También podría gustarte

- PAS 34 Interim Financial Reporting: Learning ObjectivesDocumento5 páginasPAS 34 Interim Financial Reporting: Learning ObjectivesFhrince Carl CalaquianAún no hay calificaciones

- IAS 34 Interim Financial ReportingDocumento4 páginasIAS 34 Interim Financial Reportingmusic niAún no hay calificaciones

- IAS34:Interim Financial ReportingDocumento37 páginasIAS34:Interim Financial ReportingTanvir HossainAún no hay calificaciones

- Ac510wk14Documento64 páginasAc510wk14Niño Mendoza Mabato100% (2)

- Accounting Periods and Methods and Other Compliance RequirementsDocumento5 páginasAccounting Periods and Methods and Other Compliance RequirementsTurks50% (2)

- AMLC, VAT, Interim Segment ReportingDocumento27 páginasAMLC, VAT, Interim Segment ReportingChes THGAún no hay calificaciones

- Interim Financial ReportingDocumento17 páginasInterim Financial ReportingAlexa LeeAún no hay calificaciones

- Interim Financial ReportingDocumento4 páginasInterim Financial ReportingMia CruzAún no hay calificaciones

- CHAPTER 12 - Interim Financial ReportingDocumento47 páginasCHAPTER 12 - Interim Financial ReportingChristian Gatchalian100% (1)

- Topic 2 Interim Financial ReportingDocumento78 páginasTopic 2 Interim Financial ReportingAaron MañacapAún no hay calificaciones

- Chapter 19 Interim ReportingDocumento6 páginasChapter 19 Interim ReportingEllen MaskariñoAún no hay calificaciones

- As 25Documento6 páginasAs 25abhishekkapse654Aún no hay calificaciones

- What Is Annualized Withholding TaxDocumento7 páginasWhat Is Annualized Withholding TaxMarietta Fragata RamiterreAún no hay calificaciones

- Financial Oversight and Management Board For Puerto Rico's Annex A To FIscal Year 2017 ReportDocumento5 páginasFinancial Oversight and Management Board For Puerto Rico's Annex A To FIscal Year 2017 ReportLatino USAAún no hay calificaciones

- Pas 34 Interim Financial Reporting Group 15Documento56 páginasPas 34 Interim Financial Reporting Group 15Faker MejiaAún no hay calificaciones

- Cfab - Acc - LN - Chapter 9Documento9 páginasCfab - Acc - LN - Chapter 9Huy NguyenAún no hay calificaciones

- Chapter 8 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Documento47 páginasChapter 8 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarAún no hay calificaciones

- Tax Treatement in Cash Flow StatementDocumento4 páginasTax Treatement in Cash Flow StatementtilokiAún no hay calificaciones

- Summary Cash Flow - Taxation Paid, Dividends Paid and Interest PaidDocumento8 páginasSummary Cash Flow - Taxation Paid, Dividends Paid and Interest PaidLesego BaneleAún no hay calificaciones

- Income StatementDocumento14 páginasIncome StatementDELFIN, LORENA D.Aún no hay calificaciones

- Provisional Tax - SlidesDocumento17 páginasProvisional Tax - SlidesZwivhuya MaimelaAún no hay calificaciones

- Journal Entries: Example 1: Whole-Period Depreciation in The Period of PurchaseDocumento2 páginasJournal Entries: Example 1: Whole-Period Depreciation in The Period of PurchasemulualemAún no hay calificaciones

- ÔN CUỐI KỲ CHUẨN MỰC BCTCQT 2Documento8 páginasÔN CUỐI KỲ CHUẨN MỰC BCTCQT 2trantram130903Aún no hay calificaciones

- Equity StatementDocumento10 páginasEquity StatementMUKHAMMAD CHOIRUL ANAMXII AKL 20Aún no hay calificaciones

- Interim Financial ReportingDocumento3 páginasInterim Financial ReportingBernie Mojico CaronanAún no hay calificaciones

- Practical Application of Taxation On CorporationsDocumento5 páginasPractical Application of Taxation On CorporationsClaire BarbaAún no hay calificaciones

- Chapter 6 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Documento71 páginasChapter 6 - Gripping IFRS ICAP 2008 (Solution of Graded Questions)Falah Ud Din SheryarAún no hay calificaciones

- Philadelphia Quarterly City Manager's ReportDocumento80 páginasPhiladelphia Quarterly City Manager's ReportPhillyVoice.comAún no hay calificaciones

- Hand Outs - Statement of Comprehensive IncomeDocumento1 páginaHand Outs - Statement of Comprehensive IncomeElizah SimanganAún no hay calificaciones

- Comfort LetterDocumento5 páginasComfort LetterZ_JahangeerAún no hay calificaciones

- BIR 1702Q FormDocumento3 páginasBIR 1702Q FormyellahfellahAún no hay calificaciones

- Interim Financial ReportingDocumento6 páginasInterim Financial ReportingKimberly AsuncionAún no hay calificaciones

- Interim Financial ReportingDocumento9 páginasInterim Financial ReportingNelly GomezAún no hay calificaciones

- P&L Vs OCIDocumento2 páginasP&L Vs OCIRujean Salar AltejarAún no hay calificaciones

- IFRS Chapter 10 The Consolidated Income StatementDocumento34 páginasIFRS Chapter 10 The Consolidated Income StatementJuBin DeliwalaAún no hay calificaciones

- 1702 NewDocumento11 páginas1702 NewDIVINE WAGTINGANAún no hay calificaciones

- Toa ReportingDocumento36 páginasToa ReportingMakoy BixenmanAún no hay calificaciones

- Interim Financial ReportingDocumento20 páginasInterim Financial ReportingToni Rose Hernandez LualhatiAún no hay calificaciones

- Chapter 21 IAS 1Documento4 páginasChapter 21 IAS 1Chandan SamalAún no hay calificaciones

- Wa0000 PDFDocumento12 páginasWa0000 PDFsipheleleAún no hay calificaciones

- 5695 - Partnership Account SS2 NoteDocumento11 páginas5695 - Partnership Account SS2 NoteAmarachi ObingeneAún no hay calificaciones

- How To Compute and Prepare The Quarterly Income Tax ReturnsDocumento4 páginasHow To Compute and Prepare The Quarterly Income Tax ReturnsTwoo Phil100% (5)

- Income StatementDocumento21 páginasIncome StatementKoo TaehyungAún no hay calificaciones

- Liability: What Is A Liability?Documento5 páginasLiability: What Is A Liability?Hikmət RüstəmovAún no hay calificaciones

- Interim Financial Reporting: Click To Edit Master Subtitle StyleDocumento64 páginasInterim Financial Reporting: Click To Edit Master Subtitle StyleShr BnAún no hay calificaciones

- 6 Interim ReportingDocumento3 páginas6 Interim ReportingBrian VillaluzAún no hay calificaciones

- Notes To Financial StatementsDocumento9 páginasNotes To Financial StatementsCheryl FuentesAún no hay calificaciones

- Statement of Changes in Equity ReviewerDocumento3 páginasStatement of Changes in Equity ReviewerSean Arvy SamsonAún no hay calificaciones

- 2012 Marion, Indiana Tax LevyDocumento12 páginas2012 Marion, Indiana Tax LevyMarionIndiana.netAún no hay calificaciones

- C12 - Interim Financial ReportingDocumento65 páginasC12 - Interim Financial ReportingKlare JimenoAún no hay calificaciones

- Example of A Comfort LetterDocumento5 páginasExample of A Comfort LetterAndrew Grimes0% (1)

- 2020 08a Presentation FS PPDocumento21 páginas2020 08a Presentation FS PPAngel TomAún no hay calificaciones

- Topic 2 MFRS134 Interim ReportingDocumento28 páginasTopic 2 MFRS134 Interim ReportingelinaAún no hay calificaciones

- FR17 - Employee Benefits (PracticeQns)Documento11 páginasFR17 - Employee Benefits (PracticeQns)duong duongAún no hay calificaciones

- Client Assistance ScheduleDocumento9 páginasClient Assistance SchedulesefanitAún no hay calificaciones

- Trimester 1, 2023 HI5020Documento5 páginasTrimester 1, 2023 HI5020aminbayevbAún no hay calificaciones

- Wiley GAAP for Governments 2017: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsDe EverandWiley GAAP for Governments 2017: Interpretation and Application of Generally Accepted Accounting Principles for State and Local GovernmentsAún no hay calificaciones

- Verify Udyam Registration DetailDocumento3 páginasVerify Udyam Registration DetailFinance HubAún no hay calificaciones

- Project Introduction: Instructor: Prof. Sanjeev Tripathi Academic Associate: Ms. Sonal GogriDocumento8 páginasProject Introduction: Instructor: Prof. Sanjeev Tripathi Academic Associate: Ms. Sonal GogriGarimaAún no hay calificaciones

- A Case Study On RIL vs. RNRL DisputeDocumento6 páginasA Case Study On RIL vs. RNRL DisputeAparajita SharmaAún no hay calificaciones

- SAI Employee Retention For HandoutsDocumento16 páginasSAI Employee Retention For Handoutsshindy100% (1)

- Answers HW17Documento3 páginasAnswers HW17summanahAún no hay calificaciones

- Latha Data Analyst Resume..Documento3 páginasLatha Data Analyst Resume..KIRAN KIRANAún no hay calificaciones

- Statement IbblDocumento1 páginaStatement Ibblmamunkhan1216jAún no hay calificaciones

- Tourism Market ResearchDocumento14 páginasTourism Market ResearchLoping Lee100% (1)

- A Project Report ON "Customer Satisfaction in Nokia": Bachelor of Business Administration (Banking & Insurance)Documento39 páginasA Project Report ON "Customer Satisfaction in Nokia": Bachelor of Business Administration (Banking & Insurance)Navneet TyagiAún no hay calificaciones

- PEL PakistanDocumento27 páginasPEL Pakistanjutt707100% (1)

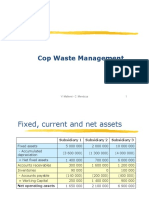

- Cop Waste Management SolutionDocumento5 páginasCop Waste Management SolutionPaul GhanimehAún no hay calificaciones

- Summary BMKT 525 Marketing ManagementDocumento112 páginasSummary BMKT 525 Marketing ManagementSobhi BraidyAún no hay calificaciones

- Trade Secrets PPT (By Aditya)Documento19 páginasTrade Secrets PPT (By Aditya)Aditya AgrawalAún no hay calificaciones

- Entrepreneurship and Economic DevelopmentDocumento44 páginasEntrepreneurship and Economic Developmentgosaye desalegn100% (1)

- Audit Internship Report Nida DKDocumento28 páginasAudit Internship Report Nida DKShan Ali ShahAún no hay calificaciones

- NALCO Recruitment 2022 Notification PDFDocumento12 páginasNALCO Recruitment 2022 Notification PDFRATHIRAM NAIKAún no hay calificaciones

- Road Safety Risk Assessment ToolkitDocumento4 páginasRoad Safety Risk Assessment ToolkitTony RandersonAún no hay calificaciones

- Rajaram Exam Fees P16mba7Documento2 páginasRajaram Exam Fees P16mba7Encom VeluAún no hay calificaciones

- Budget Circular No 2018 4 PDFDocumento245 páginasBudget Circular No 2018 4 PDFJoey Villas MaputiAún no hay calificaciones

- Project ProposalDocumento5 páginasProject ProposalJornie Duallo100% (1)

- Weirich7e Casesolutions-3Documento37 páginasWeirich7e Casesolutions-3Connor Day50% (4)

- Review 105 - Day 1 Theory of AccountsDocumento13 páginasReview 105 - Day 1 Theory of AccountsMarites ArcenaAún no hay calificaciones

- Week 5 AssignmentDocumento1 páginaWeek 5 AssignmentSushmita Shivaram100% (1)

- HR E1 - Project ManagementDocumento2 páginasHR E1 - Project ManagementAlelei BungalanAún no hay calificaciones

- ch1 12e TB Chapter1 12th Edition of Business Ethics Test BankDocumento27 páginasch1 12e TB Chapter1 12th Edition of Business Ethics Test BankKhánh Linh LêAún no hay calificaciones

- Csec Poa Handout 1Documento28 páginasCsec Poa Handout 1Taariq Abdul-Majeed100% (2)

- How To Succeed at Retail - Winning Case Studies and Strategies For Retailers and Brands PDFDocumento224 páginasHow To Succeed at Retail - Winning Case Studies and Strategies For Retailers and Brands PDFPrashant SinghAún no hay calificaciones

- Gujarati EntrepreneursDocumento7 páginasGujarati EntrepreneursPayal ChhabraAún no hay calificaciones

- Rate Rebasing Concepts For Public Consultation, MWSSDocumento13 páginasRate Rebasing Concepts For Public Consultation, MWSSImperator FuriosaAún no hay calificaciones

- Module 3 - Social Responsibility and Ethics in ManagementDocumento18 páginasModule 3 - Social Responsibility and Ethics in ManagementAaron Christopher SungaAún no hay calificaciones