También podría gustarte

- Report On Dutch Bangla BankDocumento22 páginasReport On Dutch Bangla BankIshita Israt100% (1)

- Brief Resume of Tofayel Hossain BasuniaDocumento5 páginasBrief Resume of Tofayel Hossain BasuniaMorshedDenarAlamMannaAún no hay calificaciones

- Sample Intl Bank StatementDocumento1 páginaSample Intl Bank Statementapi-3834921100% (1)

- TIN Application - NBR TIN RegistrationDocumento2 páginasTIN Application - NBR TIN RegistrationFerdous HasanAún no hay calificaciones

- NBR Tin Certificate 367005151131 PDFDocumento1 páginaNBR Tin Certificate 367005151131 PDFTahsan AhmedAún no hay calificaciones

- NBR Tin Certificate 468107475375Documento1 páginaNBR Tin Certificate 468107475375Wonder CatAún no hay calificaciones

- Saudi Arabia TINDocumento2 páginasSaudi Arabia TINseekusAún no hay calificaciones

- ISO 9001:2008 CERTIFIED Public Notice Verification of Taxpayers' RecordsDocumento2 páginasISO 9001:2008 CERTIFIED Public Notice Verification of Taxpayers' RecordsAnonymous FnM14a0Aún no hay calificaciones

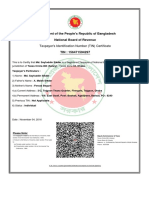

- Government of The People's Republic of Bangladesh National Board of RevenueDocumento1 páginaGovernment of The People's Republic of Bangladesh National Board of RevenuexgyhhbAún no hay calificaciones

- NBR Tin Certificate 897754123434Documento1 páginaNBR Tin Certificate 897754123434Md MasumAún no hay calificaciones

- NBR Tin Certificate 178747888345Documento1 páginaNBR Tin Certificate 178747888345Habibur RahmanAún no hay calificaciones

- NBR Tin Certificate 127597607663Documento1 páginaNBR Tin Certificate 127597607663MD. SaketAún no hay calificaciones

- Tax Code of BangladeshDocumento5 páginasTax Code of Bangladeshsouravsam100% (2)

- TIN SampleDocumento2 páginasTIN SampleAnonymous P78WJo8LPBAún no hay calificaciones

- NBR Tin Certificate 595255423005 PDFDocumento1 páginaNBR Tin Certificate 595255423005 PDFAlaul KarimAún no hay calificaciones

- NBR Tin Certificate 312329690222Documento1 páginaNBR Tin Certificate 312329690222ashaduzzamanAún no hay calificaciones

- E-TinDocumento1 páginaE-TinRezaul Alam100% (1)

- Bank Statement (Nisar Ahmad)Documento1 páginaBank Statement (Nisar Ahmad)hamid mahmoodAún no hay calificaciones

- NBR Tin Certificate 680851799008Documento1 páginaNBR Tin Certificate 680851799008Khaza MahbubAún no hay calificaciones

- NBR Tin Certificate 842774824093 PDFDocumento1 páginaNBR Tin Certificate 842774824093 PDFMd. Saifullah MunirAún no hay calificaciones

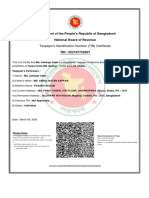

- Government of The People's Republic of Bangladesh National Board of RevenueDocumento1 páginaGovernment of The People's Republic of Bangladesh National Board of Revenuepddas13100% (1)

- NBR Tin Certificate 214981417638Documento1 páginaNBR Tin Certificate 214981417638MD. Saket0% (1)

- Petroleum Licence Application Form PDFDocumento10 páginasPetroleum Licence Application Form PDFnicholas idungafaAún no hay calificaciones

- TIN Certificate PDFDocumento1 páginaTIN Certificate PDFJust BangladeshAún no hay calificaciones

- NBR Tin Certificate 350467356871Documento1 páginaNBR Tin Certificate 350467356871Faisal Anwar100% (1)

- Applicant - S Information Sheet (ActiveOne) PDFDocumento4 páginasApplicant - S Information Sheet (ActiveOne) PDFmaris dinglasaAún no hay calificaciones

- NBR Tin Certificate 643541795237Documento2 páginasNBR Tin Certificate 643541795237nihaldu0% (1)

- Whmcs Freenom Module Installation Howto Version110Documento9 páginasWhmcs Freenom Module Installation Howto Version110Felix AdiAún no hay calificaciones

- Application Form For MSB Licence - Eng - 22032013Documento8 páginasApplication Form For MSB Licence - Eng - 22032013Shahrizan NoorAún no hay calificaciones

- TIN SayfDocumento1 páginaTIN SayfMd. Riazur RahmanAún no hay calificaciones

- NBR Tin Certificate 591973763133Documento1 páginaNBR Tin Certificate 591973763133TinyPavelAún no hay calificaciones

- FDA Certificate FileDocumento3 páginasFDA Certificate FileBilgi KurumsalAún no hay calificaciones

- BUSINESS LAW Assignment Bus 360-2-1 1Documento16 páginasBUSINESS LAW Assignment Bus 360-2-1 1Abrar SakibAún no hay calificaciones

- Study of Cash Management at Standard Chartered BankDocumento115 páginasStudy of Cash Management at Standard Chartered BankVishnu Prasad100% (2)

- YES BANK Savings AccountDocumento4 páginasYES BANK Savings AccountTanya MendirattaAún no hay calificaciones

- NBR Tin Certificate 622197722607Documento1 páginaNBR Tin Certificate 622197722607Xahangir AlamAún no hay calificaciones

- BUSLIC Business Licence FormDocumento10 páginasBUSLIC Business Licence Formcrew242Aún no hay calificaciones

- Process and Cost of Company Registration in BangladeshDocumento6 páginasProcess and Cost of Company Registration in BangladeshCompany Registration Consultancy ServiceAún no hay calificaciones

- Frequently Asked Questions & Answers For Pmoney:: 1. What Is Pmoney Internet Banking?Documento3 páginasFrequently Asked Questions & Answers For Pmoney:: 1. What Is Pmoney Internet Banking?ShahrearAún no hay calificaciones

- NBR Tin Certificate 266950216893 PDFDocumento1 páginaNBR Tin Certificate 266950216893 PDFFaruk HossainAún no hay calificaciones

- Government of The People'S Republic of Bangladesh: National Board of Revenue Mushak-9.1 Value Added Tax Return FormDocumento11 páginasGovernment of The People'S Republic of Bangladesh: National Board of Revenue Mushak-9.1 Value Added Tax Return FormMd. Abu NaserAún no hay calificaciones

- Added Registration: The of National ofDocumento1 páginaAdded Registration: The of National ofMd. S H MarufAún no hay calificaciones

- RDocumento2 páginasRMukesh ManwaniAún no hay calificaciones

- Fahimul Haque: Account Number Package Name Current Package Price Bill Period Due Date Bill Generation DateDocumento2 páginasFahimul Haque: Account Number Package Name Current Package Price Bill Period Due Date Bill Generation DateFahimul HoqueAún no hay calificaciones

- PTC 1Documento2 páginasPTC 1Shierly Arciaga ProtacioAún no hay calificaciones

- FBR - NTN Form PDFDocumento2 páginasFBR - NTN Form PDFAdeel Bin Khalid100% (1)

- Internship ReportDocumento52 páginasInternship ReportAvinash JainAún no hay calificaciones

- Bank Reconciliation Statement Worksheet With HintsDocumento1 páginaBank Reconciliation Statement Worksheet With Hintsapi-252642432Aún no hay calificaciones

- Name of The Company (In Full) :: Contractor / Vendor Registration FormDocumento14 páginasName of The Company (In Full) :: Contractor / Vendor Registration FormSantosh ThakurAún no hay calificaciones

- Loan Account Detail As On 15/07/2021: Issue Date: 15/07/2021 Page 1 of 12Documento12 páginasLoan Account Detail As On 15/07/2021: Issue Date: 15/07/2021 Page 1 of 12Omprakash KatreAún no hay calificaciones

- Summary DetailsDocumento1 páginaSummary DetailsAnk BasharAún no hay calificaciones

- Certificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)Documento52 páginasCertificate of Creditable Tax Withheld at Source: (MM/DD/YYYY) (MM/DD/YYYY)jeanieAún no hay calificaciones

- Ref - No. 16183558-19191991-3: Pramod Kumar S RDocumento3 páginasRef - No. 16183558-19191991-3: Pramod Kumar S RS R PramodAún no hay calificaciones

- NBR Tin Certificate 763444639565 PDFDocumento1 páginaNBR Tin Certificate 763444639565 PDFGame army shakilAún no hay calificaciones

- NBR Tin Certificate 180261996183 PDFDocumento1 páginaNBR Tin Certificate 180261996183 PDFNewaz KabirAún no hay calificaciones

- Company Profile IndusindDocumento2 páginasCompany Profile IndusindabhshekAún no hay calificaciones

- Tax Invoice: Invoice Number G0057870 Invoice DateDocumento1 páginaTax Invoice: Invoice Number G0057870 Invoice DateshamAún no hay calificaciones

- DBS Bank LTD Ground Floor Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-6638 8888 DBSS0IN0811 400641002Documento6 páginasDBS Bank LTD Ground Floor Express Towers, Nariman Point, Mumbai 400021 Maharashtra +91-22-6638 8888 DBSS0IN0811 400641002Sham AinapuAún no hay calificaciones

- Vendor Creation FormDocumento1 páginaVendor Creation FormRahul RSAún no hay calificaciones

- Dutch Bangla Bank Online BankingDocumento9 páginasDutch Bangla Bank Online BankingNazmulHasanAún no hay calificaciones

- Limbauan Vs AcostaDocumento6 páginasLimbauan Vs AcostaJENNY BUTACANAún no hay calificaciones

- Fan Kit InstructionDocumento4 páginasFan Kit InstructionCristian FernandezAún no hay calificaciones

- Press Release of New Michigan Children's Services Director Herman McCallDocumento2 páginasPress Release of New Michigan Children's Services Director Herman McCallBeverly TranAún no hay calificaciones

- Republic Vs MangotaraDocumento38 páginasRepublic Vs Mangotaramimisabayton0% (1)

- Liberalism and The American Natural Law TraditionDocumento73 páginasLiberalism and The American Natural Law TraditionPiguet Jean-GabrielAún no hay calificaciones

- Gen. Math. Periodical Exam. 2nd QuarterDocumento4 páginasGen. Math. Periodical Exam. 2nd Quarterhogmc media100% (1)

- Letter About Inadmissibility MP Majid Johari 2016-03-05Documento6 páginasLetter About Inadmissibility MP Majid Johari 2016-03-05api-312195002Aún no hay calificaciones

- Charles Steward Mott Foundation LetterDocumento2 páginasCharles Steward Mott Foundation LetterDave BondyAún no hay calificaciones

- Business law-Module+No.2Documento34 páginasBusiness law-Module+No.2Utkarsh SrivastavaAún no hay calificaciones

- IGAINYA LTD Vs NLC& AGDocumento15 páginasIGAINYA LTD Vs NLC& AGEdwin ChaungoAún no hay calificaciones

- Trade Union Act 1926Documento28 páginasTrade Union Act 1926Sanjeet Kumar33% (3)

- Invitations & Replies-1Documento14 páginasInvitations & Replies-1ADITYA PRATAPAún no hay calificaciones

- Slaoui The Rising Issue of Repeat ArbitratorsDocumento19 páginasSlaoui The Rising Issue of Repeat ArbitratorsJYhkAún no hay calificaciones

- Reading Wwii ApushDocumento12 páginasReading Wwii Apushapi-297350857Aún no hay calificaciones

- OMKAR OPTICALS (ZEISS) - 1346-12 Dec 23Documento1 páginaOMKAR OPTICALS (ZEISS) - 1346-12 Dec 23akansha16.kumariAún no hay calificaciones

- Division 1 NGODocumento183 páginasDivision 1 NGOAbu Bakkar SiddiqAún no hay calificaciones

- Pains of Imprisonment: University of Oslo, NorwayDocumento5 páginasPains of Imprisonment: University of Oslo, NorwayFady SamyAún no hay calificaciones

- PhptoDocumento13 páginasPhptoAshley Jovel De GuzmanAún no hay calificaciones

- Letter Request To Conduct Survey-JanuaryDocumento2 páginasLetter Request To Conduct Survey-JanuaryJohnNicoRamosLuceroAún no hay calificaciones

- FAR610 - Test 1-Apr2018-Q PDFDocumento3 páginasFAR610 - Test 1-Apr2018-Q PDFIman NadhirahAún no hay calificaciones

- Audit Program - CashDocumento1 páginaAudit Program - CashJoseph Pamaong100% (6)

- Barrazona V RTC City of Baguio - EjectmentDocumento9 páginasBarrazona V RTC City of Baguio - Ejectmentdoc dacuscosAún no hay calificaciones

- Ma2-2019 - Phan Gia BaoDocumento8 páginasMa2-2019 - Phan Gia BaoBao PAún no hay calificaciones

- NATO's Decision-Making ProcedureDocumento6 páginasNATO's Decision-Making Procedurevidovdan9852100% (1)

- NESCLDocumento56 páginasNESCLSamAún no hay calificaciones

- Incoterms 2012Documento60 páginasIncoterms 2012roberts79Aún no hay calificaciones

- Date Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceDocumento31 páginasDate Narration Chq./Ref - No. Value DT Withdrawal Amt. Deposit Amt. Closing BalanceSIDDHU KUMARAún no hay calificaciones

- Punong Himpilan Hukbong Dagat NG PilipinasDocumento9 páginasPunong Himpilan Hukbong Dagat NG PilipinasSheryl Sofia GanuayAún no hay calificaciones

- FERC Complaint Request Fast TrackDocumento116 páginasFERC Complaint Request Fast TrackThe PetroglyphAún no hay calificaciones

- Free ConsentDocumento2 páginasFree Consentkashif hamidAún no hay calificaciones