También podría gustarte

- An Incredibly Funny and Well-Crafted Piece of Legal WritingDocumento35 páginasAn Incredibly Funny and Well-Crafted Piece of Legal WritingJohn P Capitalist100% (4)

- CCA Conduct Rule 1965 MCQDocumento56 páginasCCA Conduct Rule 1965 MCQANURAG SINGH100% (7)

- In The United States Court of Appeals For The Ninth Circuit: Attorneys For Petitioner-Appellee Nouvel, LLCDocumento28 páginasIn The United States Court of Appeals For The Ninth Circuit: Attorneys For Petitioner-Appellee Nouvel, LLCHollyRustonAún no hay calificaciones

- Petition For A Writ of Certiorari, Pacetta v. Town of Ponce Inlet, No. 17-1698 (June 21, 2018)Documento52 páginasPetition For A Writ of Certiorari, Pacetta v. Town of Ponce Inlet, No. 17-1698 (June 21, 2018)RHTAún no hay calificaciones

- Brief in Opposition in Retirement Capital Access MGMT v. U.S. BancorpDocumento38 páginasBrief in Opposition in Retirement Capital Access MGMT v. U.S. BancorpMatthew DowdAún no hay calificaciones

- 19-08-30 Int'l Center For Law & Economics AcbDocumento48 páginas19-08-30 Int'l Center For Law & Economics AcbFlorian MuellerAún no hay calificaciones

- 19-08-30 Hon. Paul R. Michel AcbDocumento42 páginas19-08-30 Hon. Paul R. Michel AcbFlorian MuellerAún no hay calificaciones

- Malaney v. UALDocumento35 páginasMalaney v. UALNorthern District of California BlogAún no hay calificaciones

- Supreme Court of The United States: PetitionerDocumento38 páginasSupreme Court of The United States: PetitionerKumarAún no hay calificaciones

- 20-03-20 Statement of Interest by DOJ ATRDocumento27 páginas20-03-20 Statement of Interest by DOJ ATRFlorian MuellerAún no hay calificaciones

- 19-08-30 Antitrust and Patent Law Profs AcbDocumento47 páginas19-08-30 Antitrust and Patent Law Profs AcbFlorian MuellerAún no hay calificaciones

- Plaintiffs-Appellees,: RAL Rgument Cheduled OR EcemberDocumento37 páginasPlaintiffs-Appellees,: RAL Rgument Cheduled OR EcemberKathleen PerrinAún no hay calificaciones

- Case No. 09-16959 in The United States Court of Appeals For The Ninth CircuitDocumento37 páginasCase No. 09-16959 in The United States Court of Appeals For The Ninth CircuitEquality Case FilesAún no hay calificaciones

- Amicus Brief Unwired v. Google 02.06.2017 (15-1812)Documento18 páginasAmicus Brief Unwired v. Google 02.06.2017 (15-1812)Jon StroudAún no hay calificaciones

- 22-01-27 Microsoft Acb Iso Epic Games Against AppleDocumento38 páginas22-01-27 Microsoft Acb Iso Epic Games Against AppleFlorian MuellerAún no hay calificaciones

- Memorandum of Points and Authorities in Support of Its Motion For Partial Summary Judgment Dismissing All Claims Against JPMCDocumento48 páginasMemorandum of Points and Authorities in Support of Its Motion For Partial Summary Judgment Dismissing All Claims Against JPMCmeischerAún no hay calificaciones

- Amicus Brief Filed by Massachusetts Attorney General Maura Healey and 13 Other AGs in Class Action Suit Against Remington ArmsDocumento34 páginasAmicus Brief Filed by Massachusetts Attorney General Maura Healey and 13 Other AGs in Class Action Suit Against Remington ArmsPatrick JohnsonAún no hay calificaciones

- United States Court of Appeals: Amicus CuriaeDocumento32 páginasUnited States Court of Appeals: Amicus CuriaeKathleen PerrinAún no hay calificaciones

- Williams V Gaye Petition For Rehearing en BancDocumento22 páginasWilliams V Gaye Petition For Rehearing en BancTHROnlineAún no hay calificaciones

- Kickstarter SJDocumento43 páginasKickstarter SJEriq GardnerAún no hay calificaciones

- Immigration Voice Brief in Save Jobs H4EAD LawsuitDocumento54 páginasImmigration Voice Brief in Save Jobs H4EAD LawsuitBreitbart NewsAún no hay calificaciones

- Answering Brief of Appellees Barclays Bank PLC and Barclays Capital Real Estate Inc. D/B/A Homeq ServicingDocumento31 páginasAnswering Brief of Appellees Barclays Bank PLC and Barclays Capital Real Estate Inc. D/B/A Homeq Servicing83jjmackAún no hay calificaciones

- Economists AmicusDocumento21 páginasEconomists AmicuseriqgardnerAún no hay calificaciones

- Opposition To Motion For Preliminary InjunctionDocumento49 páginasOpposition To Motion For Preliminary InjunctionBasseemAún no hay calificaciones

- United States District Court Central District of CaliforniaDocumento21 páginasUnited States District Court Central District of Californiaeriq_gardner6833Aún no hay calificaciones

- 20-09-25 FTC Petition For Ninth Circuit Rehearing in Qualcomm Antitrust CaseDocumento83 páginas20-09-25 FTC Petition For Ninth Circuit Rehearing in Qualcomm Antitrust CaseFlorian MuellerAún no hay calificaciones

- 19-11-29 AAI and Public Knowledge Acb PDFDocumento42 páginas19-11-29 AAI and Public Knowledge Acb PDFFlorian MuellerAún no hay calificaciones

- United States Court of Appeals For The Ninth Circuit: Plaintiffs/AppelleesDocumento43 páginasUnited States Court of Appeals For The Ninth Circuit: Plaintiffs/AppelleesKathleen PerrinAún no hay calificaciones

- 21-11-16 (9th Cir.) Apple Motion To Stay InjunctionDocumento33 páginas21-11-16 (9th Cir.) Apple Motion To Stay InjunctionFlorian MuellerAún no hay calificaciones

- Appeals - Federal - 3rd Circuit - Brief For Appellant - Cravath 2020Documento68 páginasAppeals - Federal - 3rd Circuit - Brief For Appellant - Cravath 2020John PowellAún no hay calificaciones

- 26respondentkiit PDFDocumento36 páginas26respondentkiit PDFChiranjeev RoutrayAún no hay calificaciones

- Pedreira Opening BRDocumento59 páginasPedreira Opening BRHilary LedwellAún no hay calificaciones

- Amicus Brief of 16 BusinessesDocumento28 páginasAmicus Brief of 16 BusinessesLaw&CrimeAún no hay calificaciones

- Law Prof Metlife Brief 6.23.2016Documento45 páginasLaw Prof Metlife Brief 6.23.2016Chris WalkerAún no hay calificaciones

- ResponseDocumento18 páginasResponseDebtwire MunicipalsAún no hay calificaciones

- 2019-12-23 - 7 - 19-cv-07660 - No. 54 Appellant's REPLY BRIEF (S.D.N.Y.)Documento52 páginas2019-12-23 - 7 - 19-cv-07660 - No. 54 Appellant's REPLY BRIEF (S.D.N.Y.)Lyndell MooreAún no hay calificaciones

- MOTION For Preliminary Injunction With Incorporated Memorandum of Law in Support by Christopher DoyleDocumento41 páginasMOTION For Preliminary Injunction With Incorporated Memorandum of Law in Support by Christopher DoyleLindsey KaleyAún no hay calificaciones

- Paxton's Florida Amicus BriefDocumento39 páginasPaxton's Florida Amicus BriefRob LauciusAún no hay calificaciones

- Ief in Support of Motion For Status Quo Order - Crusader V HighlandDocumento31 páginasIef in Support of Motion For Status Quo Order - Crusader V HighlandSeth BrumbyAún no hay calificaciones

- Docket #8811 Date Filed: 10/14/2011Documento37 páginasDocket #8811 Date Filed: 10/14/2011meischerAún no hay calificaciones

- WBO Opposition BriefDocumento36 páginasWBO Opposition BriefMMA PayoutAún no hay calificaciones

- Judd V Weinstein Cal Senate Amicus BriefDocumento26 páginasJudd V Weinstein Cal Senate Amicus BriefTHROnlineAún no hay calificaciones

- 19-11-26 Jorge Contreras AcbDocumento42 páginas19-11-26 Jorge Contreras AcbFlorian MuellerAún no hay calificaciones

- 19-11-27 Law & Econ Profs AcbDocumento46 páginas19-11-27 Law & Econ Profs AcbFlorian MuellerAún no hay calificaciones

- Response To Motion To DismissDocumento33 páginasResponse To Motion To DismissMMA PayoutAún no hay calificaciones

- In Re Apple - Unified Amicus BriefDocumento27 páginasIn Re Apple - Unified Amicus BriefJennifer M GallagherAún no hay calificaciones

- FBI v. Fazaga (Amicus Brief)Documento36 páginasFBI v. Fazaga (Amicus Brief)The Brennan Center for JusticeAún no hay calificaciones

- Motion For Preliminary Injunction, Hobby Lobby v. Sebelius At, 5:12-cv-01000 (W.D.OK. Sept. 12, 2012) .Documento31 páginasMotion For Preliminary Injunction, Hobby Lobby v. Sebelius At, 5:12-cv-01000 (W.D.OK. Sept. 12, 2012) .joshblackmanAún no hay calificaciones

- Amicus Brief of Leading Companies and Business OrganizationsDocumento25 páginasAmicus Brief of Leading Companies and Business OrganizationsMike WuertheleAún no hay calificaciones

- 19-08-30 Dolby Labs AcbDocumento39 páginas19-08-30 Dolby Labs AcbFlorian MuellerAún no hay calificaciones

- Pedreira OppDocumento85 páginasPedreira OppHilary LedwellAún no hay calificaciones

- CU/CUF Amicus Brief - Louisiana v. Biden (Biden Climate Executive Order)Documento36 páginasCU/CUF Amicus Brief - Louisiana v. Biden (Biden Climate Executive Order)Citizens UnitedAún no hay calificaciones

- NELF Amicus Brief in West Virginia v. EPADocumento28 páginasNELF Amicus Brief in West Virginia v. EPAOakwheelAún no hay calificaciones

- EAppraiseIT Corelogic SettlementDocumento25 páginasEAppraiseIT Corelogic SettlementLori NobleAún no hay calificaciones

- Airbnb Opening Appellate BriefDocumento94 páginasAirbnb Opening Appellate BriefMarkAún no hay calificaciones

- 19-07-18 FTC Opposition To Qualcomm Motion To StayDocumento164 páginas19-07-18 FTC Opposition To Qualcomm Motion To StayFlorian MuellerAún no hay calificaciones

- For FilingDocumento24 páginasFor FilingKenneth SandersAún no hay calificaciones

- Midwest Fence Corp. v. U.S. Dept. of TransportationDocumento32 páginasMidwest Fence Corp. v. U.S. Dept. of TransportationCato InstituteAún no hay calificaciones

- Arbitration Law and Practice in KenyaDe EverandArbitration Law and Practice in KenyaCalificación: 2.5 de 5 estrellas2.5/5 (4)

- Remarkable Cities and the Fight Against Climate ChangeDe EverandRemarkable Cities and the Fight Against Climate ChangeAún no hay calificaciones

- El FMI Sobre La Inteligencia ArtificialDocumento42 páginasEl FMI Sobre La Inteligencia ArtificialCronista.comAún no hay calificaciones

- YPF 3Q23 Earnings Webcast PresentationDocumento9 páginasYPF 3Q23 Earnings Webcast PresentationCronista.comAún no hay calificaciones

- Berkshire Hathaway IncDocumento2 páginasBerkshire Hathaway IncZerohedgeAún no hay calificaciones

- FMI ArgentinaDocumento135 páginasFMI ArgentinaCronista.com100% (2)

- 2206 1Q Staff ReportDocumento105 páginas2206 1Q Staff ReportCronista.comAún no hay calificaciones

- Igj KMBDocumento21 páginasIgj KMBCronista.comAún no hay calificaciones

- World Happiness ReportDocumento158 páginasWorld Happiness ReportCronista.com100% (1)

- Documento Completo Del FMIDocumento111 páginasDocumento Completo Del FMILPOAún no hay calificaciones

- Fallo Expropiación YPFDocumento64 páginasFallo Expropiación YPFLPO100% (1)

- Carta MartinezDocumento4 páginasCarta MartinezbracamontiAún no hay calificaciones

- Vision Argentina FMIDocumento17 páginasVision Argentina FMICronista.comAún no hay calificaciones

- PR Russia ClassificationDocumento3 páginasPR Russia ClassificationBAE NegociosAún no hay calificaciones

- Paises Mas CarosjpgDocumento1 páginaPaises Mas CarosjpgCronista.comAún no hay calificaciones

- CamScanner 12-16-2021 11.38Documento2 páginasCamScanner 12-16-2021 11.38Cronista.comAún no hay calificaciones

- JuntosDocumento6 páginasJuntosCronista.comAún no hay calificaciones

- Frente de TodosDocumento10 páginasFrente de TodosCronista.comAún no hay calificaciones

- Frente Vamos Con VosDocumento4 páginasFrente Vamos Con VosCronista.comAún no hay calificaciones

- YPF 3Q21 Earnings Webcast Presentation FINAL.Documento11 páginasYPF 3Q21 Earnings Webcast Presentation FINAL.Cronista.com100% (1)

- Fdius Ubo Detailed Country Position 2008 2019Documento7 páginasFdius Ubo Detailed Country Position 2008 2019Cronista.comAún no hay calificaciones

- Fdius Ubo Detailed Country Position 2020, BEADocumento5 páginasFdius Ubo Detailed Country Position 2020, BEACronista.comAún no hay calificaciones

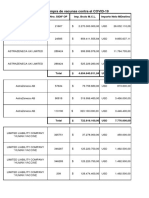

- Pagos Efectuados A LaboratoriosDocumento14 páginasPagos Efectuados A LaboratoriosCronista.comAún no hay calificaciones

- Inversión Extranjera Directa en Los EE - UU. Por País de Origen de Los FondosDocumento19 páginasInversión Extranjera Directa en Los EE - UU. Por País de Origen de Los FondosCronista.comAún no hay calificaciones

- Ley Alivio Fiscal MonotributoDocumento18 páginasLey Alivio Fiscal MonotributoCronista.com100% (1)

- Direct Investment by Country and Industry, 2020Documento12 páginasDirect Investment by Country and Industry, 2020Cronista.com100% (1)

- Gas DeudaDocumento5 páginasGas DeudaCronista.comAún no hay calificaciones

- Soñando Un Mejor ReinicioDocumento4 páginasSoñando Un Mejor ReinicioCronista.comAún no hay calificaciones

- Apéndice Del Acuerdo Mercosur-UE Con El Cronograma de Desgravación TarifariaDocumento122 páginasApéndice Del Acuerdo Mercosur-UE Con El Cronograma de Desgravación TarifariaCronista.com100% (1)

- Ley Alivio Fiscal MonotributoDocumento18 páginasLey Alivio Fiscal MonotributoCronista.com100% (1)

- Deuda Provincia Buenos Aires Propuesta BonistasDocumento6 páginasDeuda Provincia Buenos Aires Propuesta BonistasCronista.comAún no hay calificaciones

- El Informe de The LancetDocumento2 páginasEl Informe de The LancetCronista.comAún no hay calificaciones

- DPForm 12Documento8 páginasDPForm 12vietanhle81Aún no hay calificaciones

- Response of The Filipinos Against The Spanish GovernmentDocumento8 páginasResponse of The Filipinos Against The Spanish GovernmentRan Ran SoraAún no hay calificaciones

- A Quick Introduction To French Contract LawDocumento5 páginasA Quick Introduction To French Contract Lawaminata aboudramaneAún no hay calificaciones

- New World Dystopian Order QuotesDocumento24 páginasNew World Dystopian Order QuotesAnthony Tucker PoindexterAún no hay calificaciones

- Anti-Communist victory in JapanDocumento14 páginasAnti-Communist victory in Japanpabram24105203Aún no hay calificaciones

- Fundamental Rights: Q. What Do You Understand by Fundamental Rights? Discuss With Respect To Indian ConstitutionDocumento4 páginasFundamental Rights: Q. What Do You Understand by Fundamental Rights? Discuss With Respect To Indian ConstitutionShubhika PantAún no hay calificaciones

- Cyberi-Crime Law CaseDocumento11 páginasCyberi-Crime Law CaseVince AbucejoAún no hay calificaciones

- The History of the Philippine FlagDocumento63 páginasThe History of the Philippine FlagDainhil Ann PototAún no hay calificaciones

- DumpingDocumento19 páginasDumpingSahil Sharma100% (1)

- Opposition To Motion For Preliminary InjunctionDocumento49 páginasOpposition To Motion For Preliminary InjunctionBasseemAún no hay calificaciones

- Festin v. ZubiriDocumento2 páginasFestin v. ZubiriDom UmandapAún no hay calificaciones

- Attila and The Huns (1915)Documento254 páginasAttila and The Huns (1915)pomegranate24650% (2)

- Pma 0340 Schedule Baseline Change Request FormDocumento2 páginasPma 0340 Schedule Baseline Change Request FormtabaquiAún no hay calificaciones

- 1.1 Cruz v. DENR PDFDocumento7 páginas1.1 Cruz v. DENR PDFBenBulacAún no hay calificaciones

- BERRIAN v. THE HOUSE OF CORRECTIONS Et Al - Document No. 3Documento5 páginasBERRIAN v. THE HOUSE OF CORRECTIONS Et Al - Document No. 3Justia.comAún no hay calificaciones

- Political System in UKDocumento17 páginasPolitical System in UKIvan Petričević100% (1)

- Rights of Citizens - Civil Rights, Political Rights and Economic RightsDocumento7 páginasRights of Citizens - Civil Rights, Political Rights and Economic RightsvibhuAún no hay calificaciones

- Scheduled Industries (Submission of Production Returns) Rules, 1979Documento3 páginasScheduled Industries (Submission of Production Returns) Rules, 1979Latest Laws TeamAún no hay calificaciones

- Women and Human Rights Project - Protection of Women From Domestic Violence ActDocumento22 páginasWomen and Human Rights Project - Protection of Women From Domestic Violence ActSmriti SrivastavaAún no hay calificaciones

- Resolution No. 248: Province of South CotabatoDocumento2 páginasResolution No. 248: Province of South CotabatoCristina QuincenaAún no hay calificaciones

- Inception ReportDocumento13 páginasInception ReportPrincess TiosejoAún no hay calificaciones

- Four Years of Ukraine and The Myths of MaidanDocumento25 páginasFour Years of Ukraine and The Myths of MaidandtrscrAún no hay calificaciones

- RRB Chandigarh TC CC Previous Exam Paper 2008Documento12 páginasRRB Chandigarh TC CC Previous Exam Paper 2008Unique CreationAún no hay calificaciones

- Coa 2015-014Documento2 páginasCoa 2015-014melizze100% (2)

- Paradise Lost: Politicisation of The Philippine Supreme Court in The Post-Marcos EraDocumento60 páginasParadise Lost: Politicisation of The Philippine Supreme Court in The Post-Marcos EraEM RGAún no hay calificaciones

- 70 Days TNPSC Prelims Test Batch ScheduleDocumento13 páginas70 Days TNPSC Prelims Test Batch SchedulebavithrarajanAún no hay calificaciones

- Pak Study McqsDocumento78 páginasPak Study McqsHafiz Muhammad AkhterAún no hay calificaciones

- Nelson Mandela OutlineDocumento7 páginasNelson Mandela Outlineapi-408858450Aún no hay calificaciones

- Efficient Use of Paper RuleDocumento6 páginasEfficient Use of Paper RuleMaria Margaret Macasaet100% (1)