También podría gustarte

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Forex Chart Patterns in DepthDocumento70 páginasForex Chart Patterns in DepthNicolausBernard97% (32)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- Sample PDFDocumento2 páginasSample PDFkorean languageAún no hay calificaciones

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- w2022-Manu-Puti Adani-02032022Documento8 páginasw2022-Manu-Puti Adani-02032022Ulfa ChairaniAún no hay calificaciones

- APTB - A-SME PLATINUM-i - Application Form (SST) PDFDocumento16 páginasAPTB - A-SME PLATINUM-i - Application Form (SST) PDFMuizz LynnAún no hay calificaciones

- Projected Cash Income For The Year 2021-2025 RevenuesDocumento9 páginasProjected Cash Income For The Year 2021-2025 RevenuesAllia AntalanAún no hay calificaciones

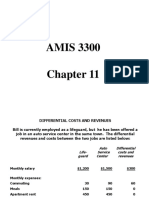

- Ch11PPSpring2016 1q5mpc0Documento20 páginasCh11PPSpring2016 1q5mpc0RiskaAún no hay calificaciones

- Chapter I and Chapter IiDocumento32 páginasChapter I and Chapter IiDhanya vijeeshAún no hay calificaciones

- Mathematics & Decision MakingDocumento9 páginasMathematics & Decision MakingXahed AbdullahAún no hay calificaciones

- Capital StructureDocumento4 páginasCapital StructureNaveen GurnaniAún no hay calificaciones

- KPK Tehsil Municipal Officer (TMO) Syllabus 2017-2018Documento1 páginaKPK Tehsil Municipal Officer (TMO) Syllabus 2017-2018Hidayat UllahAún no hay calificaciones

- The West Bengal Land Reforms Act, 1955 PDFDocumento121 páginasThe West Bengal Land Reforms Act, 1955 PDFaditya dasAún no hay calificaciones

- Financial Accounting and Reporting Test Bank 80102016 - 3: Problem 1 - Investment in AssociateDocumento5 páginasFinancial Accounting and Reporting Test Bank 80102016 - 3: Problem 1 - Investment in AssociateCarlo ParasAún no hay calificaciones

- BSG Decisions & Reports3Documento9 páginasBSG Decisions & Reports3Deyvis GabrielAún no hay calificaciones

- Westside BillDocumento3 páginasWestside BillVamsee309Aún no hay calificaciones

- Thapa. Bina Thapa. Prakash PDFDocumento76 páginasThapa. Bina Thapa. Prakash PDFTILAHUNAún no hay calificaciones

- Bir Form 1601-CDocumento4 páginasBir Form 1601-Csanto tomas proper barangay100% (1)

- AssignmentDocumento8 páginasAssignmentEdna MingAún no hay calificaciones

- Review of Literature: Chapter-2Documento5 páginasReview of Literature: Chapter-2Juan JacksonAún no hay calificaciones

- Exercise On Hedging (KEY)Documento2 páginasExercise On Hedging (KEY)juringAún no hay calificaciones

- Chapter 1 & CFP Code or EthicsDocumento9 páginasChapter 1 & CFP Code or EthicsEleni StratigakosAún no hay calificaciones

- Triangle Chart Patterns Are Commonly Used Continuation Chart Patterns and Are Easy To Trade As ItDocumento7 páginasTriangle Chart Patterns Are Commonly Used Continuation Chart Patterns and Are Easy To Trade As ItMark PangantihonAún no hay calificaciones

- Dasar Penilaian Bumi Dan Bangunan Dibawah Harga Pasar (Studi Di Dipenda Kabupaten Mojokerto)Documento25 páginasDasar Penilaian Bumi Dan Bangunan Dibawah Harga Pasar (Studi Di Dipenda Kabupaten Mojokerto)Deni Dwi PutraAún no hay calificaciones

- Pas 20 - Acctg For Govt Grants & Disclosure of Govt AssistanceDocumento12 páginasPas 20 - Acctg For Govt Grants & Disclosure of Govt AssistanceGraciasAún no hay calificaciones

- CIR Vs Filinvest Development Corporation - Tax CaseDocumento17 páginasCIR Vs Filinvest Development Corporation - Tax CaseKyle AlmeroAún no hay calificaciones

- Luigi Balucan Inacc3 Week 2Documento12 páginasLuigi Balucan Inacc3 Week 2Luigi Enderez BalucanAún no hay calificaciones

- PAYE2012 DemoDocumento110 páginasPAYE2012 DemoNorvee ReyesAún no hay calificaciones

- Contoh Format QuotationDocumento1 páginaContoh Format QuotationBenjaminOmar100% (1)

- Halina Mountain Resort (B)Documento5 páginasHalina Mountain Resort (B)SuzetTe OlmedoAún no hay calificaciones

- Audit Exam 1 ReviewDocumento6 páginasAudit Exam 1 ReviewPhish182Aún no hay calificaciones

- TX 105 Estate TaxDocumento2 páginasTX 105 Estate TaxRose Kristy SindayenAún no hay calificaciones