 4

directors and third parties. The derivative suit is a corporate concept grafted onto the limited liability company form. Members of a limited liability company may contract to avoid the applicability of statutory provisions giving Court of Chancery subject matter jurisdiction over certain claims. While Limited Liability Company Act allowed members of limited liability company to bring actions involving removal of managers and interpretation of limited liability company agreements in the Court of Chancery, it did not afford Court of Chancery special jurisdiction to adjudicate member's breach of fiduciary duty and removal claims despite a clear contractual agreement to the contrary. DUTIES AND LIABILITIES OF AGENT TO PRINCIPAL

District Court certified a question to the Supreme Court. The Supreme Court held that the equitable remedy of piercing the veil is an available remedy under the Limited Liability Company Act. N.B. Advisory Opinion (Certified question answered). Available in STATE court!

As a general rule, a corporation is a separate entity distinct from the individuals comprising it. Piercing the corporate veil is an equitable doctrine. The concept of piercing the corporate veil is a judicially-created remedy for situations where corporations have not been operated as separate entities as contemplated by statute and, therefore, are not entitled to be treated as such. COMMON BUSINESS ENTITIES

376. General Rule The existence and extent of the duties of the agent to the principal are determined by the terms of the agreement between the parties 377. Contractual Duties A person who makes a contract with another to perform services as an agent for him is subject to a duty to act in accordance with his promise 379. Duty Of Care And Skill Unless otherwise agreed, a paid agent is subject to a duty to the principal to act with standard care and with the skill which is standard. 381. Duty To Give Information 382. Duty To Keep And Render Accounts 383. Duty To Act Only As Authorized 385. Duty To Obey 386. Duties After Termination Of Authority Duties Of Loyalty 387. General Principle Unless otherwise agreed, an agent is subject to a duty to his principal to act solely for the benefit of the principal in all matters connected with his agency 388. Duty To Account For Profits Arising Out Of Employment 389 390 Acting As Adverse Party Without (With) Principal's Consent 391 392 Acting For Adverse Party Without (With) Principal's Consent 393 396 Competition, Conflicts of Interest, Uses of Confidential Information during and after Agency

Sole Proprietorship Partnership S Corporation C Corporation Limited Liability Company Single Member Limited Liability Company Factors to Consider in Selecting an Appropriate Business Entity Liability - Limited Liability v. Personal Liability Tax Implications Complexity of Formation and Management Capital - effect on ability to raise capital through angel investment, venture capital, or initial public offering (IPO) Credibility in the business world Sole Proprietorship An individual (or husband and wife team) carrying on a business for profit Unlimited personal liability Single level of income tax - all income and expense items reported on Schedule C of the owners 1040 Relatively simple to start If business conducted other than under the name of the sole proprietor, assumed name publication needed Managed by the sole proprietor Any transfer of the business would be of the underlying assets as opposed to a transfer of shares in the business Capital needs - addressed through loan to sole proprietor General Partnership Association of two or more co-owners carrying on business for profit Partners have unlimited personal liability for partnership debts 5

KAYCEE LAND AND LIVESTOCK v. FLAHIVE Landowner brought action for damages against limited liability company (LLC) and its managing member, alleging that the LLC had caused environmental damage to the land when exercising its contractual right to use the surface of the land. The

Pass through tax treatment (partnership files form 1065 but all income and expense items pass through to individual partners on schedule K-1) Relatively easy to start - partnership agreement is typically entered into but is not legally required Managed by the partners or as described in the partnership agreement; Problem: any partner can bind the partnership Ability to raise capital limited since most investors would prefer to invest in an entity offering limited liability LLC is almost always the better choice if partnership tax treatment is the goal S Corporation Limited liability for shareholders even if they participate in management Pass-through tax treatment under most circumstances but not as complete as for the LLC Formation steps include filing Articles of Incorporation with the Secretary of State, filing sub S election with the IRS, adoption of bylaws, and, usually, adoption of a shareholder (buy-sell) agreement Limitations on the number of shareholders and the type of shareholders limits ability to raise capital Limit of 75 shareholders Only one class of stock is allowed so ability to give priority return of capital to investors compromised Differences in voting rights is allowed Partnerships and corporations cannot be shareholders Only citizens or residents of USA can be shareholders Is easier to convert S corp to C corp than it is LLC to C corp in event venture capital is sought C Corporation Limited liability for shareholders even if they participate in mgmt Tax at both corporate and shareholder level. This double level tax can be avoided to some extent by payment of reasonable salaries to shareholders in exchange for services actually rendered Formation similar to S corporation except sub S election not filed with IRS Typically required for publicly traded corporations, businesses that require venture capital, or if a broad based stock option program is utilized No limits on type or numbers of shareholders Different classes of stock allowed thus enabling different priority for return of capital Common Stock Preferred Stock Limited Liability Company Combines limited liability provided by a corporation with pass-through partnership tax treatment LLC files a partnership tax return with all income and expenses being passed through to individual owners of the

LLC Formation steps include filing articles of organization with the Secretary of State, contributing an appropriate amount of capital, and adopting an operating agreement Can be managed by the members or, more often, by managers selected by the members. Can also elect officers Self-employment tax treatment less favorable than for S corporation Offers several advantages over the S corporation: 1. No limitation on the number of members 2. No limitation on who may invest (corporations, partnerships, and non US residents can invest) 3. Treatment of gain on distribution of appreciated property more favorable 4. Different classes of ownership are allowed so there is the flexibility to provide for a priority return of capital to investors Single-Member Limited Liability Company Limited liability for owners makes it a better choice than a sole proprietorship unless cost of formation or maintenance is a controlling factor Disregarded entity from an income tax perspective All income and expenses are reported on the sole members tax return and no income tax return need be filed by the LLC Formation process similar to multiple-member LLC, except that the operating agreement will likely be less complex In addition to circumstances where a sole proprietorship would be considered, a single-member LLC is often used by a corporation or LLC to insulate the liability associated with a particular line of business DODGE v. FORD MOTOR CO. A business corporation is organized primarily for the profit of the stockholders, and the discretion of the directors is to be exercised in the choice of means to attain that end, and does not extend to the reduction of profits or the non-distribution of profits among stockholders in order to benefit the public, making the profits of the stockholders incidental thereto. Where a corporation had on hand about $54,000,000 cash with a constant income of over $60,000,000 per year profits, and proposed improvements and extensions would not exceed $24,000,000, the court did not err in requiring that directors declare an extra dividend of $19,000,000, in an action by minority stockholders. Where a corporation had a surplus of $112,000,000, about $54,000,000 cash on hand, and had made profits of $59,000,000 in the past year with expectations of $60,000,000 the coming year, refusal of directors to declare a dividend of more than $1,200,000 was, in the absence of some 6

justifiable reason, an arbitrary exercise of authority which would give a court of equity the right to interfere. BUT It is a well-recognized principle of law that the directors of a corporation, and they alone, have the power to declare a dividend of the earnings of the corporation, and to determine its amount. Courts of equity will not interfere in the management of the directors unless it is clearly made to appear that they are guilty of fraud or misappropriation of the corporate funds, or refuse to declare a dividend when the corporation has a surplus of net profits which it can, without detriment to its business, divide among its stockholders, and when a refusal to do so would amount to such an abuse of discretion as would constitute a fraud, or breach of that good faith which they are bound to exercise towards the stockholders.'

More than half a million business entities have their legal home in Delaware including more than 50% of all U.S. publicly-traded companies and 58% of the Fortune 500 Corporate Chartering in US Federalism Federal Government Regulates Stock Offerings, Protects Investors, and Sets Standards for Financial Disclosures State Governments Regulate Corporation Actions Under Civil and Common Law Regimes State of Incorporation Very Important Why Delaware? First mover advantage History lesson on Incorporations Primary Corporate Market has been in New York as Commercial Capital of US th In late 19 Century States Began to Experiment with Corporate Law to become more flexible in regulating incorporations and rules governing the separation of ownership and management New Jersey was the first successful state to move into corporate charter business Delaware entered into the market after New Jersey enacted a series of anti-trust laws Delaware Law Features Allows flexibility of drafting corporate charters Law sets basic structure Respecting the right to free contract Shareholder franchise Board initiation Basic Principles duty of due care to shareholders duty of loyalty duty of good faith Delaware Who decides? Delaware Court of Chancery Delaware's court of original and exclusive equity jurisdiction, and adjudicates a wide variety of cases involving trusts, real property, guardianships, civil rights, and commercial litigation Delaware Supreme Court Delaware's court of final appeal to which appeals from the Delaware Court of Chancery immediately proceed Institutions are Important! Courts and regulators have played an important role to ensure that corporate governances mechanisms are effective and efficient Management, General Directors, CEOs, Individual directors and the board as a whole need to be held to their duties of care and loyalty to the firm and to apply business judgment in their decisions 7

A. P. SMITH MFG. CO. v. BARLOW Action brought by corporation for judgment declaring its contribution to a privately supported educational institution to be within its powers, where defendants asked for judgment declaring the contribution to be a misappropriation of corporate funds and an ultra vires act in violation of property and contract rights of defendants and of other stockholders of the plaintiff corporation. The Superior Court, Chancery Division, held the donation to be intra vires. An appeal taken to the Appellate Division was certified directly to the Supreme Court which held that the corporate power to make reasonable charitable contributions exists under modern conditions even apart from express statutory provisions. Where justified by advancement of public interest, reserved power of State to alter corporate charter may be invoked to sustain later charter alterations even though they affect contractual rights between corporations and its stockholders and between stockholders Charitable contribution statutes were within powers reserved by State in granting corporate charter, and therefore such statutes did not unconstitutionally impair obligations of charter of pre-existing corporations or operate as a deprivation of property without due process of law Corporate power to make reasonable charitable contributions exists, under modern conditions, even apart from express statutory provision. Thus, a business corporation's contribution of funds for general maintenance of privately supported educational institution was not an ultra vires act. Delaware Corporate Governance Influence Why is Delaware Important? State based incorporation statues of the US Delaware Corporate Law tradition Delawares Corporate Registry

The strength of a joint stock company in a market system is the underlying principles of rule of law and fairness to the interest of all stockholders Delaware Code General Corporation Law Subchapter IV. Directors and Officers 141. Board of directors; powers; number, qualifications, terms and quorum; committees; classes of directors; nonprofit corporations; reliance upon books; action without meeting; removal (a) The business and affairs of every corporation organized under this chapter shall be managed by or under the direction of a board of directors, except as may be otherwise provided in this chapter or in its certificate of incorporation. If any such provision is made in the certificate of incorporation, the powers and duties conferred or imposed upon the board of directors by this chapter shall be exercised or performed to such extent and by such person or persons as shall be provided in the certificate of incorporation.

CAMPBELL V. LOEW'S, INC. Action by a stockholder against a corporation, where stockholder requested a preliminary injunction restraining the holding of a stockholders' meeting, or alternatively, restraining the meeting from considering certain matters, or voting certain proxies. The Court of Chancery held, inter alia, that in view of fact bylaws of corporation authorized president to call special meetings of the stockholders for any purpose or purposes, president of the corporation was authorized to call a stockholders' meeting to fill director vacancies, amend the bylaws to increase the number of the board of directors, and to remove certain directors and fill such vacancies, even though such purposes were not in furtherance of routine business of corporation, and notwithstanding fact that such matters might have involved policy matters not defined by the board of directors, and therefore, court would not issue a preliminary injunction enjoining the holding of such meeting. A corporate bylaw giving corporate president the power to submit matters for stockholder action, could be presumed to only embrace matters which were appropriate for stockholder action, and so construed, such bylaw would not be deemed to impinge upon statutory right and duty of a corporate board of directors to manage the business of the corporation. Call of a stockholders' meeting, by corporate president, to fill director vacancies, to amend the bylaws to increase the number of the board, and remove certain directors and fill such vacancies, was not action of a character which impinged upon power of management given board of directors by statute.

Where corporate bylaws authorized president to call a stockholders' meeting for any purpose, mere fact that another section of the bylaws provided that stockholders might, on their initiative, call a meeting for the purpose of filling vacancies on board of directors, did not mean that president was deprived of power to call a stockholders' meeting for such purpose. Statute providing that not only vacancies, but newly created directorships of a corporation may be filled by majority of directors in office, unless it is otherwise provided in the certificate of incorporation, or by-laws, is not exclusive and does not prevent stockholders from filling new directorships between annual meetings. The board of directors of a corporation, acting as a board, must be recognized as the only group authorized to speak for "management" in the sense that by statute, they are responsible for the management of the corporation. Where a certain corporate faction was in charge of a corporation's facilities, and symbolized existing policy, it had sufficient status to justify reasonable use of corporate funds to present its position to the stockholders, and to expend reasonable sums of corporate funds in solicitation of proxies, although, to assure equal treatment between such faction and opposing faction in event of a proxy contest, such faction would be enjoined from using corporate facilities and employees in connection with its proxy solicitation. PIERCING THE CORPORATE VEIL

In General - Personal Liability for Corporate Debt Non-functioning of other officers and directors Siphoning of funds Absence of corporate records Corporation acts as faade for owners/shareholders Elements of injustice or fundamental unfairness General rule: The rule is the court may disregard the corporate entity if 1. there is Fraud or 2. Alter Ego Doctrine Unity of Interest: there is such a unity of interest and ownership such that the separate personalities of the corporation and the individual no longer exist the company is "a mere instrumentality or alter ego of its owner, and Injustice: Allowing shareholder to avoid liability would promote an injustice

Perception v. Reality Perception It is nearly impossible to pierce the corporate veil. Because limited liability holds such an esteemed place in our law, courts frequently opine that their power to pierce the veil should be exercised reluctantly, cautiously, or only in exceptional circumstances. 8

A Colorado Example: Insulation from individual liability is an inherent purpose of incorporation; only extraordinary circumstances justify disregarding the corporate entity to impose personal liability. Leonard v. McMorris, 63 P.3d 323 (Colo. 2003). Reality Courts will pay homage to the exceptional circumstances tradition, but do what they believe is right. An analysis of nearly 1,600 reported decisions revealed that courts pierced the corporate veil more than 40% of the time. Thompson, Piercing the Corporate Veil: An Empirical Study, 76 Cornell L.Rev. 1036 (1991). Development of the Piercing Doctrine When a plaintiff has a valid cause of action against an insolvent corporation, the Court must weigh two competing values. The first is societys desire to uphold the principle of limited liability, and the second is the desire to achieve an equitable outcome. Early decisions relied on equitable principles, and typically involved allegations of fraud. See, Booth v. Bunce, 33 N.Y. 139 (1865) General Rule If any general rule can be laid down, in the present state of authority, it is that a corporation will be looked upon as a legal entity as a general rule, and until sufficient reason to the contrary appears; but, when the notion of legal entity is used to defeat public convenience, justify wrong, protect fraud, or defend crime, the law will regard the corporation as an association of persons. A Remedy Not a Cause of Action Most Courts hold that piercing the corporate veil is an equitable remedy not a cause of action. Piercing the corporate veil is an equitable remedy, requiring balancing of the equities in each particular case. Great Neck Plaza, L.P. v. Le Peep Restaurants, LLC, 37 P.3d 485 (Colo. App. 2001); See also, Equinox Enterprises, Inc. v. Associated Media Inc., 730 SW2d 872 (Tex. App. 1987) BERKEY v. THIRD AVE. RY. CO.

required to be complete, in order for the parent company to be treated as liable for the debts of the subsidiary. It was needed that the subsidiary be merely the alter ego of the parent, or that the subsidiary be thinly capitalized, so as to perpetrate a fraud on the creditors. BARTLE v. HOME OWNERS COOPERATIVE Action to compel corporation to meet obligations of its subsidiary. The Supreme Court, Appellate Division, affirmed judgment of Supreme Court, Equity Term, dismissing complaint, and plaintiffs appealed. The Court of Appeals held that trustee of bankrupt subsidiary corporation could not maintain action to compel parent corporation to meet obligations of its subsidiary, where there had been neither fraud, misrepresentation nor illegality involved in incorporation of such subsidiary or its subsequent operation. Judgment affirmed. Doctrine of piercing corporate veil is invoked to prevent fraud or to achieve equity. The law permits incorporation of a business for very purpose of escaping personal liability. Trustee of bankrupt subsidiary corporation could not maintain action to compel parent corporation to meet obligations of such subsidiary, where there had been neither fraud, misrepresentation nor illegality involved in incorporation of such subsidiary or its subsequent operation. WALKOVSZKY v. CARLTON Action against corporation in name of which a taxicab was registered, driver of the taxicab, nine other corporations in whose names other taxicabs were registered, two additional corporations, and three individuals for injuries sustained by plaintiff when struck by the taxicab. The Supreme Court granted motion of an individual defendant who was claimed to be a stockholder of ten corporations, including corporation in name of which taxicab was registered, to dismiss the complaint as to him for failure to state a cause of action, and plaintiff appealed. The Supreme Court, Appellate Division reversed and denied the motion and individual defendant appealed by leave of the Appellate Division on a certified question. The Court of Appeals held that complaint containing allegations that individual defendant organized, managed, dominated and controlled a fragmented corporate entity and that fleet ownership of taxicabs had been deliberately split among many corporations was insufficient to state a cause of action against individual defendant as a stockholder in such corporations, where there was no allegation that individual defendant was conducting such business in his individual capacity. Order of Appellate Division reversed, certified queston answered in the negative, order of the Supreme Court, Richmond County, reinstated with 9

Actions by Minnie Best Berkey and Charles P. Berkey against the Third Avenue Railway Company, from an order of the Appellate Division reversing a judgment of the Trial Term, which dismissed complaints, and granting new trial, defendant appealed. Order reversed, and judgment of the Trial Term affirmed. The New York Court of Appeals held that the Third Avenue Railway Co was not liable for the debts of the subsidiary. It was necessary that the domination of the parent company over the subsidiary was

leave to serve an amended complaint. Courts will disregard the corporate form or pierce the corporate veil whenever necessary to prevent fraud or to achieve equity. Incorporation of a business is permitted for the purpose of enabling its proprietors to escape personal liability, although the privilege is not without limits. In determining whether liability should be extended to reach assets beyond those belonging to the corporation, courts will be guided by general rules of agency. Whenever anyone uses control of a corporation to further his own rather than the corporation's business, he will be responsible for the corporation's acts upon principle of respondeat superior applicable even where the agent is a natural person, and such liability extends not only to the corporation's commercial dealings, but to its negligent acts. Although either the circumstance that a corporation is a fragment of a larger corporate combine which actually conducts a business, or that a corporation is a dummy for its individual stockholders who in reality are carrying on a business in their own personal capacities for purely personal rather than corporate ends would justify treating the corporation as an agent and piercing the corporate veil to reach the principal, in the first circumstance only a larger corporate entity could be held financially responsible, while in the other circumstance the stockholders would be personally liable. In ascertaining whether a complaint states a cause of action, the entire pleading must be considered. Complaint containing allegations that an individual defendant organized, managed, dominated and controlled a fragmented corporate entity and that fleet ownership of taxicabs had been deliberately split among many corporations was insufficient to state a cause of action in tort against individual defendant as a stockholder in such corporations, where there was no allegation that individual defendant was conducting business in his individual capacity. The corporation form could not be disregarded merely because the assets of corporate owner of a taxicab together with mandatory insurance coverage on the taxicab which struck plaintiff were insufficient to assure plaintiff recovery sought.

MORRIS V. NEW YORK STATE DEPT. OF TAXATION AND FINANCE Board member of corporation brought action for judicial review of determination of Tax Appeals Tribunal regarding compensating use tax assessment. The Supreme Court, Appellate Division confirmed. Board member appealed. The Court of Appeals held that corporate veil could not be pierced so as to hold board member personally liable for compensating use taxes allegedly incurred by corporation.

Concept of "piercing the corporate veil" is limitation on accepted principles that corporation exists independently of its owners as separate legal entity, that owners are normally not liable for debts of corporation, and that it is perfectly legal to incorporate for express purpose of limiting liability of corporate owners. Attempt of third party to pierce the corporate veil does not constitute cause of action independent of that against corporation; rather it is assertion of facts and circumstances which will persuade court to impose corporate obligations on its owners. Although there are no definitive rules governing circumstances when corporate veil may be pierced, generally showing is required that: (1) owners exercised complete domination of corporation in respect to transaction attacked; and (2) such domination was used to commit fraud or wrong against plaintiff which resulted in plaintiff's injury. While complete domination of corporation is key to piercing corporate veil, especially when owners use corporation as mere device to further personal rather than corporate business, such domination, standing alone, is not enough; some showing of wrongful or unjust act toward plaintiff is required. Party seeking to pierce corporate veil must establish that owners, through their domination, abused privilege of doing business in corporate form to perpetrate wrong or injustice against that party such that court in equity will intervene. Even assuming that sole board member of closely held corporation owned by board member's brother and nephew dominated corporation, corporate veil could not be pierced so as to hold board member personally liable for compensating use taxes allegedly incurred by corporation; there was no evidence of intent to defraud and thus board member did not misuse corporate form for personal ends so as to commit wrong or injustice on taxing authorities, and there was no corporate obligation to be imposed on board member since corporation was entitled to nonresident exemption and thus owed nothing. Even if federal rule, recognizing that corporation may have separate taxable identity, were to be applied to question of whether corporate veil should be pierced so that sole board member of closely held corporation could be held personally liable for compensating use tax allegedly incurred by corporation, board member would not be liable since corporation had legitimate business purpose of owning and chartering boats, and there was no evidence that corporation was set up as sham or for purpose of tax avoidance.

UNITED STATES v. BESTFOODS Compensation and Liability Act (CERCLA) against parent corporations of chemical manufacturers for costs of cleaning up industrial waste generated by chemical plant. The United States District Court for the Western District of Michigan imposed operator 10

liability on parent corporations. On appeal, the Court of Appeals for the Sixth Circuit reversed in part. After grant of certiorari, the Supreme Court held that: (1) when the corporate veil may be pierced, a parent corporation may be charged with derivative CERCLA liability for its subsidiary's actions; (2) a participation-and-control test looking to the parent corporation's supervision over subsidiary cannot be used to identify operation of a facility resulting in direct parental liability under CERCLA; and (3) direct parental liability under CERCLA's operator provision is not limited to a corporate parent's sole or joint venture operation with subsidiary. Judgment of Court of Appeals vacated and case remanded with instructions. It is a general principle of corporate law deeply ingrained in our economic and legal systems that a "parent corporation," so-called because of control through ownership of another corporation's stock, is not liable for the acts of its subsidiaries. The exercise of the control which stock ownership gives to the stockholders will not create liability on the part of parent corporation for acts of subsidiary beyond the assets of the subsidiary, with "control" including the election of directors, the making of bylaws, and the doing of all other acts incident to the legal status of stockholders. Duplication of some or all of the directors or executive officers will not create liability on part of parent corporation for acts of subsidiary, beyond the assets of the subsidiary. Corporate veil may be pierced and the shareholder held liable for the corporation's conduct when, inter alia, the corporate form would otherwise be misused to accomplish certain wrongful purposes, most notably fraud, on the shareholder's behalf. CERCLA gives no indication that the entire corpus of state corporation law is to be replaced simply because a plaintiff's cause of action is based upon a federal statute, and the failure of the statute to speak to a matter as fundamental as the liability implications of corporate ownership demands application of the rule that in order to abrogate a common-law principle, the statute must speak directly to the question addressed by the common law. When, but only when, the corporate veil may be pierced, a parent corporation may be charged with derivative CERCLA liability for its subsidiary's actions. If a subsidiary that operates, but does not own, a facility is so pervasively controlled by its parent for a sufficiently improper purpose to warrant veil piercing, the parent may be held derivatively liable under

CERCLA for the subsidiary's acts as an operator. District court's focus on the relationship between parent corporation which disputed direct CERCLA operator liability and its subsidiary, rather than on the parent and the subsidiary's polluting facility, combined with the court's automatic attribution of the actions of dual officers and directors to the corporate parent, erroneously, even if unintentionally, treated CERCLA as though it displaced or fundamentally altered common law standards of limited liability. THE DUTY OF CARE

The duty of care requires that directors make decisions based upon reasonably adequate information and deliberation Discharge duties with the care that an ordinarily prudent person in a like position would exercise under similar circumstances; Discharge duties in a manner they reasonably believe is in the best interest of the corporation. Requires the directors to attend board meetings; obtain and review adequate information concerning actions taken by the board; and generally supervise the corporations business and its major policies THE BUSINESS JUDGMENT RULE The business judgment rule is a presumption of the courts that in making a business decision the directors fulfill their fiduciary duties of care and loyalty to the corporation by: Acting on an informed basis; In good faith; In the honest belief that the decision was in the best interest of the company. APPLICATION OF THE BUSINESS JUDGMENT RULE The business judgment rule protects only informed decisions To come under the rules of protection, directors must inform themselves of all information reasonably available to them and relevant to their decision; The proper standard for determining whether a business judgment was an informed one is gross negligence. The Business Judgment Rule does not protect the directors when they have either abdicated their functions or failed to act THE DUTY OF CARE The duty of care requires that directors make decisions based upon reasonably adequate information and deliberation Discharge duties with the care that an ordinarily prudent person in a like position would exercise 11

under similar circumstances; Discharge duties in a manner they reasonably believe is in the best interest of the corporation. Requires the directors to attend board meetings; obtain and review adequate information concerning actions taken by the board; and generally supervise the corporations business and its major policies THE BUSINESS JUDGMENT RULE The business judgment rule is a presumption of the courts that in making a business decision the directors fulfill their fiduciary duties of care and loyalty to the corporation by: Acting on an informed basis; In good faith; In the honest belief that the decision was in the best interest of the company. APPLICATION OF THE BUSINESS JUDGMENT RULE The business judgment rule protects only informed decisions To come under the rules of protection, directors must inform themselves of all information reasonably available to them and relevant to their decision; The proper standard for determining whether a business judgment was an informed one is gross negligence. The Business Judgment Rule does not protect the directors when they have either abdicated their functions or failed to act FRANCIS v. UNITED JERSEY BANK Action was brought by trustees in bankruptcy of corporation to recover funds paid by corporation to principal stockholder for benefit of his estate, and to members of his family. After judgment was entered in favor of plaintiffs, the Superior Court denied motion for new trial or alternatively for amendment to judgment, and appeal was taken. The Superior Court, Appellate Division affirmed and administrator and executrix of estate appealed. The Supreme Court held that decedent was negligent in not noticing and trying to prevent misappropriation of funds held by corporation in an implied trust and her negligence was proximate cause of trustees' losses. Affirmed. As a general rule, a corporate director should acquire at least a rudimentary understanding of business of corporation and accordingly, a director should become familiar with fundamentals of business in which corporation is engaged and because directors are bound to exercise ordinary care, they cannot set up as a defense lack of knowledge needed to exercise the requisite degree of care and if one feels that he has not had sufficient

business experience to qualify him to perform the duties of a director, he should either acquire the knowledge by inquiry, or refuse to act. Directors of corporations are under continuing obligation to keep informed about activities of corporation; otherwise, they may not be able to participate in overall management of corporate affairs. Shareholders have right to expect that directors will exercise reasonable supervision and control over policies and practices of a corporation Corporate directors may not shut their eyes to corporate misconduct and then claim that because they did not see the misconduct, they did not have a duty to look Directorial management of corporation does not require a detailed inspection of day-to-day activities but, rather, a general monitoring of corporate affairs and policies and accordingly, a director is well advised to attend board meetings regularly. While directors of corporations are not required to audit corporate books, they should maintain familiarity with financial status of corporation by regular review of financial statements and, in some circumstances, directors may be charged with assuring that bookkeeping methods conform to industry custom and usage. Corporate director was personally liable in negligence for failure to prevent misappropriation of trust funds by other directors who were also officers and shareholders of the corporation where negligence was proximate cause of loss. Usually a corporate director can absolve himself from liability by informing the other directors of impropriety and voting for proper course of action; conversely, a director who votes for or concurs in certain actions may be liable to the corporation for the benefit of its creditors or shareholders, to the extent of any injuries suffered by such persons, respectively, as a result of such action. In most instances an objecting director whose dissent is noted in accordance with applicable statute will be absolved after attempting to persuade fellow directors to follow different course of action. Director is not an ornament, but an essential component of corporate governance; consequently, a director cannot protect himself behind a paper shield bearing the motto, "dummy director." NURSING HOME BUILDING CORPORATION v. DeHART Action was brought by corporate nursing home against former sole shareholders of corporation for alleged fraudulent misappropriation of corporate funds. The Superior Court, King County entered judgment for plaintiff for $9,914.85, an obligation conceded by defendants, and plaintiff appealed. The Court of Appeals held that former shareholders were not liable to corporate nursing home for disbursements, which were ratified by all shareholders, of corporate assets to sellers of 12

corporate stock as installment payments for purchase of stock, that evidence supported finding that challenged expenditures by former sole shareholders were made by such shareholders within scope of proper exercise of their business judgment in running corporate nursing home, and that evidence supported finding that use of corporate funds by former sole shareholders for payment of expenses other than taxes constituted valid exercise of business judgment. Affirmed. Corporation's separate legal identity is not lost merely because all of its stock is held by members of single family or by one person and thus fact of sole ownership does not of itself immunize sole shareholder from liability to corporation, but corporate entity will be disregarded when justice so requires. Courts should be reluctant to interfere with internal management of corporations and should generally refuse to substitute their judgment for that of directors. "Business judgment rule (BJR) immunizes management from liability in corporate transaction undertaken within both power of corporation and authority of management where there is reasonable basis to indicate that transaction was made in good faith. Evidence, in action brought by corporate nursing home against former sole shareholders of corporation for alleged fraudulent misappropriation of corporate funds, supported finding that challenged expenditures by former sole shareholders, who were experienced in operation of various types of businesses including nursing homes and who were involved in day to day management of corporate nursing home on full time or greater basis, were made by such shareholders within scope of proper exercise of their business judgment. Evidence in action brought by corporate nursing home against former sole shareholders of corporation for alleged fraudulent misappropriation of corporate funds supported finding that use of corporate funds by former sole shareholders for payment of expenses other than taxes constituted valid exercise of business judgment as to which court would not interfere in absence of bad faith or fraud. Where disbursements of installment payments for purchase of stock were made with corporate assets by former sole shareholders of corporate nursing home and such disbursements were ratified by all shareholders, former sole shareholders were not liable to corporation for such installment payments. Where contract for sale of stock was executed by all parties, including corporate nursing home, contract provided that asset of corporation would be assigned to sellers of stock, corporation approved contract at time when sellers were sole shareholders and constituted majority of board of directors, and all parties consented to and ratified assignment of such

contract, ratification of such transaction by all parties in accordance with stock purchase contract was binding on corporation and thus former sole shareholders who purchased stock from sellers were not liable to corporation for their subsequent transfer of such asset. SMITH v. VAN GORKOM Class action was brought by shareholders of corporation, originally seeking rescission of cash-out merger of corporation into new corporation. Alternate relief in form of damages was sought against members of board of directors, new corporation, and owners of parent of new corporation. Following trial, the Court of Chancery, granted judgment for directors by unreported letter opinion, and shareholders appealed. The Supreme Court held that: (1) board's decision to approve proposed cash-out merger was not product of informed business judgment; (2) board acted in grossly negligent manner in approving amendments to merger proposal; and (3) board failed to disclose all material facts which they knew or should have known before securing stockholders' approval of merger. On motions for reargument, the Court held that one director's absence from meetings of directors at which merger agreement and amendments to merger agreement were approved did not relieve that director from personal liability. Reversed and Remanded. McNeilly and Christie, JJ., filed dissenting opinions and dissented in part from denial of motions for reargument In carrying out their managerial roles, directors of corporation are charged with underlying fiduciary duty to corporation and its shareholders. Business judgment rule exists to protect and promote full and free exercise of managerial power granted to directors of corporations. Party attacking board of directors' decision as uninformed must rebut presumption that board's business judgment was informed one. Determination of whether business judgment of board of directors is informed one turns on whether directors have informed themselves, prior to making business decision, of all material information reasonably available to them. Board of directors acted in grossly negligent manner when it voted to amend merger agreement, where directors approved oral presentation of substance of proposed amendments, terms of which were not reduced to writing until two days later, rather than waiting to review amendments, again approved them sight unseen and adjourned, and even though amendments allowed corporation to solicit competing offers, corporation was permitted to terminate merger agreement and abandon merger only if, prior to shareholders' meeting, corporation had either consummated merger or sale of assets to third party or had entered into definitive merger 13

agreement more favorable than original and for greater consideration, and market test period for determining fairness of purchase price was effectively reduced by amendments. Board of directors lacked valuation information adequate to reach informed business judgment as to fairness of $55 per share for sale of company, notwithstanding magnitude of premium or spread between offering price and company's current market price of $38 per share, where market had consistently undervalued worth of stock, publicly traded stock price represents only value of single share and not value of whole company, board made no evaluation of company that was designed to value entire enterprise, board accepted without scrutiny chairman's representation as to fairness of $55 price per share for sale of company and thereby failed to discover that chairman had suggested $55 price and had arrived at that figure based on calculations designed solely to determine feasibility of leveraged buy-out. Business Judgment Rule (1) Under Delaware law, the business judgment rule is the offspring of the fundamental principle, codified in 8 Del.C. 141(a), that the business and affairs of a Delaware corporation are managed by or under its board of directors. The business judgment rule exists to protect and promote the full & free exercise of the managerial power granted to Del. directors

(e.g., causation): Transaction was entirely fair to corporation Fully-informed S/hs voted to approve boards action (Van Gorkom) 3. Process challenges may have lower threshold (e.g., ordinary negligence) for banks or financial intermediaries

Class Actions and Their Abuse Class actions were conceived as an expeditious way for people with similar grievances to join in a common suit and get compensated for injuries. But class actions have evolved into a favored means for trial lawyers to launch predatory assaults on businesses and large institutions, often in the name of clients who dont even know they are being represented. Despite the absurdity of many of these suits, legitimate companies are hard-pressed to defend themselves because they face thousands or even millions of plaintiffs. As they watch their share prices sink with bad publicity, companies almost always have to settle rather than risk billions of dollars in punitive damages. Increasingly, the end result is huge fees for the lawsuit industry an average of over $1,000 per hour according to Class Action Reports but relatively tiny awards for individual plaintiffs. For example, in one Texas case, lawyers sued two auto insurers for overbilling because the insurers rounded up premium bills to the next dollar (a practice that was sanctioned by the state insurance department) and pocketed almost $11 million; policyholders got a paltry $5.50 each, a typical result in class action lawsuits. MARKET IN SECURITIES Within days of a drop in a companys stock price (usually a high-growth technology stock with a naturally high shareprice volatility), trial lawyers swoop in to file a claimoften lacking any real proof of corporate wrongdoing. Corporations faced with the inevitable, extremely onerous discovery process must defend themselves at great expense; little wonder that such cases typically settle, with one-third of the proceeds going to lawyers. These actions merely redistribute wealth from one class of shareholders to another and thus do nothing to curb management abuse The empirical evidence shows that securities class actions settlement values are unrelated to the merits of the underlying cases, so the argument that the securities class action system offers any meaningful deterrent to corporate misconduct is wholly unpersuasive. Despite the Private Securities Litigation Reform Act of 1995, the securities gravy train for trial lawyers rolls on: securities class action filings rose 31 percent in 2002, and one prominent plaintiffs firm negotiated three recent 14

Business Judgment Rule (2) Since a director is vested with the responsibility for the management of the affairs of the corporation, he must execute that duty with the recognition that he acts on behalf of others. Such obligation does not tolerate faithlessness or self-dealing. But fulfillment of the fiduciary function requires more than the mere absence of bad faith or fraud. Representation of the financial interests of others imposes on a director an affirmative duty to protect those interests and to proceed with a critical eye. Business Judgment Rule (3) To be protected by the BJR, managerial decisions must meet the following criteria: made in good faith made with loyalty to the company made with due diligence

Challenging Process: Lessons from Van Gorkom 1. While BJR creates a presumption that the boards decision was informed plaintiff can rebut presumption by showing that prior to making decision, board was grossly negligent (or reckless) in informing themselves about material information reasonably available to them. 2. Defendants found to have breached their Duty of Care procedurally can still defend on other grounds

settlements of $300 million or more. Magnet Courts Unlike traditional lawsuits, class actions tend to involve plaintiffs from multiple jurisdictions, if not from all over the nation. Thus, instead of filing suit at the place of residence or injury as is normally required in the typical single plaintiff lawsuit trial lawyers are able to shop class action suits in search of the most favorable forum. Quite predictably, the best forum winds up being a state magnet court well known for its hospitable treatment of class action lawsuits. For instance, Madison County, Illinois recently made famous by handing out a $10.1 billion verdict against Philip Morris for allegedly insinuating that its light cigarettes were safer has seen a tremendous upsurge in class action filings in recent years. From 1998 to 2000, class action filings in Madison County increased over 1,800%; over 80% of these suits were brought on behalf of proposed nation-wide classes. Oversight of Class Action Settlements Many judges, too, see the need to rein in the lawsuit industrys worst excesses. In its landmark Campbell v. State Farm decision, the Supreme Court put a constitutional limit on a jurys ability to set punitive damages at an extreme multiple of actual damages. And while courts have traditionally been reluctant to enforce state codes of ethics prohibiting excessive fees, judges may finally be cracking down in the wake of the outrageous tobacco settlements: New York State judge Nicholas Figueroa recently threw out as excessive a $1.3 billion claim by the Castano group for work allegedly done on the California tobacco settlement. Magnet Courts Unlike traditional lawsuits, class actions tend to involve plaintiffs from multiple jurisdictions, if not from all over the nation. Thus, instead of filing suit at the place of residence or injury as is normally required in the typical single plaintiff lawsuit trial lawyers are able to shop class action suits in search of the most favorable forum. Quite predictably, the best forum winds up being a state magnet court well known for its hospitable treatment of class action lawsuits. For instance, Madison County, Illinois recently made famous by handing out a $10.1 billion verdict against Philip Morris for allegedly insinuating that its light cigarettes were safer has seen a tremendous upsurge in class action filings in recent years. From 1998 to 2000, class action filings in Madison County increased over 1,800%; over 80% of these suits were brought on behalf of proposed nation-wide classes. Oversight of Class Action Settlements Many judges, too, see the need to rein in the lawsuit industrys worst excesses. In its landmark Campbell

v. State Farm decision, the Supreme Court put a constitutional limit on a jurys ability to set punitive damages at an extreme multiple of actual damages. And while courts have traditionally been reluctant to enforce state codes of ethics prohibiting excessive fees, judges may finally be cracking down in the wake of the outrageous tobacco settlements: New York State judge Nicholas Figueroa in recent years threw out as excessive a $1.3 billion claim by the Castano group for work allegedly done on the California tobacco settlement. Duties of Agent to Principal Duty of Loyalty -- An agent: must act for the benefit of the principal. may not receive outside benefits without approval of the principal. can neither disclose nor use for her own benefit any confidential information. is not allowed to compete with his principal within the scope of the agency business. may not act for two principals whose interests conflict. may not become a party to a transaction without the principals permission. may not engage in inappropriate behavior that reflects badly on the principal Principals Remedies When the Agent Breaches a Duty The principal can recover damages caused by the agents breach. The agent must refund any profits made from the agency, if he breaches his duty of loyalty. The principal may rescind a transaction with an disloyal agent. Fiduciary Duties of Directors - Duty of Loyalty Questions about board members duty of loyalty most often arise where: There is a conflict of interest; or Board member takes advantage of a corporate opportunity of the Company. Traditional Duty of Loyalty Analysis Is there a conflict of interest? Direct Transaction between corporation and fiduciary Indirect Transaction between corp and another corp in which fiduciary has [substantial?] financial interest Family transactions If yes, transaction is voidable by corporation Compare: DGCL 144 Merely a financial interest for a conflict of interest Three Alternative ways to cleanse: Disclosure to Board of Directors & approval No quorum requirement; but majority of minority requirement 15

Disclosure to Shareholders & approval No apparent Quorum requirement Transaction fair at time of approval Burden of Proof? HOLDEN v. CONSTRUCTION MACHINERY COMPANY An action in equity was instituted, individually and derivatively, by the holder of 49.976% of the outstanding stock of a corporation, against the corporation, its officers and directors. The Black Hawk District Court held in part adverse to the defendants, and they appealed. The minority shareholder cross-appealed. The Supreme Court held that where the majority shareholder was found to be a constructive trustee of another company's stock, purchased with a check from the corporation, an award to the corporation of the shares including shares acquired by stock split and cash dividends appropriately stood as a judgment for restitution. The Court also held that where the majority shareholder, as president and general manager of the corporation, personally engineered every phase of the deal by which the stock in the other company was acquired by a check from the corporation, appropriated to his own use all dividends issued upon such stock, directed falsification of corporate records and other documents, and subsequently endeavored to impress upon the whole transaction a coloration of honesty and also did all in his power to isolate the minority holder from any rights or privileges pertaining to management, assessment of exemplary damages was compelled. Affirmed on defendants' appeal; reversed in part, affirmed in part, affirmed in part as modified on plaintiff's cross appeal, and remanded with instructions. Equity holds officers and directors of corporate entity, particularly management-controlling directors of closely held corporations, strictly accountable as trustees. Majority shareholder of corporation who was also president and general manager was strictly accountable to corporation for another company's stock purchased with check from corporation, or for fair market value of such stock, and for all increases, income, proceeds or dividends realized.

that some legally protected right has been invaded, such as by intentional act of fraud or other wrongful conduct. Security Requirement In around 1/3 of states (though not Delaware), a derivative claimant with low stakes must post security for corporations legal expenses. Why do you think this requirement exists? Effects on strategic or incentive problems among relevant parties (Shareholders, Managers, Attorneys)? Demand Requirement Most states require S/hs in derivative suits first to approach Board of Directors and demand that they pursue legal action unless the S/h can claim a valid excuse. When is demand requirement excused? If not excused, what recourse does S/h have if Board decides not to pursue? Does making the demand affect ones subsequent rights to bring a derivative action? EISENBERG v. The FLYING TIGER LINE, INC. Action by stockholder, on behalf of himself and all other stockholders of corporation similarly situated, to enjoin effectuation of plan of reorganization and merger. The United States District Court for the Eastern District of New York dismissed the action after stockholder failed to post security for corporation's costs and stockholder appealed. The Court of Appeals held that action seeking to overturn reorganization and merger the effects of which was that business operations were confined to a wholly owned subsidiary of holding company whose stockholders were the former stockholders of defendant corporation was a "personal action" and not "derivative" within meaning of New York statute requiring posting of security for corporation's costs. Reversed. Action by stockholder, suing on behalf of himself and all other stockholders of corporation similarly situated, seeking to overturn reorganization and merger the effect of which was that business operations were confined to a wholly owned subsidiary of holding company whose stockholders were the former stockholders of defendant corporation, was a "personal action" and not "derivative" within meaning of New York statute requiring posting of security for corporation's costs. If the gravamen of the complaint is injury to the corporation the suit is derivative, but "if the injury is one to the plaintiff as a stockholder and to him individually and not to the corporation," the suit is individual in nature and may take the form of a representative class action. 16

Where majority shareholder, as president and general manager of corporation, personally engineered every phase of deal by which stock in another company was acquired with check from corporation, appropriated to his own use all dividends issued upon such stock, directed falsification of corporate records and other documents, and subsequently endeavored to impress upon whole transaction a coloration of honesty and also did all in his power to isolate minority holder of 49.976% of outstanding stock from any rights or privileges pertaining to management, assessment of exemplary damages was compelled. In shareholder's derivative action, equity court may, in its discretion, award exemplary damages upon showing