También podría gustarte

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5795)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- CORPO Control and Managment 1Documento92 páginasCORPO Control and Managment 1alyza burdeosAún no hay calificaciones

- A Summer Internship Report On: Master of Business AdministrationDocumento47 páginasA Summer Internship Report On: Master of Business AdministrationLove GumberAún no hay calificaciones

- Real Estate Construction COO in San Francisco Bay CA Resume Mark HeaveyDocumento2 páginasReal Estate Construction COO in San Francisco Bay CA Resume Mark HeaveyMarkHeaveyAún no hay calificaciones

- How To Create Make Print Payroll Pay Check Payslip Stub w-2 w/2 w2 1099 Forms Self Employed CreditDocumento7 páginasHow To Create Make Print Payroll Pay Check Payslip Stub w-2 w/2 w2 1099 Forms Self Employed Creditrealstubs50% (4)

- Monte de Piedad Vs RodrigoDocumento4 páginasMonte de Piedad Vs RodrigoEricson Sarmiento Dela CruzAún no hay calificaciones

- NYC EDC Atlantic Yards Cost-Benefit Analysis 2009Documento3 páginasNYC EDC Atlantic Yards Cost-Benefit Analysis 2009Norman OderAún no hay calificaciones

- Internship Report CBDocumento27 páginasInternship Report CBAyoniseh Carol100% (1)

- "Fundamental Analysis of Voltas": P.E.S Institute of Technology Department of MBADocumento17 páginas"Fundamental Analysis of Voltas": P.E.S Institute of Technology Department of MBAJennifer SmithAún no hay calificaciones

- Appeasement ArgumentsDocumento3 páginasAppeasement Argumentsapi-309710992Aún no hay calificaciones

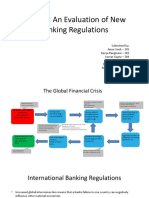

- Basel III: An Evaluation of New Banking RegulationsDocumento22 páginasBasel III: An Evaluation of New Banking RegulationsMegha BepariAún no hay calificaciones

- Recording Procedures-Barangay FundsDocumento21 páginasRecording Procedures-Barangay FundsMarliezel Sarda100% (1)

- Market Transformation Through Introduction of Energy-Efficient Electric Vehicles ProjectDocumento20 páginasMarket Transformation Through Introduction of Energy-Efficient Electric Vehicles ProjectElvin LouieAún no hay calificaciones

- BEL Executive Wage Revision 2009Documento21 páginasBEL Executive Wage Revision 2009banker_mcaAún no hay calificaciones

- Accounting BasicsDocumento144 páginasAccounting BasicsSabyasachi Srimany100% (1)

- Take Home Quiz Audit Theory-CPA BoardDocumento7 páginasTake Home Quiz Audit Theory-CPA BoardJc GappiAún no hay calificaciones

- ACCA F7 MockDocumento17 páginasACCA F7 MockayeshaghufranAún no hay calificaciones

- COREN Assembly by Engr. Chris Okoye (V. 03)Documento41 páginasCOREN Assembly by Engr. Chris Okoye (V. 03)bbllngAún no hay calificaciones

- Case Digest: Lozana vs. DepakakiboDocumento32 páginasCase Digest: Lozana vs. DepakakiboDjan QuidatoAún no hay calificaciones

- Functions of Central Bank Final PresentationDocumento27 páginasFunctions of Central Bank Final PresentationZayed Mohammad JohnyAún no hay calificaciones

- OFS9.Special OFS Messages (FOREX and LD) - R13 PDFDocumento18 páginasOFS9.Special OFS Messages (FOREX and LD) - R13 PDFPreethi GopalanAún no hay calificaciones

- NHB Grievance Redressal PolicyDocumento13 páginasNHB Grievance Redressal PolicyGitanjali SinghAún no hay calificaciones

- Assessment ProcessDocumento2 páginasAssessment ProcessAltheaVergaraAún no hay calificaciones

- Direct Tax Summary Notes For IPCC JKQK1AK0Documento24 páginasDirect Tax Summary Notes For IPCC JKQK1AK0Vivek ShimogaAún no hay calificaciones

- Position PaperDocumento9 páginasPosition PaperRoel PalmairaAún no hay calificaciones

- Balance of PaymentsDocumento14 páginasBalance of Paymentsনীল রহমানAún no hay calificaciones

- FranchiseeDocumento43 páginasFranchiseeMAHENDERAún no hay calificaciones

- WBW Deed - Compare Version (3).pdf WBWC Settlement Deed Allan Family Wide Bay Water Lenthalls Dam Gate Failures Peter Care CEO Fraser Coast Regional Council Hervey Bay Burrum River Torbanlea Howard Crest Gate Failure Dam Failure Tops Gates FailureDocumento23 páginasWBW Deed - Compare Version (3).pdf WBWC Settlement Deed Allan Family Wide Bay Water Lenthalls Dam Gate Failures Peter Care CEO Fraser Coast Regional Council Hervey Bay Burrum River Torbanlea Howard Crest Gate Failure Dam Failure Tops Gates FailureLenthallsdamgatefailAún no hay calificaciones

- American Diplomatic Noncitizen National Passport and MCO52418Documento4 páginasAmerican Diplomatic Noncitizen National Passport and MCO52418NotarysTo Go100% (52)

- Credit Risk Project PDFDocumento104 páginasCredit Risk Project PDFDenish PatelAún no hay calificaciones

- Private Equity and Private Debt Investments in IndiaDocumento76 páginasPrivate Equity and Private Debt Investments in Indiagoyal.rohit8089Aún no hay calificaciones