También podría gustarte

- Country Strategy 2011-2014 UkraineDocumento17 páginasCountry Strategy 2011-2014 UkraineBeeHoofAún no hay calificaciones

- Gvietnam eDocumento2 páginasGvietnam eTrang KieuAún no hay calificaciones

- Ukrainian Economy Anders As Lund 31008Documento42 páginasUkrainian Economy Anders As Lund 31008ankurbehlcoolAún no hay calificaciones

- Country Strategy 2011-2014 RussiaDocumento18 páginasCountry Strategy 2011-2014 RussiaBeeHoofAún no hay calificaciones

- Sweden A Macroeconomic OverviewDocumento16 páginasSweden A Macroeconomic OverviewVarun LohiaAún no hay calificaciones

- Economic Insight: Monthly Briefing From Icaew'S Economic Advisers MAY 2012Documento4 páginasEconomic Insight: Monthly Briefing From Icaew'S Economic Advisers MAY 2012api-125732404Aún no hay calificaciones

- June 28, 2011 July 13, 2011 June 28, 2011 June 28, 2011 January 29, 2001Documento70 páginasJune 28, 2011 July 13, 2011 June 28, 2011 June 28, 2011 January 29, 2001Ilya MozyrskiyAún no hay calificaciones

- Is Slovenia Next For An EU Bailout?Documento13 páginasIs Slovenia Next For An EU Bailout?Edward HughAún no hay calificaciones

- Key Issues For The Global Economy and Construction in 2011: Program, Cost, ConsultancyDocumento14 páginasKey Issues For The Global Economy and Construction in 2011: Program, Cost, ConsultancyUjjal RegmiAún no hay calificaciones

- Economic Update Nov201Documento12 páginasEconomic Update Nov201admin866Aún no hay calificaciones

- International Monetary Fund: Hina Conomic UtlookDocumento10 páginasInternational Monetary Fund: Hina Conomic UtlooktoobaziAún no hay calificaciones

- Macroeconomic Developments in Serbia: September 2014Documento20 páginasMacroeconomic Developments in Serbia: September 2014faca_zakonAún no hay calificaciones

- Country Strategy 2011-2014 MoldovaDocumento21 páginasCountry Strategy 2011-2014 MoldovaBeeHoofAún no hay calificaciones

- Greece Country Strategy Black Sea Bank's 2011-2014 Strategy for GreeceDocumento19 páginasGreece Country Strategy Black Sea Bank's 2011-2014 Strategy for GreeceBeeHoofAún no hay calificaciones

- UK Pound Exchange Rate AnalysisDocumento11 páginasUK Pound Exchange Rate AnalysisSiqi LIAún no hay calificaciones

- IIF Capital Flows Report 10 15Documento38 páginasIIF Capital Flows Report 10 15ed_nycAún no hay calificaciones

- Market Report 2011 OctoberDocumento18 páginasMarket Report 2011 OctoberAndra Elena AlexandrescuAún no hay calificaciones

- Republic of Moldova 2011Documento78 páginasRepublic of Moldova 2011Alexandra MelentiiAún no hay calificaciones

- Can Putinomics Survive 3Documento10 páginasCan Putinomics Survive 3AslanZeynalovAún no hay calificaciones

- Trade Growth To Ease in 2011 But Despite 2010 Record Surge, Crisis Hangover PersistsDocumento9 páginasTrade Growth To Ease in 2011 But Despite 2010 Record Surge, Crisis Hangover PersistsreneavaldezAún no hay calificaciones

- On The Development of The Russian Economy in 2011 and Forecast For 2012-2014Documento31 páginasOn The Development of The Russian Economy in 2011 and Forecast For 2012-2014ftorbergAún no hay calificaciones

- Country Strategy 2011-2014 ArmeniaDocumento16 páginasCountry Strategy 2011-2014 ArmeniaBeeHoofAún no hay calificaciones

- Unele Aspecte Ale Ajustarii Macroeconomice Din RomaniaDocumento32 páginasUnele Aspecte Ale Ajustarii Macroeconomice Din RomaniaIulia FlorescuAún no hay calificaciones

- Monthly: La Reforma Del Sector Servicios OUTLOOK 2012Documento76 páginasMonthly: La Reforma Del Sector Servicios OUTLOOK 2012Anonymous OY8hR2NAún no hay calificaciones

- EU Barroso PresDocumento117 páginasEU Barroso PresVlaki Lek VasdAún no hay calificaciones

- Channels Through Which The Effects of The Great Recession Were Transmitted or Propagated To The Developing and Least Developed CountriesDocumento5 páginasChannels Through Which The Effects of The Great Recession Were Transmitted or Propagated To The Developing and Least Developed CountriesMwawi MsukuAún no hay calificaciones

- The Balance of Payments - A Level EconomicsDocumento10 páginasThe Balance of Payments - A Level EconomicsjannerickAún no hay calificaciones

- The Economic Outlook For Germany May 8, 2010Documento16 páginasThe Economic Outlook For Germany May 8, 2010Ankit_modi2000Aún no hay calificaciones

- 4feb11 Retrospectiva2010 Scenarii2011 PDFDocumento16 páginas4feb11 Retrospectiva2010 Scenarii2011 PDFCalin PerpeleaAún no hay calificaciones

- Azerbaijan Country Strategy 2011-2014Documento15 páginasAzerbaijan Country Strategy 2011-2014BeeHoofAún no hay calificaciones

- Ifs Presentation CIA 3Documento21 páginasIfs Presentation CIA 3Ajay SinghAún no hay calificaciones

- Office Market: Marketview H1 2012Documento22 páginasOffice Market: Marketview H1 2012api-165123940Aún no hay calificaciones

- Eco Project UKDocumento16 páginasEco Project UKPankesh SethiAún no hay calificaciones

- Global Economic OutlookDocumento38 páginasGlobal Economic OutlookSami119Aún no hay calificaciones

- Development EconomicsDocumento16 páginasDevelopment EconomicsMehrin MorshedAún no hay calificaciones

- Country Strategy 2011-2014 TurkeyDocumento16 páginasCountry Strategy 2011-2014 TurkeyBeeHoofAún no hay calificaciones

- Erste Group ResearchDocumento18 páginasErste Group ResearchCatalin CroitoruAún no hay calificaciones

- Global CrisisDocumento28 páginasGlobal CrisisAli JumaniAún no hay calificaciones

- Quarterly Economic Update: June 2005Documento26 páginasQuarterly Economic Update: June 2005সামিউল ইসলাম রাজুAún no hay calificaciones

- Latin Manharlal Commodities Pvt. LTD.: Light at The EndDocumento25 páginasLatin Manharlal Commodities Pvt. LTD.: Light at The EndTushar PunjaniAún no hay calificaciones

- Economic Fact Book Greece: Key FactsDocumento8 páginasEconomic Fact Book Greece: Key Factslevel3assetsAún no hay calificaciones

- Macroeconomic Policy Tools for Ethiopia's Economic StabilityDocumento14 páginasMacroeconomic Policy Tools for Ethiopia's Economic Stabilitymuluken tewabeAún no hay calificaciones

- India Economic Update: September, 2011Documento17 páginasIndia Economic Update: September, 2011Rahul KaushikAún no hay calificaciones

- EN EN: European CommissionDocumento24 páginasEN EN: European Commissionapi-58353949Aún no hay calificaciones

- HSCB Mark Berrisford Smith PresentationDocumento42 páginasHSCB Mark Berrisford Smith PresentationMikeNigawhatupAún no hay calificaciones

- Table of Contents (40 Pages) : B G S - A H G R R Y S ?Documento12 páginasTable of Contents (40 Pages) : B G S - A H G R R Y S ?qwze9Aún no hay calificaciones

- UkraineDocumento2 páginasUkraineNgoc VoAún no hay calificaciones

- Highlights: Economy and Strategy GroupDocumento33 páginasHighlights: Economy and Strategy GroupvladvAún no hay calificaciones

- KH Econ Monitor Feb2011Documento22 páginasKH Econ Monitor Feb2011ChanthouHouyAún no hay calificaciones

- G R o U P o F T W e N T Y: M G - 2 0 D J 1 9 - 2 0, 2 0 1 2 M CDocumento20 páginasG R o U P o F T W e N T Y: M G - 2 0 D J 1 9 - 2 0, 2 0 1 2 M CLuke Campbell-SmithAún no hay calificaciones

- Analysis of Musharraf Era 1999-2008Documento37 páginasAnalysis of Musharraf Era 1999-2008Bushra NaumanAún no hay calificaciones

- Euro Crisis's Impact On IndiaDocumento49 páginasEuro Crisis's Impact On IndiaAncy ShajahanAún no hay calificaciones

- Venables YuehDocumento8 páginasVenables YuehMatthew BakerAún no hay calificaciones

- Balance of Payments Report: Central Bank of The Republic of TurkeyDocumento28 páginasBalance of Payments Report: Central Bank of The Republic of TurkeyKonna DiAún no hay calificaciones

- The Euro Crisis Is Sleeping, Not DeadDocumento1 páginaThe Euro Crisis Is Sleeping, Not DeadJayaKhemaniAún no hay calificaciones

- Vi. Price Situation: Global InflationDocumento15 páginasVi. Price Situation: Global InflationAnkur DubeyAún no hay calificaciones

- The Best Countries For LongDocumento13 páginasThe Best Countries For LongNam SanchunAún no hay calificaciones

- EIB Investment Report 2023/2024 - Key Findings: Transforming for competitivenessDe EverandEIB Investment Report 2023/2024 - Key Findings: Transforming for competitivenessAún no hay calificaciones

- Interim Report Q2 2017Documento56 páginasInterim Report Q2 2017Swedbank AB (publ)Aún no hay calificaciones

- Interim Report Q1 2017Documento54 páginasInterim Report Q1 2017Swedbank AB (publ)Aún no hay calificaciones

- Year-End Report 2016Documento51 páginasYear-End Report 2016Swedbank AB (publ)Aún no hay calificaciones

- PMI - February 2016Documento8 páginasPMI - February 2016Swedbank AB (publ)Aún no hay calificaciones

- Swedbank's Year-End Report 2015Documento58 páginasSwedbank's Year-End Report 2015Swedbank AB (publ)Aún no hay calificaciones

- Interim Report Q3 2016 Final ReportDocumento49 páginasInterim Report Q3 2016 Final ReportSwedbank AB (publ)Aún no hay calificaciones

- Full Interim Report Q2 2016Documento52 páginasFull Interim Report Q2 2016Swedbank AB (publ)Aún no hay calificaciones

- PMI Services - February 2016Documento8 páginasPMI Services - February 2016Swedbank AB (publ)Aún no hay calificaciones

- Swedbank Interim Report Q1 2016Documento55 páginasSwedbank Interim Report Q1 2016Swedbank AB (publ)Aún no hay calificaciones

- PMI Services March 2016Documento8 páginasPMI Services March 2016Swedbank AB (publ)Aún no hay calificaciones

- PMI - March 2016Documento8 páginasPMI - March 2016Swedbank AB (publ)Aún no hay calificaciones

- PMI Services January 2016Documento8 páginasPMI Services January 2016Swedbank AB (publ)Aún no hay calificaciones

- PMI Services - December 2015Documento8 páginasPMI Services - December 2015Swedbank AB (publ)Aún no hay calificaciones

- Swedbank Economic Outlook January 2016Documento35 páginasSwedbank Economic Outlook January 2016Swedbank AB (publ)Aún no hay calificaciones

- PMI January 2016Documento8 páginasPMI January 2016Swedbank AB (publ)Aún no hay calificaciones

- PMI-Services November 2015Documento8 páginasPMI-Services November 2015Swedbank AB (publ)Aún no hay calificaciones

- BrexitDocumento8 páginasBrexitSwedbank AB (publ)Aún no hay calificaciones

- Swedbank Economic Outlook January 2016Documento35 páginasSwedbank Economic Outlook January 2016Swedbank AB (publ)Aún no hay calificaciones

- Swedbank Economic Outlook Update, November 2015Documento17 páginasSwedbank Economic Outlook Update, November 2015Swedbank AB (publ)Aún no hay calificaciones

- PMI December 2015Documento8 páginasPMI December 2015Swedbank AB (publ)Aún no hay calificaciones

- Baltic Sea Report 2015Documento31 páginasBaltic Sea Report 2015Swedbank AB (publ)Aún no hay calificaciones

- PMI Services December 2015Documento9 páginasPMI Services December 2015Swedbank AB (publ)Aún no hay calificaciones

- PMI November 2015Documento8 páginasPMI November 2015Swedbank AB (publ)Aún no hay calificaciones

- PMI-Services November 2015Documento8 páginasPMI-Services November 2015Swedbank AB (publ)Aún no hay calificaciones

- ECB QE in The Baltics 2015-11-25Documento4 páginasECB QE in The Baltics 2015-11-25Swedbank AB (publ)Aún no hay calificaciones

- Swedbank Interim Report Third Quarter 2015Documento57 páginasSwedbank Interim Report Third Quarter 2015Swedbank AB (publ)Aún no hay calificaciones

- Wave of Refugees Propels GrowthDocumento8 páginasWave of Refugees Propels GrowthSwedbank AB (publ)Aún no hay calificaciones

- PMI-Services, September 2015Documento8 páginasPMI-Services, September 2015Swedbank AB (publ)Aún no hay calificaciones

- PMI October 2015Documento8 páginasPMI October 2015Swedbank AB (publ)Aún no hay calificaciones

- PMI September 2015Documento8 páginasPMI September 2015Swedbank AB (publ)Aún no hay calificaciones

- Finmar Invty Cash Receivables Management PDFDocumento18 páginasFinmar Invty Cash Receivables Management PDFJoshua CabinasAún no hay calificaciones

- ProQuestDocuments 2013 11 11Documento163 páginasProQuestDocuments 2013 11 11Parul AggarwalAún no hay calificaciones

- Saudi EconomicDocumento70 páginasSaudi EconomicFrancis Salviejo100% (1)

- Farm Laws: Confl Ating Deregulation With ModernisationDocumento6 páginasFarm Laws: Confl Ating Deregulation With ModernisationRASHMI RASHMIAún no hay calificaciones

- The Stony Brook Press - Volume 11, Issue 8Documento16 páginasThe Stony Brook Press - Volume 11, Issue 8The Stony Brook PressAún no hay calificaciones

- 2.1 How Can Inflation Be Good For You - BBC NewsDocumento1 página2.1 How Can Inflation Be Good For You - BBC NewsAbhinav UppalAún no hay calificaciones

- 105 Mag Economic SurveyDocumento331 páginas105 Mag Economic SurveyManoj KumarAún no hay calificaciones

- Chapter 6 Mankiw (Macroeconomics)Documento36 páginasChapter 6 Mankiw (Macroeconomics)andrew myintmyat100% (1)

- AppendicesDocumento13 páginasAppendicesapi-20017434Aún no hay calificaciones

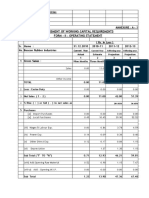

- Assessment of Working Capital Requirements Form - Ii: Operating StatementDocumento17 páginasAssessment of Working Capital Requirements Form - Ii: Operating StatementAshok TiwaryAún no hay calificaciones

- Student Paper One Ib EconomicsDocumento7 páginasStudent Paper One Ib Economicsilgyu1207Aún no hay calificaciones

- League of Women Voter GuideDocumento24 páginasLeague of Women Voter GuideReporterJennaAún no hay calificaciones

- Review Article Piketty RevDocumento18 páginasReview Article Piketty RevCreomar BaptistaAún no hay calificaciones

- Chapter 1 - Structure of Financial SystemDocumento18 páginasChapter 1 - Structure of Financial SystemNur HazirahAún no hay calificaciones

- Fundamental Analysis Sun PharmaDocumento5 páginasFundamental Analysis Sun PharmadeveshAún no hay calificaciones

- KSE100 down 4.6% in December amid political turmoilDocumento24 páginasKSE100 down 4.6% in December amid political turmoilMUHAMMAD QASIMAún no hay calificaciones

- Chapter 11 - Public Finance-1Documento7 páginasChapter 11 - Public Finance-1Gulshan Academy High School JamshoroAún no hay calificaciones

- Macro Economics Project Report - Group 7.Documento30 páginasMacro Economics Project Report - Group 7.Mayank Misra50% (2)

- Erj 2 BTDocumento43 páginasErj 2 BTlimtekkaunAún no hay calificaciones

- Competitiveness and Private Sector Development-Egypt 2010-2510041eDocumento144 páginasCompetitiveness and Private Sector Development-Egypt 2010-2510041eMohamed AboudAún no hay calificaciones

- 7 CMA FormatDocumento22 páginas7 CMA Formatzahoor80100% (2)

- 2021 RVHS H1 Prelim CSQ - Suggested Answers For SharingDocumento18 páginas2021 RVHS H1 Prelim CSQ - Suggested Answers For SharingAmelia WongAún no hay calificaciones

- MCQ's On EconomicsDocumento43 páginasMCQ's On Economicsआई सी एस इंस्टीट्यूटAún no hay calificaciones

- Reinventing Government for Greater EfficiencyDocumento9 páginasReinventing Government for Greater Efficiencygugoloth shankarAún no hay calificaciones

- 2023 Ghana Budget Highlights and Key Sector Growth ProjectionsDocumento37 páginas2023 Ghana Budget Highlights and Key Sector Growth ProjectionsdmensahAún no hay calificaciones

- Investment Office ANRS: Project Profile On The HONEY Processing PlantDocumento24 páginasInvestment Office ANRS: Project Profile On The HONEY Processing PlantJohn100% (1)

- Budget Law SonDocumento16 páginasBudget Law SonObrabotka FotografiyAún no hay calificaciones

- LIC Assistant Mains GA Power Capsule 2019 PDFDocumento104 páginasLIC Assistant Mains GA Power Capsule 2019 PDFAbhilash GanjarapalliAún no hay calificaciones

- Security Analysis and Portfolio Management Mba Project ReportDocumento75 páginasSecurity Analysis and Portfolio Management Mba Project ReportJyostna Kollamgunta70% (10)

- Fiscal policy implications for budgeting and taxationDocumento20 páginasFiscal policy implications for budgeting and taxationHIMANSHI HIMANSHIAún no hay calificaciones