También podría gustarte

- ACC10 L1 01 Fundamentals of Accounting CgomezDocumento6 páginasACC10 L1 01 Fundamentals of Accounting CgomezccgomezAún no hay calificaciones

- Forms of Business OrganisationDocumento19 páginasForms of Business OrganisationCaroline Rebecca DAún no hay calificaciones

- As Entrepreneurship Q4 Week 1 2Documento13 páginasAs Entrepreneurship Q4 Week 1 2Mawie duligAún no hay calificaciones

- Notes Ni HazelDocumento38 páginasNotes Ni HazelJulia GorgonioAún no hay calificaciones

- Module in Fundamentals of ABM 1Documento81 páginasModule in Fundamentals of ABM 1A.Aún no hay calificaciones

- ABM Fundamentals of ABM 1 CG PDFDocumento7 páginasABM Fundamentals of ABM 1 CG PDFMica SaeronAún no hay calificaciones

- Abm1 PPTDocumento161 páginasAbm1 PPTPavi Antoni Villaceran100% (1)

- Chapter 5 - Type of Business According To ActivitiesDocumento10 páginasChapter 5 - Type of Business According To Activitiesairam cabadduAún no hay calificaciones

- BookkeepingDocumento11 páginasBookkeepingGlenn Asuncion PagaduanAún no hay calificaciones

- The Accounting Equation: An IntroductionDocumento8 páginasThe Accounting Equation: An IntroductionALMA ACUNAAún no hay calificaciones

- SYLLABUS Financial Accounting and ReportingDocumento9 páginasSYLLABUS Financial Accounting and ReportingChristian De GuzmanAún no hay calificaciones

- Fundamentals of Accountancy Business and Management II Module 2Documento5 páginasFundamentals of Accountancy Business and Management II Module 2Rafael RetubisAún no hay calificaciones

- Lesson 8 Elements of FsDocumento53 páginasLesson 8 Elements of FsSoothing BlendAún no hay calificaciones

- Definitions of Common Accounting TermsDocumento6 páginasDefinitions of Common Accounting TermsAliya SaeedAún no hay calificaciones

- Quiz 4 Types of Major Accounts Without AnswerDocumento5 páginasQuiz 4 Types of Major Accounts Without AnswerHello KittyAún no hay calificaciones

- Fundamentals of Abm 1 Quarter 2, Week 1Documento2 páginasFundamentals of Abm 1 Quarter 2, Week 1Shiellai Mae PolintangAún no hay calificaciones

- FABM1 Week1Documento5 páginasFABM1 Week1TrixieAún no hay calificaciones

- Lesson 2 ACCOUNTING AS THE LANGUAGE OF BUSINESSDocumento9 páginasLesson 2 ACCOUNTING AS THE LANGUAGE OF BUSINESSamora elyseAún no hay calificaciones

- FMA PPT-3 Accounting Cycle & Journal EntriesDocumento17 páginasFMA PPT-3 Accounting Cycle & Journal EntriesArpit VermaAún no hay calificaciones

- Modules 1Documento4 páginasModules 1JT GalAún no hay calificaciones

- Syllabus Mgmt. AcctgDocumento10 páginasSyllabus Mgmt. AcctgVanessa L. VinluanAún no hay calificaciones

- On Line Class With 11 ABM Day1Documento21 páginasOn Line Class With 11 ABM Day1Mirian De Ocampo100% (1)

- Chapter 2 Branches of Accounting and Users of Accounting InformationDocumento14 páginasChapter 2 Branches of Accounting and Users of Accounting InformationAngellouiza MatampacAún no hay calificaciones

- Merchandising BusinessDocumento31 páginasMerchandising BusinessAngelo ReyesAún no hay calificaciones

- Chapter 2 Acctg 1 LessonDocumento9 páginasChapter 2 Acctg 1 Lessonizai vitorAún no hay calificaciones

- Module 1Documento5 páginasModule 1Charissa Jamis ChingwaAún no hay calificaciones

- Chapter 1 Intro To AcctgDocumento27 páginasChapter 1 Intro To AcctgJesseca JosafatAún no hay calificaciones

- Handouts Acctg 1Documento14 páginasHandouts Acctg 1technician laoAún no hay calificaciones

- Entrepreneurship Report 1Documento30 páginasEntrepreneurship Report 1Fretchie Anne LauroAún no hay calificaciones

- Income and Business TaxationDocumento24 páginasIncome and Business TaxationFerdinand Carlos B. DadoAún no hay calificaciones

- Market Segmentation, Targeting, and Positioning ForDocumento25 páginasMarket Segmentation, Targeting, and Positioning ForJeremy DupaganAún no hay calificaciones

- Week 5 Contemporary IssuesDocumento4 páginasWeek 5 Contemporary IssuesJasmin EspeletaAún no hay calificaciones

- Accounting Equation Exercises PDFDocumento1 páginaAccounting Equation Exercises PDFAdelle Bert DiazAún no hay calificaciones

- Accounts Notes For BCA - IncompleteDocumento56 páginasAccounts Notes For BCA - IncompleteSahil Kumar Gupta100% (1)

- Part 2 - Module 7 - The Nature of Merchandising Business 1Documento13 páginasPart 2 - Module 7 - The Nature of Merchandising Business 1jevieconsultaaquino2003Aún no hay calificaciones

- Business Finance: Financial Statement Preparation, Analysis, and InterpretationDocumento7 páginasBusiness Finance: Financial Statement Preparation, Analysis, and InterpretationRosalyn Mauricio VelascoAún no hay calificaciones

- Detailed Lesson Plan in Accounting 1Documento3 páginasDetailed Lesson Plan in Accounting 1Glezile DamirayAún no hay calificaciones

- Lesson Plan ABM Fundamentals of Accountancy, Business and ManagementDocumento13 páginasLesson Plan ABM Fundamentals of Accountancy, Business and Managementmarystel b. Borbon100% (1)

- Orgmngmt DLL Week 9Documento4 páginasOrgmngmt DLL Week 9Rizalyn AbilaAún no hay calificaciones

- TG #01 - ABM 006Documento9 páginasTG #01 - ABM 006Cyrill Paghangaan VitorAún no hay calificaciones

- History of AccountingDocumento22 páginasHistory of AccountingGia Patricia SalisiAún no hay calificaciones

- Abm PPT Week 1 and 2Documento50 páginasAbm PPT Week 1 and 2Robertojr sembranoAún no hay calificaciones

- Marketing Principles and StrategiesDocumento17 páginasMarketing Principles and StrategiesMagdalena OrdoñezAún no hay calificaciones

- Journalizing TransactionsDocumento5 páginasJournalizing TransactionsSatvik Bisht100% (1)

- Idea Lesson Nancy - Fabm2 FinalDocumento4 páginasIdea Lesson Nancy - Fabm2 FinalNancy AtentarAún no hay calificaciones

- Statement of Comprehensive Income (SCI) : Lesson 2Documento20 páginasStatement of Comprehensive Income (SCI) : Lesson 2Rojane L. AlcantaraAún no hay calificaciones

- Dvcpa Lesson 1 Handout 1 Fundamentals of Accounting Converted 2Documento6 páginasDvcpa Lesson 1 Handout 1 Fundamentals of Accounting Converted 2DV CPA REVIEWAún no hay calificaciones

- Package 1 (LT 1 - 6) Includes TutorialsDocumento102 páginasPackage 1 (LT 1 - 6) Includes TutorialsjacechanAún no hay calificaciones

- Finance Policies and Procedures Manual - TEMPLATEDocumento60 páginasFinance Policies and Procedures Manual - TEMPLATEHassan Liquat100% (2)

- Financial Accounting MD 1Documento87 páginasFinancial Accounting MD 1Robert KabweAún no hay calificaciones

- Acca NotesDocumento100 páginasAcca Notesasifkazmi100% (2)

- TOPIC: A.) Conceptual Framework and Elements of Financial StatementsDocumento6 páginasTOPIC: A.) Conceptual Framework and Elements of Financial StatementsADAún no hay calificaciones

- Finance Policies and Procedures Manual - TEMPLATE PDFDocumento60 páginasFinance Policies and Procedures Manual - TEMPLATE PDFIPFC CochinAún no hay calificaciones

- "The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"De Everand"The Language of Business: How Accounting Tells Your Story" "A Comprehensive Guide to Understanding, Interpreting, and Leveraging Financial Statements for Personal and Professional Success"Aún no hay calificaciones

- Accountancy and ManagementDocumento19 páginasAccountancy and ManagementLiwash SaikiaAún no hay calificaciones

- Giao Trinh Tacn Ke Toan Tai ChinhDocumento76 páginasGiao Trinh Tacn Ke Toan Tai ChinhMinh Lý TrịnhAún no hay calificaciones

- Fabm I SSLM Dennis M. Aujero Week 2Documento8 páginasFabm I SSLM Dennis M. Aujero Week 2DENNIS AUJEROAún no hay calificaciones

- Assignment 2 Accounting PrinciplesDocumento5 páginasAssignment 2 Accounting PrinciplesFelipe Mensorado GrandeAún no hay calificaciones

- What Is AccountingDocumento6 páginasWhat Is AccountingOtaku girlAún no hay calificaciones

- Puboff Ra 9006Documento8 páginasPuboff Ra 9006ccgomezAún no hay calificaciones

- Knitting For BeginnersDocumento2 páginasKnitting For BeginnersccgomezAún no hay calificaciones

- Lesson 1 - Handout 2 - The Financial Statements and Accounting EquationDocumento5 páginasLesson 1 - Handout 2 - The Financial Statements and Accounting EquationccgomezAún no hay calificaciones

- ACC30 Accounting For Partnerships Lesson Plan LiquidationDocumento4 páginasACC30 Accounting For Partnerships Lesson Plan Liquidationccgomez0% (1)

- E-Tailing: Challenges and Oppurtunities: A Self-Study Paper Submitted To Department of ManagementDocumento9 páginasE-Tailing: Challenges and Oppurtunities: A Self-Study Paper Submitted To Department of Managementreena sharmaAún no hay calificaciones

- Cars 24Documento6 páginasCars 24Manish Prabhat100% (1)

- HOMEWORKDocumento3 páginasHOMEWORKFranklin FiencoAún no hay calificaciones

- Cyber Security Unit 2Documento27 páginasCyber Security Unit 2Raj Kumar YadavAún no hay calificaciones

- Due Diligence Format (Jan 14)Documento10 páginasDue Diligence Format (Jan 14)Vivek GargAún no hay calificaciones

- Sps. Dela Cruz vs. Planters Products, Inc.Documento19 páginasSps. Dela Cruz vs. Planters Products, Inc.Alfred Lacandula0% (1)

- WWW - Ticketkaran.in Print TicketDocumento1 páginaWWW - Ticketkaran.in Print TicketkumarlntvAún no hay calificaciones

- Basic Accounting TermsDocumento13 páginasBasic Accounting TermsShivam Mutkule100% (1)

- NCWEB Admission 2021-22Documento21 páginasNCWEB Admission 2021-22vidishaniallerAún no hay calificaciones

- BIR Ruling 091-99 PDFDocumento6 páginasBIR Ruling 091-99 PDFleahtabsAún no hay calificaciones

- Emerging Modes of BusinessDocumento10 páginasEmerging Modes of BusinessdhruvrohatgiAún no hay calificaciones

- HSBC Qatar - Premier TariffDocumento16 páginasHSBC Qatar - Premier TariffjoeAún no hay calificaciones

- Company Letter Head: Letter of Request (Lor)Documento28 páginasCompany Letter Head: Letter of Request (Lor)Thomas HiggsAún no hay calificaciones

- Peachtree Users Manual CompleteDocumento317 páginasPeachtree Users Manual CompleteTAS_ALPHA100% (2)

- Paper Industries Corp v. CADocumento3 páginasPaper Industries Corp v. CAPio MathayAún no hay calificaciones

- Chapter 03: Electronic Payment System: By: Diwakar UpadhyayaDocumento67 páginasChapter 03: Electronic Payment System: By: Diwakar UpadhyayaBibek karnaAún no hay calificaciones

- PHP ReadmeDocumento3 páginasPHP ReadmeAdita Rini SusilowatiAún no hay calificaciones

- Abdul K Kallon Financial Disclosure Report For Kallon, Abdul KDocumento15 páginasAbdul K Kallon Financial Disclosure Report For Kallon, Abdul KJudicial Watch, Inc.Aún no hay calificaciones

- (1/1 Point) : Correct Answers: FALSEDocumento20 páginas(1/1 Point) : Correct Answers: FALSELawrence YusiAún no hay calificaciones

- T3SCAT - Securities Administration & Trading - Front OfficeDocumento294 páginasT3SCAT - Securities Administration & Trading - Front OfficeAlexandra Sache100% (7)

- EY-Smart Commerce Battling For Customers in Digital RetailDocumento40 páginasEY-Smart Commerce Battling For Customers in Digital RetailEuglena VerdeAún no hay calificaciones

- Principles of Accounting I - Converted-MinDocumento5 páginasPrinciples of Accounting I - Converted-Minsamuel zelaelmAún no hay calificaciones

- Buyers Procedures For Historic BondsDocumento2 páginasBuyers Procedures For Historic Bondsshahil_4uAún no hay calificaciones

- Global Investment Banking & Brokerage Industry ReportDocumento38 páginasGlobal Investment Banking & Brokerage Industry ReportJessyAún no hay calificaciones

- Transaction CycleDocumento5 páginasTransaction CycleMinhoAún no hay calificaciones

- Table - Names and DescriptionDocumento13 páginasTable - Names and DescriptionMohammed ReyazAún no hay calificaciones

- So A 900920160610Documento1 páginaSo A 900920160610Francisco Oringo Sr ESAún no hay calificaciones

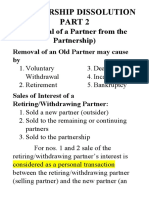

- Chapter 5 - Partnership Dissolution Part 2Documento7 páginasChapter 5 - Partnership Dissolution Part 2Xyzra AlfonsoAún no hay calificaciones

- CASBA User Manual: AnnouncementDocumento53 páginasCASBA User Manual: Announcementjosy100% (4)

- Renewal Premium Acknowledgement: Policy DetailsDocumento1 páginaRenewal Premium Acknowledgement: Policy DetailsTejpal Singh ShekhawatAún no hay calificaciones