También podría gustarte

- Ma IiDocumento2 páginasMa IiPryaAún no hay calificaciones

- MA CVP SolutionDocumento11 páginasMA CVP SolutionAll in ONEAún no hay calificaciones

- Relevant CostsDocumento7 páginasRelevant CostsPalesaAún no hay calificaciones

- MIDocumento18 páginasMImy tràAún no hay calificaciones

- Break Even Point Fixed Cost/ Contribution Per UnitDocumento11 páginasBreak Even Point Fixed Cost/ Contribution Per UnitKushagra VarmaAún no hay calificaciones

- CVP Analysis Q.1-10Documento28 páginasCVP Analysis Q.1-10James WisleyAún no hay calificaciones

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 21Documento2 páginasAllocation and Apportionment and Job and Batch Costing Worked Example Question 21Roshan RamkhalawonAún no hay calificaciones

- Horizential AnalysisDocumento4 páginasHorizential AnalysisM.TalhaAún no hay calificaciones

- Solution To Compiled QuestionsDocumento7 páginasSolution To Compiled Questionslovia mensahAún no hay calificaciones

- Fixed Cost Vs Variable CostDocumento24 páginasFixed Cost Vs Variable Costsrk_soumyaAún no hay calificaciones

- Chapter 7, 8, 9: Answers Cost Accounting ACCT3395Documento11 páginasChapter 7, 8, 9: Answers Cost Accounting ACCT3395Quynhu Smiley Nguyen50% (10)

- Acc116 Assignment Ahmad Irfan Bin Zakaria 2020836308Documento7 páginasAcc116 Assignment Ahmad Irfan Bin Zakaria 2020836308Siti RuzanaAún no hay calificaciones

- 2m00154 S.y.b.com - Bms Sem Ivchoice Based 78512 Group A Finance Strategic Cost Management Q.p.code53273Documento5 páginas2m00154 S.y.b.com - Bms Sem Ivchoice Based 78512 Group A Finance Strategic Cost Management Q.p.code53273Navira MirajkarAún no hay calificaciones

- Management Accounting: Page 1 of 6Documento70 páginasManagement Accounting: Page 1 of 6Ahmed Raza MirAún no hay calificaciones

- Accounting calculations and journal entriesDocumento6 páginasAccounting calculations and journal entriesZatsumono YamamotoAún no hay calificaciones

- Question 8 PresentationDocumento11 páginasQuestion 8 PresentationJeremiah NcubeAún no hay calificaciones

- F2 Past Paper - Ans12-2001Documento9 páginasF2 Past Paper - Ans12-2001ArsalanACCAAún no hay calificaciones

- Cost Accounting SolutionsDocumento3 páginasCost Accounting Solutionsamitdesai1508Aún no hay calificaciones

- ROI CALCULATION - MBA MKT 1 - Shivam JadhavDocumento4 páginasROI CALCULATION - MBA MKT 1 - Shivam JadhavShivam JadhavAún no hay calificaciones

- Cost Accounting Assignment 2Documento4 páginasCost Accounting Assignment 2leeroy mekiAún no hay calificaciones

- Nur Qaseh SDN BHD Soci CorrectedDocumento5 páginasNur Qaseh SDN BHD Soci CorrectedSyza LinaAún no hay calificaciones

- unit 8 -BudgetingDocumento8 páginasunit 8 -Budgetingkevin75108Aún no hay calificaciones

- Set 19 3Documento6 páginasSet 19 3Caro Kan LopezAún no hay calificaciones

- Allocation and Apportionment and Job and Batch Costing Worked Example Question 5Documento2 páginasAllocation and Apportionment and Job and Batch Costing Worked Example Question 5Roshan RamkhalawonAún no hay calificaciones

- Uts Mbb3313Documento5 páginasUts Mbb3313havre accountsAún no hay calificaciones

- Past Papers2Documento46 páginasPast Papers2leylaAún no hay calificaciones

- Past Year 2019 Sem 2 Ans (ZW)Documento4 páginasPast Year 2019 Sem 2 Ans (ZW)zhaoweiAún no hay calificaciones

- Mock Marking SchemeDocumento5 páginasMock Marking SchemeEric BYIRINGIROAún no hay calificaciones

- Assignment File FMDocumento4 páginasAssignment File FMvineeth kumarAún no hay calificaciones

- خالد محمد محمد سالمDocumento11 páginasخالد محمد محمد سالمkhaledmhmad157Aún no hay calificaciones

- BTEC Higher National Diploma (HND) in Business: Guildhall CollegeDocumento15 páginasBTEC Higher National Diploma (HND) in Business: Guildhall CollegeNayeem SiddiqueAún no hay calificaciones

- FR AssDocumento10 páginasFR Asssimon mtAún no hay calificaciones

- Product Allocation and CostingDocumento5 páginasProduct Allocation and CostingTariq RahimAún no hay calificaciones

- Marking SchemeDocumento5 páginasMarking SchemeEric BYIRINGIROAún no hay calificaciones

- Ke Toan Quan Tri FinalDocumento13 páginasKe Toan Quan Tri Finalkhanhlinh.vuha02Aún no hay calificaciones

- Department Accounts - SolutionDocumento17 páginasDepartment Accounts - Solution203 596 Reuben RoyAún no hay calificaciones

- MAF551 - Exercise 1 - Answer Question 4 - Karrimost SDN BHD - Ridzuan Bin Saharun - 2017700141Documento3 páginasMAF551 - Exercise 1 - Answer Question 4 - Karrimost SDN BHD - Ridzuan Bin Saharun - 2017700141RIDZUAN SAHARUNAún no hay calificaciones

- MAS-03 WorksheetDocumento32 páginasMAS-03 WorksheetPaupauAún no hay calificaciones

- Cost Estimation & CVP Suggested SolutionDocumento15 páginasCost Estimation & CVP Suggested SolutionNguyên Văn NhậtAún no hay calificaciones

- 21st - OCTOBER - 2022-TODAY CLASS - DotDocumento23 páginas21st - OCTOBER - 2022-TODAY CLASS - DotPalesaAún no hay calificaciones

- Business Plan of Manufacturing Air PurifiersDocumento7 páginasBusiness Plan of Manufacturing Air PurifiersSakshi BaiwalAún no hay calificaciones

- Delta Project and Repco AnalysisDocumento9 páginasDelta Project and Repco AnalysisvarunjajooAún no hay calificaciones

- 84 1.05 54 B. Direct Labour 14 0.175 28 Add: Factory O/h 42 0.525 84 Units Produced 80 120Documento6 páginas84 1.05 54 B. Direct Labour 14 0.175 28 Add: Factory O/h 42 0.525 84 Units Produced 80 120Ashutosh PatidarAún no hay calificaciones

- UntitledDocumento3 páginasUntitledVatsal ChangoiwalaAún no hay calificaciones

- SG2 4Documento3 páginasSG2 4snfrcbkb88Aún no hay calificaciones

- Management Control: (Session 6) Variances IDocumento35 páginasManagement Control: (Session 6) Variances IjohnAún no hay calificaciones

- Assignment: Table of ContentDocumento9 páginasAssignment: Table of ContentAhsanur HossainAún no hay calificaciones

- Installment SalesDocumento13 páginasInstallment SalesMichael BongalontaAún no hay calificaciones

- ABC Company Is Considering The Replacement of Old Machine That Is 3 Three Years Old With A NewDocumento9 páginasABC Company Is Considering The Replacement of Old Machine That Is 3 Three Years Old With A Newrajaroma45Aún no hay calificaciones

- Profitability Analysis Questions - Answer To Class ExercisesDocumento3 páginasProfitability Analysis Questions - Answer To Class ExercisesAhmed MunawarAún no hay calificaciones

- 3 Departmental AccountsDocumento13 páginas3 Departmental AccountsJayesh VyasAún no hay calificaciones

- Chapter # 10Documento2 páginasChapter # 10kqandeelAún no hay calificaciones

- Overhead: Allocation & ApportionmentDocumento10 páginasOverhead: Allocation & ApportionmentbiarrahsiaAún no hay calificaciones

- A) Financial Analysis of Divisional Performance of GMPHS: ParticularsDocumento6 páginasA) Financial Analysis of Divisional Performance of GMPHS: ParticularsAtmiya BiscuitwalaAún no hay calificaciones

- Budgetary ControlDocumento14 páginasBudgetary ControlCool BuddyAún no hay calificaciones

- MA Chap 5Documento19 páginasMA Chap 5Lan Tran HoangAún no hay calificaciones

- Costing For Decision-Making: Cost Defined As Total ExpenseDocumento44 páginasCosting For Decision-Making: Cost Defined As Total ExpenseUttam Kr PatraAún no hay calificaciones

- Submitted By:: Qaisar Shahzad Submitted To: Dr. Haroon Hussain Sb. Roll NoDocumento8 páginasSubmitted By:: Qaisar Shahzad Submitted To: Dr. Haroon Hussain Sb. Roll NoFaaiz YousafAún no hay calificaciones

- Five-Year Cash Flow Analysis of Machinery ProjectDocumento47 páginasFive-Year Cash Flow Analysis of Machinery ProjectleylaAún no hay calificaciones

- Invitation to Bid for Goods, Works and Non-Consulting ServicesDocumento1 páginaInvitation to Bid for Goods, Works and Non-Consulting ServicesMuhammad Shakil JanAún no hay calificaciones

- General Knowledge MCQsDocumento92 páginasGeneral Knowledge MCQsZain-ul- Farid100% (5)

- Request For Expression of Interest (EOI) (For Consulting Services)Documento1 páginaRequest For Expression of Interest (EOI) (For Consulting Services)Zain-ul- FaridAún no hay calificaciones

- Request For Expression of Interest (EOI) (For Consulting Services)Documento1 páginaRequest For Expression of Interest (EOI) (For Consulting Services)Zain-ul- FaridAún no hay calificaciones

- Application Form PDFDocumento1 páginaApplication Form PDFZain-ul- FaridAún no hay calificaciones

- Economics MCQS Ebook Download PDFDocumento85 páginasEconomics MCQS Ebook Download PDFMudassarGillani100% (5)

- Public Finance MCQSDocumento17 páginasPublic Finance MCQSZain-ul- Farid100% (2)

- MDA extends application deadline for job opportunities, read noticeDocumento4 páginasMDA extends application deadline for job opportunities, read noticeIrshad Ali SolangiAún no hay calificaciones

- CreditsDocumento1 páginaCreditsZain-ul- FaridAún no hay calificaciones

- Economics MCQS Ebook Download PDFDocumento85 páginasEconomics MCQS Ebook Download PDFMudassarGillani100% (5)

- Public Finance MCQSDocumento17 páginasPublic Finance MCQSZain-ul- Farid100% (2)

- Application Form PDFDocumento1 páginaApplication Form PDFZain-ul- FaridAún no hay calificaciones

- 1001 Vocabulary and Spelling QuestionsDocumento160 páginas1001 Vocabulary and Spelling Questionssashi01092% (12)

- Competetive Maths PDFDocumento464 páginasCompetetive Maths PDFTom McGovern100% (1)

- Economics MCQS Ebook Download PDFDocumento85 páginasEconomics MCQS Ebook Download PDFMudassarGillani100% (5)

- Economics MCQS Ebook Download PDFDocumento85 páginasEconomics MCQS Ebook Download PDFMudassarGillani100% (5)

- Pre-Feasibility Study: Media Production HouseDocumento28 páginasPre-Feasibility Study: Media Production Housealia khanAún no hay calificaciones

- Economics MCQS Ebook Download PDFDocumento85 páginasEconomics MCQS Ebook Download PDFMudassarGillani100% (5)

- Harry's Fluxco production variancesDocumento2 páginasHarry's Fluxco production variancesZain-ul- FaridAún no hay calificaciones

- Assignment 4Documento1 páginaAssignment 4Zain-ul- FaridAún no hay calificaciones

- Chapter 12 - Tax Depreciation, Amortisation - Pre-Commencement Expenditure PDFDocumento24 páginasChapter 12 - Tax Depreciation, Amortisation - Pre-Commencement Expenditure PDFZain-ul- FaridAún no hay calificaciones

- 2nd Week Oct Current Affairs - Prep4examsDocumento39 páginas2nd Week Oct Current Affairs - Prep4examsZain-ul- FaridAún no hay calificaciones

- Practice Question - 1Documento2 páginasPractice Question - 1Zain-ul- FaridAún no hay calificaciones

- Flexible Budget Practice QuestionDocumento2 páginasFlexible Budget Practice QuestionZain-ul- FaridAún no hay calificaciones

- Oogle in Hina: "It's An Imperfect World, We Had To Make An Imperfect Choice."Documento8 páginasOogle in Hina: "It's An Imperfect World, We Had To Make An Imperfect Choice."Zain-ul- FaridAún no hay calificaciones

- Toyota Case AnalysisDocumento4 páginasToyota Case AnalysisZain-ul- FaridAún no hay calificaciones

- Chinese Management IIDocumento21 páginasChinese Management IIZain-ul- FaridAún no hay calificaciones

- Toyota Case AnalysisDocumento4 páginasToyota Case AnalysisZain-ul- FaridAún no hay calificaciones

- Store Sales 2011Documento70 páginasStore Sales 2011bangiebangieAún no hay calificaciones

- The Treasury High Quality Market (HQM) Corporate Bond Yield CurveDocumento11 páginasThe Treasury High Quality Market (HQM) Corporate Bond Yield CurveZain-ul- FaridAún no hay calificaciones

- Women and Small Business EntrepreneurshiDocumento16 páginasWomen and Small Business EntrepreneurshiBaneenAún no hay calificaciones

- PharmEasy PE LabsDocumento9 páginasPharmEasy PE LabsPragya SachdevaAún no hay calificaciones

- OROTAN™ 1124 Dispersant: Regional Product Availability DescriptionDocumento3 páginasOROTAN™ 1124 Dispersant: Regional Product Availability DescriptionNOAún no hay calificaciones

- ת"א 5976-05-20 XL אנרג'י נ' מוטי גרינוולדDocumento338 páginasת"א 5976-05-20 XL אנרג'י נ' מוטי גרינוולדAlice AbramovichAún no hay calificaciones

- Ensuring Quality in Distribution of Medicinal ProductsDocumento16 páginasEnsuring Quality in Distribution of Medicinal ProductsASHU PURIAún no hay calificaciones

- Entrepreneurship Training ManualDocumento35 páginasEntrepreneurship Training Manualelias abdumalikAún no hay calificaciones

- Chetan KumarDocumento3 páginasChetan KumarChetan SharmaAún no hay calificaciones

- ProjectReport VinayDocumento75 páginasProjectReport VinayAbhishek raiAún no hay calificaciones

- Assignment DMBA104 MBA 1 Set-1 and 2 Jan-Feb 2023Documento6 páginasAssignment DMBA104 MBA 1 Set-1 and 2 Jan-Feb 2023Nihar KambleAún no hay calificaciones

- Castrol: Initiatives To Increase Rural Footprint: Srijit Chatterjee (C-61) Ankit Gupta (G-06)Documento16 páginasCastrol: Initiatives To Increase Rural Footprint: Srijit Chatterjee (C-61) Ankit Gupta (G-06)Srijit Jon ChatterjeeAún no hay calificaciones

- Lego Essay MergeDocumento16 páginasLego Essay Mergeadewale abiodunAún no hay calificaciones

- 3 What Else Can I DoDocumento1 página3 What Else Can I DoEnrico Luis BalisalisaAún no hay calificaciones

- Unit-II Lesson 6: Feasibility Analysis-Preparation of Project ReportDocumento25 páginasUnit-II Lesson 6: Feasibility Analysis-Preparation of Project ReportprathyushaelisettyAún no hay calificaciones

- Project Synopsis: Scms Cochin School of BusinessDocumento2 páginasProject Synopsis: Scms Cochin School of BusinessUmang ZehenAún no hay calificaciones

- c4 - NonvideosDocumento45 páginasc4 - NonvideosThanh TuyềnAún no hay calificaciones

- RIN Detergent: To Position OR Reposition: Group 7Documento16 páginasRIN Detergent: To Position OR Reposition: Group 7Satyam SinghAún no hay calificaciones

- Meralco vs. Vera 67 Scra 352, G.R. No. L-29987Documento11 páginasMeralco vs. Vera 67 Scra 352, G.R. No. L-29987Clarinda MerleAún no hay calificaciones

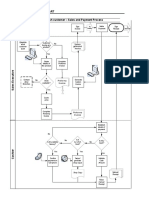

- As-Is-Flow Process Chart: No System Generated InvoiceDocumento10 páginasAs-Is-Flow Process Chart: No System Generated Invoicepeter mulilaAún no hay calificaciones

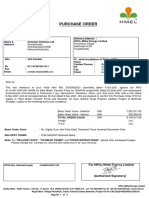

- Purchase Order for PumpsDocumento6 páginasPurchase Order for PumpsSuyog GawandeAún no hay calificaciones

- DRDDDDocumento12 páginasDRDDDWaqar HussainAún no hay calificaciones

- Organizational BehaviourDocumento6 páginasOrganizational BehaviourJudAún no hay calificaciones

- Packaging Industry ReportDocumento44 páginasPackaging Industry ReportKunalAún no hay calificaciones

- HSE Inspection Report-10Documento14 páginasHSE Inspection Report-10najihahAún no hay calificaciones

- 5 Little Known Profitable BusinessesDocumento34 páginas5 Little Known Profitable BusinessesFidelisAún no hay calificaciones

- Enterprise Resource Planning (ERP) : Presented By: Makansingh ChauhanDocumento28 páginasEnterprise Resource Planning (ERP) : Presented By: Makansingh ChauhanGuru Darshan0% (1)

- SME and SE ParagraphDocumento2 páginasSME and SE ParagraphAimee CuteAún no hay calificaciones

- Ipsas 23: Revenue From Non Exchange TransactionsDocumento11 páginasIpsas 23: Revenue From Non Exchange TransactionsHace AdisAún no hay calificaciones

- Effective Supervisory SkillsDocumento36 páginasEffective Supervisory SkillsAmosAún no hay calificaciones

- IJSDP MuafiandRatnaDocumento12 páginasIJSDP MuafiandRatnaWardani ArsyadAún no hay calificaciones

- Group 33 CRM Hubble Contact LensesDocumento6 páginasGroup 33 CRM Hubble Contact LensesSuman GoswamiAún no hay calificaciones