También podría gustarte

- Cec 103. - Workshop Technology 1Documento128 páginasCec 103. - Workshop Technology 1VietHungCao92% (13)

- PDS OperatorStationDocumento7 páginasPDS OperatorStationMisael Castillo CamachoAún no hay calificaciones

- Max Born, Albert Einstein-The Born-Einstein Letters-Macmillan (1971)Documento132 páginasMax Born, Albert Einstein-The Born-Einstein Letters-Macmillan (1971)Brian O'SullivanAún no hay calificaciones

- Water Reducing - Retarding AdmixturesDocumento17 páginasWater Reducing - Retarding AdmixturesAbdullah PathanAún no hay calificaciones

- Control PhilosophyDocumento2 páginasControl PhilosophytsplinstAún no hay calificaciones

- Homa 2 CalculatorDocumento6 páginasHoma 2 CalculatorAnonymous 4dE7mUCIH0% (1)

- Qualcomm LTE Performance & Challenges 09-01-2011Documento29 páginasQualcomm LTE Performance & Challenges 09-01-2011vembri2178100% (1)

- Marketing Concept NPODocumento26 páginasMarketing Concept NPOKristy LeAún no hay calificaciones

- Tablas Modulo1 PDFDocumento5 páginasTablas Modulo1 PDFWilfredo RiveraAún no hay calificaciones

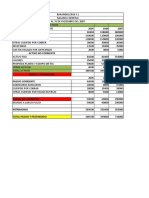

- Balance GeneralDocumento3 páginasBalance Generaledgardo duranAún no hay calificaciones

- Chapter 4 Audit Evidence Documentation Compatibility ModeDocumento33 páginasChapter 4 Audit Evidence Documentation Compatibility ModeAnh PhamAún no hay calificaciones

- Contabilidad de Costos Sinesterra 50 - 89Documento40 páginasContabilidad de Costos Sinesterra 50 - 89ariel502010Aún no hay calificaciones

- Narver and Slater, Kohli and Jaworski and The Market Orientation Construct: Integration and InternationalizationDocumento21 páginasNarver and Slater, Kohli and Jaworski and The Market Orientation Construct: Integration and Internationalizationbennie7390Aún no hay calificaciones

- Jaworski and Kohli 1993Documento19 páginasJaworski and Kohli 1993stiffsn100% (1)

- Cultural and Behavioral Adoption of Market Orientation FormsDocumento10 páginasCultural and Behavioral Adoption of Market Orientation FormsbalbalAún no hay calificaciones

- Market Orientation: Antecedents and ConsequencesDocumento19 páginasMarket Orientation: Antecedents and ConsequencesSalas MazizAún no hay calificaciones

- The Effects of Strategy Type On The Market Orientation-Performance RelationshipDocumento17 páginasThe Effects of Strategy Type On The Market Orientation-Performance RelationshipEmmy SukhAún no hay calificaciones

- Kirca Et Al 2005 Market Orientation A Meta Analytic Review and Assessment of Its Antecedents and Impact On PerformanceDocumento18 páginasKirca Et Al 2005 Market Orientation A Meta Analytic Review and Assessment of Its Antecedents and Impact On PerformanceBart WolsingAún no hay calificaciones

- Petency MODocumento21 páginasPetency MOjohnalis22Aún no hay calificaciones

- Market Orientation in Pakistani CompaniesDocumento26 páginasMarket Orientation in Pakistani Companiessgggg0% (1)

- Market OrientationDocumento40 páginasMarket OrientationBoogii EnkhboldAún no hay calificaciones

- Interfunctional Dynamics and Firm Performance: A Comparison Between Firms in Poland and The United StatesDocumento19 páginasInterfunctional Dynamics and Firm Performance: A Comparison Between Firms in Poland and The United StatesLeila BenmansourAún no hay calificaciones

- An Analysis of The MKTOR and MARKOR Measures of MaDocumento12 páginasAn Analysis of The MKTOR and MARKOR Measures of MaArvind ShuklaAún no hay calificaciones

- Kara 2005Documento14 páginasKara 2005Nicolás MárquezAún no hay calificaciones

- Theory, Research and Practice in Library Management 8: Market OrientationDocumento10 páginasTheory, Research and Practice in Library Management 8: Market OrientationWan Ahmad FadirAún no hay calificaciones

- Jurnal CRMDocumento19 páginasJurnal CRMYudha PriambodoAún no hay calificaciones

- Cultural vs. Operational Market Orientation and Objective vs. Subjective Performance: Perspective of Production and OperationsDocumento33 páginasCultural vs. Operational Market Orientation and Objective vs. Subjective Performance: Perspective of Production and Operationssamas7480Aún no hay calificaciones

- Corporate Culture, Customer Orientation, and Innovativeness Japanese Firms: A Quadrad AnalysisDocumento15 páginasCorporate Culture, Customer Orientation, and Innovativeness Japanese Firms: A Quadrad AnalysisAndrés GómezAún no hay calificaciones

- Effect of SMO On Manufacturer's Trust - Zhao 2005pdfDocumento10 páginasEffect of SMO On Manufacturer's Trust - Zhao 2005pdfElaine Antonette RositaAún no hay calificaciones

- Market Orientation and Entrepreneurial Culture Drive Business ProfitabilityDocumento5 páginasMarket Orientation and Entrepreneurial Culture Drive Business ProfitabilityIng Raul OrozcoAún no hay calificaciones

- MB V8 A3 Farrell PDFDocumento11 páginasMB V8 A3 Farrell PDFHexaNotesAún no hay calificaciones

- Relationship Between Desired & Achieved Market Orientation LevelsDocumento17 páginasRelationship Between Desired & Achieved Market Orientation Levels:-*kiss youAún no hay calificaciones

- The Journey From Market Orientation To Firm Performance: A Comparative Study of US and Taiwanese SmesDocumento13 páginasThe Journey From Market Orientation To Firm Performance: A Comparative Study of US and Taiwanese Smesbandi_2340Aún no hay calificaciones

- Jaworski Jaworski and Kohliand KohliDocumento19 páginasJaworski Jaworski and Kohliand KohliSmucek87Aún no hay calificaciones

- Family Business and Market Orientationthesis PDFDocumento19 páginasFamily Business and Market Orientationthesis PDFFrancis RiveroAún no hay calificaciones

- Measuring Marketing OrientationDocumento2 páginasMeasuring Marketing OrientationFrancis RiveroAún no hay calificaciones

- Being Entrepreneurial and Market Driven: Implications For Company PerformanceDocumento18 páginasBeing Entrepreneurial and Market Driven: Implications For Company PerformanceEsrael WaworuntuAún no hay calificaciones

- Linking Strategic and Market Orientations To Organizat 2013 Procedia SociaDocumento7 páginasLinking Strategic and Market Orientations To Organizat 2013 Procedia SociabalbalAún no hay calificaciones

- Master of Business Adminstration Marketing OrientationDocumento11 páginasMaster of Business Adminstration Marketing OrientationQuảng Nguyễn ĐìnhAún no hay calificaciones

- RSM Erasmus University, Rotterdam, The Netherlands, andDocumento49 páginasRSM Erasmus University, Rotterdam, The Netherlands, andMahipal18Aún no hay calificaciones

- American Marketing AssociationDocumento23 páginasAmerican Marketing AssociationpadmavathiAún no hay calificaciones

- A New Perspective On Market Dynamics: Market Plasticity and The Stability-Fluidity DialecticsDocumento21 páginasA New Perspective On Market Dynamics: Market Plasticity and The Stability-Fluidity DialecticslomahanaAún no hay calificaciones

- ATM PositioningDocumento17 páginasATM PositioningNguyễn Tiến LâmAún no hay calificaciones

- Executive Insights. Market Orientation of Mexican CompaniesDocumento18 páginasExecutive Insights. Market Orientation of Mexican CompaniesRicardo Santos GarcíaAún no hay calificaciones

- KOTTIKA - Market-Driving - Strategy - and - Personnel - Attributes - 2018Documento41 páginasKOTTIKA - Market-Driving - Strategy - and - Personnel - Attributes - 2018Ferdous AminAún no hay calificaciones

- Organizational Culture and Job SatisfactionDocumento18 páginasOrganizational Culture and Job SatisfactionryarezsaAún no hay calificaciones

- Critical Perspective On Motivation TheoriesDocumento20 páginasCritical Perspective On Motivation TheoriesHoang Vy Le DinhAún no hay calificaciones

- Positioning Strategies of Services, BlanksonDocumento16 páginasPositioning Strategies of Services, BlanksonKatarina PanićAún no hay calificaciones

- Market Orientation Kohli and JaworskiDocumento19 páginasMarket Orientation Kohli and JaworskiSara KhanAún no hay calificaciones

- Towards An Institution-Based View of Business Strategy: 2002 Kluwer Academic Publishers. Manufactured in The NetherlandsDocumento18 páginasTowards An Institution-Based View of Business Strategy: 2002 Kluwer Academic Publishers. Manufactured in The NetherlandsSurekha NayakAún no hay calificaciones

- Article 2Documento17 páginasArticle 2Feven WenduAún no hay calificaciones

- The Measurement of Strategic Orientation and Its Efficacy in Predicting Financial PerformanceDocumento21 páginasThe Measurement of Strategic Orientation and Its Efficacy in Predicting Financial PerformanceDwitya AribawaAún no hay calificaciones

- Venter, P, Wright, A & Dibb, S 2015, Performing Market SegmentationDocumento36 páginasVenter, P, Wright, A & Dibb, S 2015, Performing Market SegmentationAhmad DarojiAún no hay calificaciones

- Deshpande 1989Documento14 páginasDeshpande 1989Jihene ChebbiAún no hay calificaciones

- Zeljko BunicDocumento17 páginasZeljko BunicGoltman SvAún no hay calificaciones

- American Marketing AssociationDocumento16 páginasAmerican Marketing AssociationMohamed SellamnaAún no hay calificaciones

- Ikea Ki Kya Aat GeDocumento37 páginasIkea Ki Kya Aat GeFurqangreatAún no hay calificaciones

- Capabilities and Financial PerformanceDocumento17 páginasCapabilities and Financial Performancemesay83Aún no hay calificaciones

- Converging On A New Theoretical Foundation For SellingDocumento18 páginasConverging On A New Theoretical Foundation For SellingJorge IvanAún no hay calificaciones

- Capabilities For Market-Shaping - Triggering and Facilitating Increased Value CreationDocumento24 páginasCapabilities For Market-Shaping - Triggering and Facilitating Increased Value CreationMariaAún no hay calificaciones

- Marketing and InnovationDocumento10 páginasMarketing and Innovationmedusa alfaidzeAún no hay calificaciones

- Kohli and Jaworski - Market OrientationDocumento19 páginasKohli and Jaworski - Market Orientationprayas_taraniAún no hay calificaciones

- How Context Frames Exchange and Value Co-CreationDocumento15 páginasHow Context Frames Exchange and Value Co-CreationTariq Waheed QureshiAún no hay calificaciones

- Prikaz Literature Za Ok, Liderstvo I PromeneDocumento34 páginasPrikaz Literature Za Ok, Liderstvo I PromeneDanka GrubicAún no hay calificaciones

- Toward A Deeper Understanding of Service PDFDocumento17 páginasToward A Deeper Understanding of Service PDFTriyoga RahmawanAún no hay calificaciones

- 10.1007@s11002 020 09529 5Documento12 páginas10.1007@s11002 020 09529 5The Armwrestling HubAún no hay calificaciones

- 1 s2.0 S0019850106000836 MainimpDocumento15 páginas1 s2.0 S0019850106000836 Mainimpsamas7480Aún no hay calificaciones

- 2.6 Rational Functions Asymptotes TutorialDocumento30 páginas2.6 Rational Functions Asymptotes TutorialAljun Aldava BadeAún no hay calificaciones

- Impedance Measurement Handbook: 1st EditionDocumento36 páginasImpedance Measurement Handbook: 1st EditionAlex IslasAún no hay calificaciones

- MITRES 6 002S08 Chapter2Documento87 páginasMITRES 6 002S08 Chapter2shalvinAún no hay calificaciones

- Lesson 1Documento24 páginasLesson 1Jayzelle100% (1)

- R8557B KCGGDocumento178 páginasR8557B KCGGRinda_RaynaAún no hay calificaciones

- Jaguar Land Rover Configuration Lifecycle Management WebDocumento4 páginasJaguar Land Rover Configuration Lifecycle Management WebStar Nair Rock0% (1)

- Technical Data: Pump NameDocumento6 páginasTechnical Data: Pump Nameسمير البسيونىAún no hay calificaciones

- UnderstandingCryptology CoreConcepts 6-2-2013Documento128 páginasUnderstandingCryptology CoreConcepts 6-2-2013zenzei_Aún no hay calificaciones

- Reference Mil-Aero Guide ConnectorDocumento80 páginasReference Mil-Aero Guide ConnectorjamesclhAún no hay calificaciones

- Data AnalysisDocumento7 páginasData AnalysisAndrea MejiaAún no hay calificaciones

- Turbine Buyers Guide - Mick Sagrillo & Ian WoofendenDocumento7 páginasTurbine Buyers Guide - Mick Sagrillo & Ian WoofendenAnonymous xYhjeilnZAún no hay calificaciones

- Design of Shaft Straightening MachineDocumento58 páginasDesign of Shaft Straightening MachineChiragPhadkeAún no hay calificaciones

- ENGG1330 2N Computer Programming I (20-21 Semester 2) Assignment 1Documento5 páginasENGG1330 2N Computer Programming I (20-21 Semester 2) Assignment 1Fizza JafferyAún no hay calificaciones

- Kalayaan Elementary SchoolDocumento3 páginasKalayaan Elementary SchoolEmmanuel MejiaAún no hay calificaciones

- Biogen 2021Documento12 páginasBiogen 2021taufiq hidAún no hay calificaciones

- Pumps - IntroductionDocumento31 páginasPumps - IntroductionSuresh Thangarajan100% (1)

- User Mode I. System Support Processes: de Leon - Dolliente - Gayeta - Rondilla It201 - Platform Technology - TPDocumento6 páginasUser Mode I. System Support Processes: de Leon - Dolliente - Gayeta - Rondilla It201 - Platform Technology - TPCariza DollienteAún no hay calificaciones

- Shares Dan Yang Belum Diterbitkan Disebut Unissued SharesDocumento5 páginasShares Dan Yang Belum Diterbitkan Disebut Unissued Sharesstefanus budiAún no hay calificaciones

- M.E. Comm. SystemsDocumento105 páginasM.E. Comm. SystemsShobana SAún no hay calificaciones

- Python - How To Compute Jaccard Similarity From A Pandas Dataframe - Stack OverflowDocumento4 páginasPython - How To Compute Jaccard Similarity From A Pandas Dataframe - Stack OverflowJession DiwanganAún no hay calificaciones

- PDF Solution Manual For Gas Turbine Theory 6th Edition Saravanamuttoo Rogers CompressDocumento7 páginasPDF Solution Manual For Gas Turbine Theory 6th Edition Saravanamuttoo Rogers CompressErickson Brayner MarBerAún no hay calificaciones

- Submittal Chiller COP 6.02Documento3 páginasSubmittal Chiller COP 6.02juan yenqueAún no hay calificaciones

- Eurotech IoT Gateway Reliagate 10 12 ManualDocumento88 páginasEurotech IoT Gateway Reliagate 10 12 Manualfelix olguinAún no hay calificaciones