También podría gustarte

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5795)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

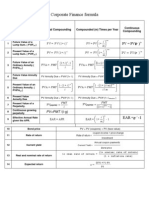

- Corporate Finance FormulasDocumento3 páginasCorporate Finance FormulasMustafa Yavuzcan83% (12)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- Eastboro Case SolutionDocumento22 páginasEastboro Case Solutionuddindjm100% (2)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- FINC 312 Midterm Exam 1-Fall 2020Documento8 páginasFINC 312 Midterm Exam 1-Fall 2020Gianna DeMarcoAún no hay calificaciones

- Coca-Cola Corporate ValuationDocumento29 páginasCoca-Cola Corporate ValuationS Scott Taylor100% (2)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- Aes Case SolutionDocumento3 páginasAes Case SolutionXimenaLopezCifuentes100% (1)

- Company-Specific Risk Premiums (American Bankruptcy Insitute, 2010) PDFDocumento100 páginasCompany-Specific Risk Premiums (American Bankruptcy Insitute, 2010) PDFMichael SmithAún no hay calificaciones

- MIRANDA - Post Task 3,4,5 Compilation PDFDocumento9 páginasMIRANDA - Post Task 3,4,5 Compilation PDFSHARMAINE CORPUZ MIRANDAAún no hay calificaciones

- Value CreationDocumento48 páginasValue Creationviral1622100% (1)

- Financial Accounting Theory Craig Deegan Chapter 7Documento41 páginasFinancial Accounting Theory Craig Deegan Chapter 7Rob26in0978% (9)

- Top 52 Financial Analyst Interview Questions and AnswersDocumento24 páginasTop 52 Financial Analyst Interview Questions and AnswersJerry TurtleAún no hay calificaciones

- Distress PDFDocumento65 páginasDistress PDFKhushal UpraityAún no hay calificaciones

- Final Doc of Management AssignmentDocumento10 páginasFinal Doc of Management AssignmentrasithapradeepAún no hay calificaciones

- Security Analysis and Valuation Blue Red Ink (1) - WatermarkDocumento22 páginasSecurity Analysis and Valuation Blue Red Ink (1) - WatermarkKishan RajyaguruAún no hay calificaciones

- Securities Fraud, Stock Price Valuation, and Loss Causation: Toward A Corporate Finance-Based Theory of Loss CausationDocumento5 páginasSecurities Fraud, Stock Price Valuation, and Loss Causation: Toward A Corporate Finance-Based Theory of Loss CausationMoin Max ReevesAún no hay calificaciones

- FMDocumento45 páginasFMSaumya GoelAún no hay calificaciones

- Cost FM Sample PaperDocumento6 páginasCost FM Sample PapercacmacsAún no hay calificaciones

- Colgate ReportDocumento17 páginasColgate Reportpinakchatterjee669Aún no hay calificaciones

- 15 Dividend DecisionDocumento18 páginas15 Dividend Decisionsiva19789Aún no hay calificaciones

- D - 05 Berger PaintsDocumento7 páginasD - 05 Berger PaintstanyaAún no hay calificaciones

- Homework 7 Problems and SolutionsDocumento17 páginasHomework 7 Problems and Solutionswasif ahmedAún no hay calificaciones

- Valuation of SharesDocumento23 páginasValuation of SharesRuchi SharmaAún no hay calificaciones

- Method of Banks Valuation: Horvátová Eva UDC: 336.717 JEL: G21Documento11 páginasMethod of Banks Valuation: Horvátová Eva UDC: 336.717 JEL: G21VARUN SINGLAAún no hay calificaciones

- Leverages NotesDocumento9 páginasLeverages NotesAshwani ChouhanAún no hay calificaciones

- Kuis Manajemen Keuangan - Manajemen UIDocumento16 páginasKuis Manajemen Keuangan - Manajemen UIjadwal SekjenAún no hay calificaciones

- Rapidrill Case AnalysisDocumento8 páginasRapidrill Case AnalysisAdeel RanaAún no hay calificaciones

- Tài liệu TA CF chap 15 16 23 24Documento18 páginasTài liệu TA CF chap 15 16 23 24huanbilly2003Aún no hay calificaciones

- Bahas Latihan Soal WACCDocumento5 páginasBahas Latihan Soal WACCagnesAún no hay calificaciones

- Financial Study of ACCDocumento65 páginasFinancial Study of ACCAmitabh TiwariAún no hay calificaciones

- TYBMS Sem 5 SyllabusDocumento15 páginasTYBMS Sem 5 SyllabusRavi KrishnanAún no hay calificaciones

- Af208 Fe PDFDocumento14 páginasAf208 Fe PDFTetzAún no hay calificaciones