También podría gustarte

- Chapter 1 - PartnershipDocumento72 páginasChapter 1 - PartnershipJohn Lloyd Yasto100% (5)

- Afar Concept Review Notes Part 1Documento13 páginasAfar Concept Review Notes Part 1Alexis SosingAún no hay calificaciones

- Finding Balance 2019: Benchmarking the Performance of State-Owned Banks in the PacificDe EverandFinding Balance 2019: Benchmarking the Performance of State-Owned Banks in the PacificAún no hay calificaciones

- LBODocumento42 páginasLBOSandeep Kumar100% (1)

- Working Capital Position of Siddhartha BankDocumento36 páginasWorking Capital Position of Siddhartha BankKhadka Manish71% (21)

- State Bank of IndiaDocumento37 páginasState Bank of IndiarooappuAún no hay calificaciones

- Banking ProjectDocumento91 páginasBanking Projectmridulakhanna84% (200)

- Asia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexDe EverandAsia Small and Medium-Sized Enterprise Monitor 2020: Volume IV: Technical Note—Designing a Small and Medium-Sized Enterprise Development IndexAún no hay calificaciones

- Modernizing Banking ServicesDocumento78 páginasModernizing Banking ServicesDharmikAún no hay calificaciones

- Regional Rural Banks of India: Evolution, Performance and ManagementDe EverandRegional Rural Banks of India: Evolution, Performance and ManagementAún no hay calificaciones

- Mba Project Report On Central BankDocumento74 páginasMba Project Report On Central BankDeepak Mangal40% (5)

- Financial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeDe EverandFinancial Inclusion for Micro, Small, and Medium Enterprises in Kazakhstan: ADB Support for Regional Cooperation and Integration across Asia and the Pacific during Unprecedented Challenge and ChangeAún no hay calificaciones

- Internship Report On MCB Bank LimitedDocumento42 páginasInternship Report On MCB Bank Limitedbbaahmad89Aún no hay calificaciones

- Marketing Activities of Products and Services of The City Bank LimitedDocumento61 páginasMarketing Activities of Products and Services of The City Bank LimitedZiaul Onim0% (1)

- Alia AccountsDocumento182 páginasAlia AccountsAnonymous wZ81HensAún no hay calificaciones

- Address: Jhang Road, Opposite MCB Bank Ltd. Muzaffargarh. PH: 0662-2423350-2424350Documento14 páginasAddress: Jhang Road, Opposite MCB Bank Ltd. Muzaffargarh. PH: 0662-2423350-2424350Basit KhanAún no hay calificaciones

- Syndicate-Bank Company ProfileDocumento13 páginasSyndicate-Bank Company ProfileSanthosh SomaAún no hay calificaciones

- Projects - "CUSTOMER RELATIONSHIP MANAGEMENT IN BANKS WITH REFERENCE TO CORPORATION BANKDocumento38 páginasProjects - "CUSTOMER RELATIONSHIP MANAGEMENT IN BANKS WITH REFERENCE TO CORPORATION BANKRahul Singh100% (2)

- DiruDocumento84 páginasDirudhiru_hadiaAún no hay calificaciones

- 2012 City Bank Aims For Greater Heights 2012Documento4 páginas2012 City Bank Aims For Greater Heights 2012nurul000Aún no hay calificaciones

- Raj Bank Ratio Analysis PDFDocumento72 páginasRaj Bank Ratio Analysis PDFRonak VaishnavAún no hay calificaciones

- ICICI Bank Business StrategyDocumento18 páginasICICI Bank Business StrategyVimal93Aún no hay calificaciones

- Performance Appraisal System of AB Bank LTDDocumento67 páginasPerformance Appraisal System of AB Bank LTDMahmud Abdullah100% (1)

- The Bank of Punjab Latest Internship Report With Three Years Financial DataDocumento23 páginasThe Bank of Punjab Latest Internship Report With Three Years Financial DataMuhammad Taif KhanAún no hay calificaciones

- Project On: Submitted ToDocumento72 páginasProject On: Submitted ToMohmmad IqbalAún no hay calificaciones

- Loans and AdvancesDocumento49 páginasLoans and Advancesravi kangneAún no hay calificaciones

- J&K Bank Performance HighlightsDocumento13 páginasJ&K Bank Performance HighlightsUman MushtaqAún no hay calificaciones

- ETLI Annual Report 2022-23Documento214 páginasETLI Annual Report 2022-23ompatelAún no hay calificaciones

- TypeDocumento20 páginasTypeakshayAún no hay calificaciones

- Term Paper Service Marketing RT1802A10Documento35 páginasTerm Paper Service Marketing RT1802A10rajiv kumarAún no hay calificaciones

- Internship Report On MCB Bank LimitedDocumento40 páginasInternship Report On MCB Bank Limitedbbaahmad89Aún no hay calificaciones

- Customer Relationship Management PDFDocumento50 páginasCustomer Relationship Management PDFArif BashirAún no hay calificaciones

- Assignment MKT Mba 1Documento6 páginasAssignment MKT Mba 1Nahid BhuiyanAún no hay calificaciones

- SbiDocumento36 páginasSbiGaganjot SinghAún no hay calificaciones

- Ratio Analysis Uttara Bank VS City BankDocumento70 páginasRatio Analysis Uttara Bank VS City BankTaznina Nur MuntahaAún no hay calificaciones

- COMPANY PROFILE - OdtDocumento13 páginasCOMPANY PROFILE - OdtkailashAún no hay calificaciones

- Corporation Bank ProjectDocumento65 páginasCorporation Bank ProjectAjay MasseyAún no hay calificaciones

- CRM in BankDocumento78 páginasCRM in BankSaurabh MaheshwariAún no hay calificaciones

- Sarswat Bank in ShortDocumento22 páginasSarswat Bank in ShortKrishan BhagwaniAún no hay calificaciones

- MCB Bank Internship ReportDocumento41 páginasMCB Bank Internship ReportAmanullah KhanAún no hay calificaciones

- Budgeting and Its Impact On Performance of Commercial Bank (A Case Study On Dicha Branch)Documento54 páginasBudgeting and Its Impact On Performance of Commercial Bank (A Case Study On Dicha Branch)meseret sisayAún no hay calificaciones

- New Major ProjectDocumento50 páginasNew Major Projectgeetumittal65Aún no hay calificaciones

- Products Offered by HDFC BankDocumento80 páginasProducts Offered by HDFC BankUmar ThukarAún no hay calificaciones

- Employee Job Satisfaction at Ellaquai Dehati BankDocumento64 páginasEmployee Job Satisfaction at Ellaquai Dehati BankSwyam DuggalAún no hay calificaciones

- Pragathi Bank customer satisfaction surveyDocumento15 páginasPragathi Bank customer satisfaction surveySatveer SinghAún no hay calificaciones

- Canara Bank ProfileDocumento13 páginasCanara Bank ProfileRaveendra BatageriAún no hay calificaciones

- Internship-Report-on-General-Banking-of-Janata-Bank-Limited 2Documento35 páginasInternship-Report-on-General-Banking-of-Janata-Bank-Limited 2Bronson CastroAún no hay calificaciones

- Chapter - I: Profile of TMB Tamilnad Mercantile Bank Limited (TMB) Is A Bank Headquartered atDocumento29 páginasChapter - I: Profile of TMB Tamilnad Mercantile Bank Limited (TMB) Is A Bank Headquartered atPoojaAún no hay calificaciones

- Banking Internship ExperienceDocumento72 páginasBanking Internship ExperienceShahjalal Sumon100% (1)

- Raj Bank PPT 2003Documento32 páginasRaj Bank PPT 2003Sunny Bhatt100% (1)

- HRM370-CASE 1-NCC BankDocumento16 páginasHRM370-CASE 1-NCC BankOishee AhmedAún no hay calificaciones

- Ankita's Summer Project ReportDocumento29 páginasAnkita's Summer Project ReportKamal More100% (7)

- ReportDocumento9 páginasReportLakshya AggarwalAún no hay calificaciones

- Internship Report: NOON Business School University of SargodhaDocumento25 páginasInternship Report: NOON Business School University of Sargodhaanees razaAún no hay calificaciones

- Report On NCC Bank Ltd.Documento28 páginasReport On NCC Bank Ltd.cap_dubois100% (3)

- Finance ProjectDocumento50 páginasFinance ProjectGOURAVAún no hay calificaciones

- Bank of Maharashtra ProjectDocumento39 páginasBank of Maharashtra Projectchakshyutgupta76% (21)

- Union Bank Limited Internship ReportDocumento60 páginasUnion Bank Limited Internship Reportsaleemkhp50% (2)

- INTERNSHIP REPORT in Prime Bank Limited - BD For Asian University of Bangladesh - DhakaDocumento50 páginasINTERNSHIP REPORT in Prime Bank Limited - BD For Asian University of Bangladesh - DhakaTouhidul Islam83% (6)

- A Study of Small and Medium Enterprises Loans Ing Vsaya BankDocumento95 páginasA Study of Small and Medium Enterprises Loans Ing Vsaya BankSilvi KhuranaAún no hay calificaciones

- Project Vijaya Bank FinalDocumento62 páginasProject Vijaya Bank FinalNalina Gs G100% (1)

- T R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)De EverandT R A N S F O R M A T I O N: THREE DECADES OF INDIA’S FINANCIAL AND BANKING SECTOR REFORMS (1991–2021)Aún no hay calificaciones

- Effective Project Financing Essential Principles And Tactics: An Introduction To Finance, Cash Flows, And Project EvaluationDe EverandEffective Project Financing Essential Principles And Tactics: An Introduction To Finance, Cash Flows, And Project EvaluationAún no hay calificaciones

- Online Platforms, Pandemic, and Business Resilience in Indonesia: A Joint Study by Gojek and the Asian Development BankDe EverandOnline Platforms, Pandemic, and Business Resilience in Indonesia: A Joint Study by Gojek and the Asian Development BankAún no hay calificaciones

- Sevket - Pamuk - Prices in The Ottoman Empire - 1469-1914Documento18 páginasSevket - Pamuk - Prices in The Ottoman Empire - 1469-1914Hristiyan AtanasovAún no hay calificaciones

- Term Paper On Inflation in NigeriaDocumento11 páginasTerm Paper On Inflation in Nigeriac5ha8c7g100% (1)

- Indian BankDocumento94 páginasIndian Banknanisir100% (1)

- Friday Bulletin 398Documento8 páginasFriday Bulletin 398Wajid CockarAún no hay calificaciones

- In Problem 10 16 We Projected Financial Statements For Wal Mart Stores 126776Documento2 páginasIn Problem 10 16 We Projected Financial Statements For Wal Mart Stores 126776Amit PandeyAún no hay calificaciones

- Analyzing Punjab National Bank Scam: June 2019Documento9 páginasAnalyzing Punjab National Bank Scam: June 2019TejaswiniAún no hay calificaciones

- B V M Engineering College Vallabh VidyanagarDocumento9 páginasB V M Engineering College Vallabh VidyanagarShish DattaAún no hay calificaciones

- Chapter 2 Overview Financial Risk MGMT Questions and Answers-RevisedDocumento3 páginasChapter 2 Overview Financial Risk MGMT Questions and Answers-RevisedSahaana VijayAún no hay calificaciones

- Accountancy XII Exam Handbook For 2024 ExamDocumento88 páginasAccountancy XII Exam Handbook For 2024 ExamHari prakarsh Nimi100% (1)

- LazyPay-General Terms and ConditionsDocumento15 páginasLazyPay-General Terms and Conditionsramakrishnan balanAún no hay calificaciones

- Chapter 12 Bond Portfolio MGMTDocumento32 páginasChapter 12 Bond Portfolio MGMTAanchalAún no hay calificaciones

- Banco Filipino Savings and Mortgage Bank v. YbanezDocumento14 páginasBanco Filipino Savings and Mortgage Bank v. YbanezArnold BagalanteAún no hay calificaciones

- RIL IR2022 FinancialPerformanceDocumento10 páginasRIL IR2022 FinancialPerformanceMansiAún no hay calificaciones

- The Kerala Stamp Act 1959Documento45 páginasThe Kerala Stamp Act 1959Deepesh KumarAún no hay calificaciones

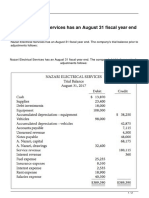

- Nazari Electrical Services Has An August 31 Fiscal Year EndDocumento2 páginasNazari Electrical Services Has An August 31 Fiscal Year EndCharlotteAún no hay calificaciones

- Air Asia Financial AnalysisDocumento16 páginasAir Asia Financial AnalysisMohamed ShaminAún no hay calificaciones

- Mind-Map - Marathon NotesDocumento10 páginasMind-Map - Marathon NotesMd. Sohail Raza100% (1)

- 2019 NVC FS and NotesDocumento23 páginas2019 NVC FS and NotesNVC FoundationAún no hay calificaciones

- Bonds and NotesDocumento3 páginasBonds and Notesjano_art21Aún no hay calificaciones

- Loan EMI CalculatorDocumento7 páginasLoan EMI CalculatorjayantsAún no hay calificaciones

- Toa 41 42 PDFDocumento22 páginasToa 41 42 PDFspur iousAún no hay calificaciones

- FR - Study Hub - Flash CardsDocumento14 páginasFR - Study Hub - Flash CardsFalguni PurohitAún no hay calificaciones

- Philippines - France Tax Treaty and ProtocolDocumento35 páginasPhilippines - France Tax Treaty and ProtocolDanzki BadiqueAún no hay calificaciones

- Self Study Exercises Chapter 6 With AnswersDocumento23 páginasSelf Study Exercises Chapter 6 With AnswersDeng JuniorAún no hay calificaciones

- Unit 9: Financial Information SystemDocumento13 páginasUnit 9: Financial Information SystemSrishti VivekAún no hay calificaciones

- Fixed Income Securities NumericalsDocumento5 páginasFixed Income Securities NumericalsNatraj PandeyAún no hay calificaciones