También podría gustarte

- Renewable Energy for Agriculture: Insights from Southeast AsiaDe EverandRenewable Energy for Agriculture: Insights from Southeast AsiaAún no hay calificaciones

- Energy Efficiency in South Asia: Opportunities for Energy Sector TransformationDe EverandEnergy Efficiency in South Asia: Opportunities for Energy Sector TransformationAún no hay calificaciones

- Chairperson, PNGRB (080110)Documento44 páginasChairperson, PNGRB (080110)Sainu KalathingalAún no hay calificaciones

- Dannif DanusaputroDocumento9 páginasDannif DanusaputroReza HaryohatmodjoAún no hay calificaciones

- BP Energy Outlook 2019 Country Insight IndiaDocumento2 páginasBP Energy Outlook 2019 Country Insight IndiaAnant vikram singhAún no hay calificaciones

- Energy Scenario & Related Policies in BangladeshDocumento27 páginasEnergy Scenario & Related Policies in BangladesharpondevAún no hay calificaciones

- Role of Energy in Balanced Sectorial GrowthDocumento11 páginasRole of Energy in Balanced Sectorial GrowthDharmesh KalsariaAún no hay calificaciones

- 2015-09-17 PM 12 by Li Yao CNDocumento21 páginas2015-09-17 PM 12 by Li Yao CNDare SmithAún no hay calificaciones

- SolarStorageReport - JMK Research - Jan 2020 2 PDFDocumento32 páginasSolarStorageReport - JMK Research - Jan 2020 2 PDFiyer34Aún no hay calificaciones

- A Road Map For An Energy Independent Sri Lanka by 2030: Eng Parakrama JayasingheDocumento38 páginasA Road Map For An Energy Independent Sri Lanka by 2030: Eng Parakrama JayasingheAnuradha wkvAún no hay calificaciones

- BP Energy Outlook 2017 Country Insight IndiaDocumento2 páginasBP Energy Outlook 2017 Country Insight IndiasamAún no hay calificaciones

- 6 Refineries PDFDocumento27 páginas6 Refineries PDFMinh PhuongAún no hay calificaciones

- Innovation For The Energy Transition Preliminary FindingDocumento26 páginasInnovation For The Energy Transition Preliminary FindingJohn BenderAún no hay calificaciones

- Corporate Catalyst India A Report On Indian Power and Energy IndustryDocumento35 páginasCorporate Catalyst India A Report On Indian Power and Energy IndustryThanga PrakashAún no hay calificaciones

- Highlight of RUEN - Ver EnglishDocumento15 páginasHighlight of RUEN - Ver EnglishLuthfieSangKaptenAún no hay calificaciones

- M1 P1 Energy Review World and India DR R R JoshiDocumento36 páginasM1 P1 Energy Review World and India DR R R JoshiAkshat RawatAún no hay calificaciones

- Power - Year Update and OutlookDocumento6 páginasPower - Year Update and OutlookRahul SainiAún no hay calificaciones

- Energy Crises in Pakistan ??Documento48 páginasEnergy Crises in Pakistan ??Malik Afzaal AwanAún no hay calificaciones

- 1-1slide K SUCHADA-hydroDocumento61 páginas1-1slide K SUCHADA-hydroPae RangsanAún no hay calificaciones

- DREI Booklet EnglishDocumento17 páginasDREI Booklet EnglishPawan TiwariAún no hay calificaciones

- RE in MalaysiaDocumento25 páginasRE in MalaysiaAzraqul IlmiAún no hay calificaciones

- IRENA REmap Indonesia Summary 2017 PDFDocumento14 páginasIRENA REmap Indonesia Summary 2017 PDFwitdono100% (1)

- Market Brief Saudi ArabiaDocumento4 páginasMarket Brief Saudi ArabiaregallydivineAún no hay calificaciones

- Review of Gas Based Power Technologies - Gas Turbines: Robin W. AmesDocumento37 páginasReview of Gas Based Power Technologies - Gas Turbines: Robin W. AmesAndri YantoAún no hay calificaciones

- Sbi Energy Opportunities Fund LeafletDocumento4 páginasSbi Energy Opportunities Fund LeafletJoseph T VAún no hay calificaciones

- VietNam GangubaiDocumento44 páginasVietNam GangubaiTrang NguyenAún no hay calificaciones

- Coal To Urea at TalcherDocumento37 páginasCoal To Urea at TalcherAlfin A. N.Aún no hay calificaciones

- Opportunities and Challenges For Solar PV Rooftop in IndonesiaDocumento24 páginasOpportunities and Challenges For Solar PV Rooftop in IndonesiaIskandarAún no hay calificaciones

- BP Energy Outlook 2020 Country Insight ChinaDocumento2 páginasBP Energy Outlook 2020 Country Insight ChinaJaret FajriantoAún no hay calificaciones

- Cognizance Group Welcome YouDocumento58 páginasCognizance Group Welcome Yousudhakar jhaAún no hay calificaciones

- Energies: Review of Potential and Actual Penetration of Solar Power in VietnamDocumento25 páginasEnergies: Review of Potential and Actual Penetration of Solar Power in VietnamhnmjzhviAún no hay calificaciones

- (Stu Z) The - Economist.august.01st August.07th.2009Documento9 páginas(Stu Z) The - Economist.august.01st August.07th.2009vikashbh043Aún no hay calificaciones

- Natural Gas Scenario in IndiaDocumento28 páginasNatural Gas Scenario in IndiaShweta Suresh100% (1)

- Welcome To Presentation: Depletable Resource Allocation in BangladeshDocumento16 páginasWelcome To Presentation: Depletable Resource Allocation in BangladeshWalid HasanAún no hay calificaciones

- E&P Opportunities: Pakistan Petroleum LimitedDocumento53 páginasE&P Opportunities: Pakistan Petroleum Limitednasir.hdip8468Aún no hay calificaciones

- E - Overview of The Vietnamese Energy Sector - EREADocumento17 páginasE - Overview of The Vietnamese Energy Sector - EREAnamakAún no hay calificaciones

- Hafidi Session3Documento19 páginasHafidi Session3oussama jamalAún no hay calificaciones

- Insights 2030 Energy Mix Marching Towards A Cleaner FutureDocumento80 páginasInsights 2030 Energy Mix Marching Towards A Cleaner Future@yuanAún no hay calificaciones

- Indian Energy ScenarioDocumento17 páginasIndian Energy ScenarioTony StarkAún no hay calificaciones

- BS Simon MinerbapabumDocumento15 páginasBS Simon MinerbapabumDadanAún no hay calificaciones

- Nuclear Power in India - Future & Emergence As Leading Global PlayerDocumento24 páginasNuclear Power in India - Future & Emergence As Leading Global PlayerSandip KarmakarAún no hay calificaciones

- Engy Scenario 15 16Documento25 páginasEngy Scenario 15 16Hydrosys InnovationAún no hay calificaciones

- Energy Crisis of Pakistan Causes & RemedyDocumento16 páginasEnergy Crisis of Pakistan Causes & Remedyamirq4Aún no hay calificaciones

- Presentation To Institutional Investors On Non-Deal Roadshow at USA 01042017Documento14 páginasPresentation To Institutional Investors On Non-Deal Roadshow at USA 01042017Yadav JiAún no hay calificaciones

- Power Sector Overview 2023Documento24 páginasPower Sector Overview 2023Rakesh MahtaAún no hay calificaciones

- (E4) IndonesiaDocumento36 páginas(E4) IndonesiaKarlinaAún no hay calificaciones

- Dirty Business: A Greenpeace Philippines Briefing PaperDocumento32 páginasDirty Business: A Greenpeace Philippines Briefing PaperKaykay MoleAún no hay calificaciones

- Dirty Business: A Greenpeace Philippines Briefing PaperDocumento32 páginasDirty Business: A Greenpeace Philippines Briefing PaperKaykay MoleAún no hay calificaciones

- SWITCH-Asia EE MEPS Labeling in Indonesia MR HarrisDocumento19 páginasSWITCH-Asia EE MEPS Labeling in Indonesia MR HarrisMuhammad Anjas Abdul KholikAún no hay calificaciones

- Turkey Oil Gas and Energy DemandDocumento16 páginasTurkey Oil Gas and Energy DemandElman AskerovAún no hay calificaciones

- MLT Out Look 2023 EditionDocumento46 páginasMLT Out Look 2023 EditionhambaliAún no hay calificaciones

- Saad PDF ReportDocumento13 páginasSaad PDF ReportAkbar RizviAún no hay calificaciones

- Energy Outlookin PakistanDocumento6 páginasEnergy Outlookin PakistanUmar SubzwariAún no hay calificaciones

- IndonesiaDocumento14 páginasIndonesiaeksarettaniaAún no hay calificaciones

- Roadmap Biodiesel IndonesiaDocumento22 páginasRoadmap Biodiesel IndonesiaSyartina SAún no hay calificaciones

- Article On Renewable EnergyDocumento14 páginasArticle On Renewable EnergyPoonam YadavAún no hay calificaciones

- TTTTTTDocumento15 páginasTTTTTTAjakqAún no hay calificaciones

- Coal India Limited: Corporate PresentationDocumento14 páginasCoal India Limited: Corporate PresentationPraveen KumarAún no hay calificaciones

- ETM forASEANwebinarDocumento14 páginasETM forASEANwebinarTiara SyAún no hay calificaciones

- Power Sector OverviewDocumento9 páginasPower Sector OverviewMuneer AhmedAún no hay calificaciones

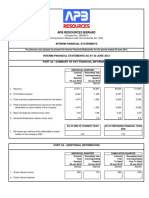

- Apb Resources Berhad: Interim Financial StatementsDocumento5 páginasApb Resources Berhad: Interim Financial StatementsDeep Kisor Datta-RayAún no hay calificaciones

- Elaborate Argument Elusive Premise A Rev PDFDocumento9 páginasElaborate Argument Elusive Premise A Rev PDFDeep Kisor Datta-RayAún no hay calificaciones

- Inp626680 PDFDocumento1 páginaInp626680 PDFDeep Kisor Datta-RayAún no hay calificaciones

- Sly CivilityDocumento11 páginasSly CivilityDeep Kisor Datta-RayAún no hay calificaciones

- Life and Words: Violence and The Descent Into The Ordinary (Veena Das)Documento5 páginasLife and Words: Violence and The Descent Into The Ordinary (Veena Das)Deep Kisor Datta-RayAún no hay calificaciones

- Intellectual India: Reason, Identity, Dissent: Jonardon GaneriDocumento18 páginasIntellectual India: Reason, Identity, Dissent: Jonardon GaneriDeep Kisor Datta-RayAún no hay calificaciones

- Srinath Raghavan "War and Peace in Modern India" ReviewDocumento3 páginasSrinath Raghavan "War and Peace in Modern India" ReviewDeep Kisor Datta-RayAún no hay calificaciones

- WInd Solar HybridDocumento3 páginasWInd Solar HybridFahdAún no hay calificaciones

- Design and Analysis of Inline Pipe Turbine: April 2020Documento12 páginasDesign and Analysis of Inline Pipe Turbine: April 2020ЖивотаЛазаревићAún no hay calificaciones

- Photovoltaic Standards ReferenceDocumento2 páginasPhotovoltaic Standards ReferenceChandra Salim100% (2)

- 20 MW Solar Plant ProposalDocumento8 páginas20 MW Solar Plant ProposalAbraham Sidagam80% (15)

- BEAM EV ARC 2020 Info Sheet v1.1Documento2 páginasBEAM EV ARC 2020 Info Sheet v1.1ankhbayar batkhuuAún no hay calificaciones

- BluE-S 10KTDocumento2 páginasBluE-S 10KTBoonmi BoonprasertAún no hay calificaciones

- Solar Off Grid BFDDocumento6 páginasSolar Off Grid BFDharAún no hay calificaciones

- Innovation, Sustainability and Transition in The Oil and Gas SectorDocumento15 páginasInnovation, Sustainability and Transition in The Oil and Gas SectorEmmanuel AdeboyeAún no hay calificaciones

- Barkapower 2017 2018 Annual 8036634217 PDFDocumento136 páginasBarkapower 2017 2018 Annual 8036634217 PDFMohammad helal uddin ChowdhuryAún no hay calificaciones

- Biaxial Solar Tracking SystemDocumento18 páginasBiaxial Solar Tracking SystemNirmit MadaanAún no hay calificaciones

- 09 - C NaCl-ODC Electrolysis Technology - Business Cases NaCl-ODC - Wolfgang FriedlDocumento7 páginas09 - C NaCl-ODC Electrolysis Technology - Business Cases NaCl-ODC - Wolfgang FriedlAnburaj NatarajaAún no hay calificaciones

- Solar PV Panel: InstallationDocumento2 páginasSolar PV Panel: InstallationHOD MECH DEGREE-LITAún no hay calificaciones

- Co-Genration of Power: A Project Report ON " "Documento15 páginasCo-Genration of Power: A Project Report ON " "Zaroon KhanAún no hay calificaciones

- Solarbuzz - Module Pricing - 2012-06-19Documento2 páginasSolarbuzz - Module Pricing - 2012-06-19Varun JadAún no hay calificaciones

- Luzon - Indicative - 2021 - June - 01Documento4 páginasLuzon - Indicative - 2021 - June - 01asiancutieAún no hay calificaciones

- (Elearnica - Ir) - Ground-Source Heat Pumps Systems and ApplicationsDocumento28 páginas(Elearnica - Ir) - Ground-Source Heat Pumps Systems and ApplicationsSeyed0% (1)

- Meisongmao Industrial Co., LTD Profile PDFDocumento10 páginasMeisongmao Industrial Co., LTD Profile PDFMalina MaAún no hay calificaciones

- 15 KW New Pinak Infra Projects Ltd.Documento8 páginas15 KW New Pinak Infra Projects Ltd.pinak powerAún no hay calificaciones

- Industrial Visit Report To Solar Power PlantDocumento9 páginasIndustrial Visit Report To Solar Power PlantAbhiAún no hay calificaciones

- Air Pollution: Analysis On The Adequacy of Government ActionsDocumento3 páginasAir Pollution: Analysis On The Adequacy of Government ActionsDK DMAún no hay calificaciones

- 560wP Micro InverterDocumento1 página560wP Micro InverterEric ValenciaAún no hay calificaciones

- State of The Art and Outlook of Chinese Wind Power IndustryDocumento39 páginasState of The Art and Outlook of Chinese Wind Power Industrywangwen zhaoAún no hay calificaciones

- ScorecardDocumento1 páginaScorecardYves NkamgniaAún no hay calificaciones

- Ece Solar Mobile Charger ReportDocumento19 páginasEce Solar Mobile Charger Reportfolagtech50% (2)

- Not Everything That Is Faced Can Be ChangedDocumento1 páginaNot Everything That Is Faced Can Be ChangedJonas JonaitisAún no hay calificaciones

- Manjalpur-Sub DivisionDocumento4 páginasManjalpur-Sub DivisionKuldeep RupareliaAún no hay calificaciones

- Kogaion V1.09: Renewable Potential Estimation: LoadsDocumento10 páginasKogaion V1.09: Renewable Potential Estimation: LoadsDonosa Cosmin IonutAún no hay calificaciones

- Annual - Report - 2019 ClarksonsDocumento202 páginasAnnual - Report - 2019 ClarksonsFernando Igor AlvarezAún no hay calificaciones

- FDP-JNTUA - Online ScheduleDocumento2 páginasFDP-JNTUA - Online ScheduleDamodara ReddyAún no hay calificaciones

- Tabel Invertoare Conforme - 60Documento19 páginasTabel Invertoare Conforme - 60ioana_poppyAún no hay calificaciones