También podría gustarte

- EnerChemTek - The Reach of Energy and Its Value ChainDocumento15 páginasEnerChemTek - The Reach of Energy and Its Value ChainmdavilasAún no hay calificaciones

- EnerChemTek - The Reach of Energy and Its Value ChainDocumento15 páginasEnerChemTek - The Reach of Energy and Its Value ChainmdavilasAún no hay calificaciones

- MC Pub NaturalGasSupply 121814Documento31 páginasMC Pub NaturalGasSupply 121814Boris FernandezAún no hay calificaciones

- EnerChemTek - Adding Value To Canada's Polyolefins - Workshop - Sept. 2018Documento8 páginasEnerChemTek - Adding Value To Canada's Polyolefins - Workshop - Sept. 2018mdavilasAún no hay calificaciones

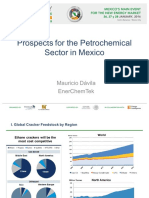

- Prospects For The Petrochemical Sector in MexicoDocumento8 páginasProspects For The Petrochemical Sector in MexicomdavilasAún no hay calificaciones

- Prospects For The Petrochemical Sector in MexicoDocumento8 páginasProspects For The Petrochemical Sector in MexicomdavilasAún no hay calificaciones

- Prospects For The Petrochemical Sector in MexicoDocumento8 páginasProspects For The Petrochemical Sector in MexicomdavilasAún no hay calificaciones

- Pemex Refineries & Base Oil Production 2017Documento2 páginasPemex Refineries & Base Oil Production 2017mdavilasAún no hay calificaciones

- The Global LNG Industry in TransitionDocumento10 páginasThe Global LNG Industry in TransitionmdavilasAún no hay calificaciones

- Monograde Vs Multigrade OilsDocumento3 páginasMonograde Vs Multigrade OilsmdavilasAún no hay calificaciones

- The Global LNG Industry in TransitionDocumento10 páginasThe Global LNG Industry in TransitionmdavilasAún no hay calificaciones

- The Global LNG Industry in TransitionDocumento10 páginasThe Global LNG Industry in TransitionmdavilasAún no hay calificaciones

- The Global LNG Industry in TransitionDocumento10 páginasThe Global LNG Industry in TransitionmdavilasAún no hay calificaciones

- Natural Gas - CFE StrategyDocumento19 páginasNatural Gas - CFE StrategymdavilasAún no hay calificaciones

- Costa Rica - Central America - Bio-Energy MarketsDocumento71 páginasCosta Rica - Central America - Bio-Energy MarketsmdavilasAún no hay calificaciones

- UOP-Mercury-Removal-From-Natural-Gas-and-Liquid-Streams-Tech-Paper 2 PDFDocumento9 páginasUOP-Mercury-Removal-From-Natural-Gas-and-Liquid-Streams-Tech-Paper 2 PDFPedraza Velandia JhonAún no hay calificaciones

- Economic Indicator (Cepci 2009)Documento2 páginasEconomic Indicator (Cepci 2009)hafiz_karim_2Aún no hay calificaciones

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2102)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- Behringer, Wolfgang (2006) - Communications Revolutions - A Historical ConceptDocumento42 páginasBehringer, Wolfgang (2006) - Communications Revolutions - A Historical Conceptlucaslsantana100% (1)

- List of Document PT Gunbuster Nickel Industry (GNI) GeneralDocumento2 páginasList of Document PT Gunbuster Nickel Industry (GNI) GeneralAlif GhazaliAún no hay calificaciones

- 7th Sea CCG - Reapers Fee SpoilersDocumento11 páginas7th Sea CCG - Reapers Fee SpoilersmrtibblesAún no hay calificaciones

- The Economic Impact of The World Cup On BrazilDocumento7 páginasThe Economic Impact of The World Cup On Brazileadona15Aún no hay calificaciones

- Kuantan PortDocumento11 páginasKuantan PortShashank Shekhar100% (1)

- Caravanning Australia v14#2Documento164 páginasCaravanning Australia v14#2Executive MediaAún no hay calificaciones

- Twin Clutch TransmissionDocumento237 páginasTwin Clutch TransmissionAkash Mankar100% (1)

- Sea King's MaliceDocumento144 páginasSea King's MaliceBrent Tanner100% (4)

- Lepa PDFDocumento97 páginasLepa PDFMiguel Angel MartinAún no hay calificaciones

- Manitou MLT 735 (EN)Documento20 páginasManitou MLT 735 (EN)ManitouAún no hay calificaciones

- Piper Warrior II N82487 Weight and Balance / CG: (2 GAL Unusable)Documento1 páginaPiper Warrior II N82487 Weight and Balance / CG: (2 GAL Unusable)C NascimentoAún no hay calificaciones

- FireEMS Location Analysis For Atlanta AirportDocumento46 páginasFireEMS Location Analysis For Atlanta AirportJulie WolfeAún no hay calificaciones

- 7.3 Vertical CurvesDocumento8 páginas7.3 Vertical CurvesJB RSNJNAún no hay calificaciones

- Match The WordsDocumento3 páginasMatch The WordsEmma ShavaAún no hay calificaciones

- HSC Business Studies Revision Guide PDFDocumento96 páginasHSC Business Studies Revision Guide PDFckAún no hay calificaciones

- Emirates AirlinesDocumento8 páginasEmirates AirlinesMuhammad AliAún no hay calificaciones

- SCM MCQSDocumento8 páginasSCM MCQSRao Nawaz Naji100% (3)

- Methodstatementhq Com GRP Pipe Installation and Lamination Method Statement HTML PDFDocumento22 páginasMethodstatementhq Com GRP Pipe Installation and Lamination Method Statement HTML PDFHaithem ChairiAún no hay calificaciones

- Copy FM 55-30: Motor Transportation OperationsDocumento76 páginasCopy FM 55-30: Motor Transportation OperationsjamesfletcherAún no hay calificaciones

- Rizal'S Visit To The United States (1888Documento2 páginasRizal'S Visit To The United States (1888banned napudAún no hay calificaciones

- MBTA Capital Needs Assessment and InventoryDocumento52 páginasMBTA Capital Needs Assessment and InventoryAbby PatkinAún no hay calificaciones

- Harga Satuan Upah Dan Bahan: Penanganan Drainase Semarang Wilayah TimurDocumento30 páginasHarga Satuan Upah Dan Bahan: Penanganan Drainase Semarang Wilayah TimurWahyu WidartoAún no hay calificaciones

- SAP Trg. Log Sheet - All ModulesDocumento51 páginasSAP Trg. Log Sheet - All Modulespawandubey9Aún no hay calificaciones

- SMRT Annual Report 2016Documento141 páginasSMRT Annual Report 2016Sassy TanAún no hay calificaciones

- Flying The Flag': Mapping IAL & Boac RoutesDocumento7 páginasFlying The Flag': Mapping IAL & Boac RoutesDave FaganAún no hay calificaciones

- West Tower vs. Phil. Ind. Corp.Documento14 páginasWest Tower vs. Phil. Ind. Corp.Antonio Dominic SalvadorAún no hay calificaciones

- Station Platforms: StandardDocumento35 páginasStation Platforms: StandardweihuangcraneAún no hay calificaciones

- 8frba SeriesDocumento2 páginas8frba Seriesargo kuncahyoAún no hay calificaciones

- Conway Maritime Press - Anatomy of The Ship - Hms VictoryDocumento121 páginasConway Maritime Press - Anatomy of The Ship - Hms VictoryWerner Welgens0% (1)

- ME 2010 04 Vehicle Front-End Active AerodynamicsDocumento6 páginasME 2010 04 Vehicle Front-End Active AerodynamicsAsha DashAún no hay calificaciones