También podría gustarte

- Accounts Payable NotesDocumento12 páginasAccounts Payable Notesjohn_841100% (1)

- Subcontracting Process in SAPDocumento11 páginasSubcontracting Process in SAPUmakant MahapatraAún no hay calificaciones

- Assets Capitalization Routing Through CWIP or AuC With IODocumento3 páginasAssets Capitalization Routing Through CWIP or AuC With IORavindra Jain100% (2)

- Intercompany Billing ProcessDocumento4 páginasIntercompany Billing ProcessKhushi Mughal100% (1)

- Accounting EnteriesDocumento9 páginasAccounting Enterieskavita sihagAún no hay calificaciones

- GR&IR Clearing AccountDocumento8 páginasGR&IR Clearing AccountWupankAún no hay calificaciones

- GR IR Account Maintenance in SAPDocumento6 páginasGR IR Account Maintenance in SAPVishnu Kumar S100% (1)

- Misc Reporting ConfigDocumento4 páginasMisc Reporting ConfigTitus GeorgeAún no hay calificaciones

- Display A List of POs With Outstanding GR or IRDocumento6 páginasDisplay A List of POs With Outstanding GR or IRchonchalAún no hay calificaciones

- ABC Construction Revenue RecognitionDocumento15 páginasABC Construction Revenue RecognitionJam SurdivillaAún no hay calificaciones

- Fashion Event Management SyllabusDocumento2 páginasFashion Event Management SyllabusRitika KabraAún no hay calificaciones

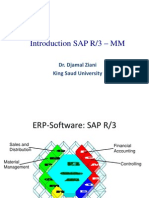

- Introduction SAP R/3 - MM: Dr. Djamal Ziani King Saud UniversityDocumento67 páginasIntroduction SAP R/3 - MM: Dr. Djamal Ziani King Saud UniversitySachin RachanaikarAún no hay calificaciones

- 1.-Accounting For ConsignmentsDocumento40 páginas1.-Accounting For ConsignmentsEligius Nyika50% (6)

- Third Party GRDocumento2 páginasThird Party GRayan dasAún no hay calificaciones

- SAP GST - Smajo Rapid Start RoadMap V1.0Documento25 páginasSAP GST - Smajo Rapid Start RoadMap V1.0satwikaAún no hay calificaciones

- Chapter 3 Accounting Books and RecordsDocumento77 páginasChapter 3 Accounting Books and RecordsRashid Hussain80% (5)

- Understanding the Key Data and Process Flow in SAP MM ModuleDocumento40 páginasUnderstanding the Key Data and Process Flow in SAP MM ModuleexcelhelplineAún no hay calificaciones

- Consignment Accounts: Consignment-What Is It?Documento6 páginasConsignment Accounts: Consignment-What Is It?neeraj goyal100% (1)

- 5 Steps to Understand Product Costing in SAP FICODocumento7 páginas5 Steps to Understand Product Costing in SAP FICOsreekumarAún no hay calificaciones

- Accounting For Consigned GoodsDocumento6 páginasAccounting For Consigned GoodsHumphrey OdchigueAún no hay calificaciones

- Validation Process of VAT Numbers in SAP - Tax Management ConsultancyDocumento3 páginasValidation Process of VAT Numbers in SAP - Tax Management Consultancyfairdeal2k1Aún no hay calificaciones

- Purchase Vs Consumption Based Accounting Accounting Entries in SapDocumento10 páginasPurchase Vs Consumption Based Accounting Accounting Entries in SapAAPS ACGSAún no hay calificaciones

- TP Technolgoies: Cross Company Code Configuration and TestingDocumento11 páginasTP Technolgoies: Cross Company Code Configuration and TestingKrushna SwainAún no hay calificaciones

- At-5909 Risk AssessmentDocumento7 páginasAt-5909 Risk Assessmentshambiruar100% (2)

- CO-PA Profitability Analysis and Planning FundamentalsDocumento47 páginasCO-PA Profitability Analysis and Planning Fundamentalsitkishorkumar33% (3)

- What Is Debit or Credit MemosDocumento2 páginasWhat Is Debit or Credit Memoschauhans_100Aún no hay calificaciones

- Consignment Accounting Journal EntriesDocumento22 páginasConsignment Accounting Journal EntriesRashid HussainAún no hay calificaciones

- Credit ManagementDocumento14 páginasCredit ManagementPurushottam Kashte100% (1)

- Configure Asset Under ConstructionDocumento18 páginasConfigure Asset Under ConstructionSandhya AbhishekAún no hay calificaciones

- How To Configure Inter Company BillingDocumento4 páginasHow To Configure Inter Company BillingSwarna Kumar GAún no hay calificaciones

- GST Return Business Process For GSTDocumento72 páginasGST Return Business Process For GSTAccounting & Taxation100% (1)

- Third Party ProcessingDocumento3 páginasThird Party ProcessingVishnu Kumar SAún no hay calificaciones

- STP Analysis of NikeDocumento8 páginasSTP Analysis of NikeManshi SadadeAún no hay calificaciones

- Duplicate Invoice Check Part 1Documento10 páginasDuplicate Invoice Check Part 1Rajeev MenonAún no hay calificaciones

- Factsheet 1 - Planning A Kuroilers Business VentureDocumento3 páginasFactsheet 1 - Planning A Kuroilers Business VentureYouth Environmental and Social Enterprises (YESE)60% (5)

- Cross-Company - Inter-Company Transactions - SAP BlogsDocumento12 páginasCross-Company - Inter-Company Transactions - SAP BlogsAnanthakumar A100% (1)

- Sap Fi Retained Earnings AccountsDocumento1 páginaSap Fi Retained Earnings AccountsDebabrata SahooAún no hay calificaciones

- SAP Intercompany Sales Configuration GuideDocumento10 páginasSAP Intercompany Sales Configuration GuideDILIP PORWALAún no hay calificaciones

- SAP MM Consignment StockDocumento2 páginasSAP MM Consignment StockPadmanabha Narayan0% (1)

- Inter Company SalesDocumento6 páginasInter Company SalesParvati B100% (1)

- Unit 2: Sale of Goods On Approval or Return Basis: Learning OutcomesDocumento17 páginasUnit 2: Sale of Goods On Approval or Return Basis: Learning OutcomessajedulAún no hay calificaciones

- Exercise 4. 2 - Financial Accotg - SAP FrioriDocumento18 páginasExercise 4. 2 - Financial Accotg - SAP FriorileoAún no hay calificaciones

- Welcome To Level 2 Training: by LGS TeamDocumento31 páginasWelcome To Level 2 Training: by LGS Teamkrishna_1238Aún no hay calificaciones

- Stock Transfer From A Plant To Another Plant in SAPDocumento4 páginasStock Transfer From A Plant To Another Plant in SAPCristiano LimaAún no hay calificaciones

- INTRASTAT Declarations - Italy - SAP LibraryDocumento1 páginaINTRASTAT Declarations - Italy - SAP LibraryAlphaSierra5056Aún no hay calificaciones

- Final AccountsDocumento61 páginasFinal AccountsvimalaAún no hay calificaciones

- 13 PO & GR IV With ValuationsDocumento31 páginas13 PO & GR IV With ValuationslymacsauokAún no hay calificaciones

- Procure To Pay ProcessDocumento54 páginasProcure To Pay ProcessSunil KumarAún no hay calificaciones

- Inter Company Stock Transfer Process 1682874118Documento14 páginasInter Company Stock Transfer Process 1682874118Dalil HbyAún no hay calificaciones

- Multiple Account Assignment Non Valuated GR Reqs&POsDocumento7 páginasMultiple Account Assignment Non Valuated GR Reqs&POsLohith KumarAún no hay calificaciones

- Inter Company SalesDocumento3 páginasInter Company SaleshrsapvisionAún no hay calificaciones

- Direct Return To VendorDocumento5 páginasDirect Return To VendorsandunsulakshanaAún no hay calificaciones

- IND AS-16 Property, Plant and Equipment: Measurement of PpeDocumento3 páginasIND AS-16 Property, Plant and Equipment: Measurement of PpeHimank SinglaAún no hay calificaciones

- Tax Vat CasesDocumento51 páginasTax Vat CasesCassey Koi FarmAún no hay calificaciones

- Inter Company BillingDocumento5 páginasInter Company BillingMaheshJMAún no hay calificaciones

- Stock Transfer Between Plants in One StepDocumento5 páginasStock Transfer Between Plants in One StepRahul JainAún no hay calificaciones

- Invoice ListDocumento19 páginasInvoice ListRinna Belle Cruz-Soliva100% (1)

- Global Movement Types and Accounting DocumentsDocumento13 páginasGlobal Movement Types and Accounting DocumentsJoy Kristine BuenaventuraAún no hay calificaciones

- Cash Journal - Asset Payment and CapitalizationDocumento11 páginasCash Journal - Asset Payment and CapitalizationpaiashokAún no hay calificaciones

- ThirdPartySales SAP SDDocumento14 páginasThirdPartySales SAP SDRaja ShekarAún no hay calificaciones

- SAP Field Status Definition GroupsDocumento3 páginasSAP Field Status Definition GroupsMrudula V.100% (1)

- ERPLO DeemedExport 200614 0653 1304Documento4 páginasERPLO DeemedExport 200614 0653 1304SivaprasadVasireddyAún no hay calificaciones

- Consignment Accounting Journal EntriesDocumento2 páginasConsignment Accounting Journal EntriesVenn Bacus RabadonAún no hay calificaciones

- Consignments and Bill of ExchangeDocumento4 páginasConsignments and Bill of ExchangeNurfarhanis Bt Azamuddin Anis100% (2)

- ConsignmentDocumento2 páginasConsignmentLorifel Antonette Laoreno TejeroAún no hay calificaciones

- Chandoo 07mar17Documento2 páginasChandoo 07mar17Nanda CmaAún no hay calificaciones

- Research proposal on fast food brand perception in VietnamDocumento5 páginasResearch proposal on fast food brand perception in VietnamHuỳnh ChâuAún no hay calificaciones

- 02 Break Even AnalysisDocumento9 páginas02 Break Even AnalysisMarenightAún no hay calificaciones

- Accounts Cia Accounting Concepts, Conventions and ApplicationsDocumento11 páginasAccounts Cia Accounting Concepts, Conventions and ApplicationsAashish mishraAún no hay calificaciones

- Control Cost CentersDocumento31 páginasControl Cost CentersMendoza KlariseAún no hay calificaciones

- A Study On Distribution Channels in CementindustryDocumento8 páginasA Study On Distribution Channels in CementindustryAashish MishraAún no hay calificaciones

- Introduction To Economics - ppt1Documento13 páginasIntroduction To Economics - ppt1Akshay HemanthAún no hay calificaciones

- University of California PE and VC IRR ReturnsDocumento5 páginasUniversity of California PE and VC IRR Returnsdavidsun1988Aún no hay calificaciones

- Principles of Accounting Chapter 12Documento40 páginasPrinciples of Accounting Chapter 12myrentistoodamnhigh100% (2)

- 4303 14719 1 PBDocumento19 páginas4303 14719 1 PBshintyaAún no hay calificaciones

- 5.IAS 23 .Borrowing Cost Q&ADocumento12 páginas5.IAS 23 .Borrowing Cost Q&AAbdulkarim Hamisi KufakunogaAún no hay calificaciones

- Operations 12122017 12032018Documento2 páginasOperations 12122017 12032018Mohamed ElankoudAún no hay calificaciones

- Demat AccountDocumento5 páginasDemat AccountHimanshu Das100% (1)

- 3 AccountingDocumento39 páginas3 AccountingSaltanat ShamovaAún no hay calificaciones

- Practice 2Documento24 páginasPractice 2Софи БреславецAún no hay calificaciones

- Palmer Cook Productions Manages and Operates Two Rock Bands TheDocumento1 páginaPalmer Cook Productions Manages and Operates Two Rock Bands TheLet's Talk With HassanAún no hay calificaciones

- LITERATURE REVIEW ON ASSET-LIABILITY MANAGEMENTDocumento9 páginasLITERATURE REVIEW ON ASSET-LIABILITY MANAGEMENTAnkur Upadhyay0% (1)

- Advanced Financial Reporting and Theory 26325 Module Leader: Pat MouldDocumento8 páginasAdvanced Financial Reporting and Theory 26325 Module Leader: Pat MouldKaran ChopraAún no hay calificaciones

- Test BankDocumento16 páginasTest BankHashaira AlimAún no hay calificaciones

- Financial Accounting (D.com-II)Documento6 páginasFinancial Accounting (D.com-II)Basit RehmanAún no hay calificaciones

- Practice Final Bus331 Spring2023Documento2 páginasPractice Final Bus331 Spring2023Javan OdephAún no hay calificaciones

- Audit of ExpensesDocumento18 páginasAudit of Expenseseequals mcsquaredAún no hay calificaciones

- Personal Selling - Within 1000 WordsDocumento23 páginasPersonal Selling - Within 1000 Wordssangeta100% (1)

- Pcoa 008 - Intermediate Accounting Ii Learning OutcomesDocumento19 páginasPcoa 008 - Intermediate Accounting Ii Learning OutcomesNicole LucasAún no hay calificaciones

- Topic 4 PP&EDocumento62 páginasTopic 4 PP&Efastidious_5100% (1)