También podría gustarte

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (119)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (399)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (587)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2219)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2099)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (73)

- Updated Japan Visa RequirementsDocumento2 páginasUpdated Japan Visa RequirementsRheneir MoraAún no hay calificaciones

- Application Form for Funds Transfer via NEFTDocumento2 páginasApplication Form for Funds Transfer via NEFTMohit Goyal50% (4)

- Session 1 - QAR Audit Methodology Manual Presentation - Fundamentals of PSA AuditDocumento34 páginasSession 1 - QAR Audit Methodology Manual Presentation - Fundamentals of PSA AuditRheneir MoraAún no hay calificaciones

- Session 5 - QAR Audit Methodology Manual Presentation - Detailed ProcedureDocumento18 páginasSession 5 - QAR Audit Methodology Manual Presentation - Detailed ProcedureRheneir MoraAún no hay calificaciones

- Session 6 - QAR Audit Methodology Manual Presentation - Review and FinalizationDocumento23 páginasSession 6 - QAR Audit Methodology Manual Presentation - Review and FinalizationRheneir MoraAún no hay calificaciones

- Session 2 - QAR Audit Methodology Manual - IsQMDocumento49 páginasSession 2 - QAR Audit Methodology Manual - IsQMRheneir MoraAún no hay calificaciones

- Cta CaseDocumento10 páginasCta Caselucial_68Aún no hay calificaciones

- Case of Air BlueDocumento10 páginasCase of Air Blueshah_zain89Aún no hay calificaciones

- Ahmedabad MainlineDocumento14 páginasAhmedabad MainlineDolly NadarAún no hay calificaciones

- Session 3 - QAR Audit Methodology Manual Presentation - Intro To The ManualDocumento12 páginasSession 3 - QAR Audit Methodology Manual Presentation - Intro To The ManualRheneir MoraAún no hay calificaciones

- Session 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsDocumento55 páginasSession 4 - QAR Audit Methodology Manual - Pre-Engagement, Planning and Test of ControlsRheneir Mora100% (1)

- Bir Train Law PresentationDocumento74 páginasBir Train Law PresentationPAULINE KRISTINE FULGENCIO100% (3)

- BO2 Case Digest Nos. 11-20Documento8 páginasBO2 Case Digest Nos. 11-20kumag2Aún no hay calificaciones

- Brickman & Joyner, Cpas Room Revenue Analytical: PurposeDocumento2 páginasBrickman & Joyner, Cpas Room Revenue Analytical: PurposeDendy BossAún no hay calificaciones

- PunchTab - Group 10Documento2 páginasPunchTab - Group 10Sudhanshu VermaAún no hay calificaciones

- Marikina Shoe Industry's Struggles and Prospects for RevivalDocumento4 páginasMarikina Shoe Industry's Struggles and Prospects for RevivalHowell FelicildaAún no hay calificaciones

- Banglore of Customer DatabaseDocumento30 páginasBanglore of Customer DatabaseSarita JoshiAún no hay calificaciones

- List of Company SlogansDocumento62 páginasList of Company SlogansrajalaksmiramAún no hay calificaciones

- Digital DisruptionDocumento112 páginasDigital DisruptionSyndicated News100% (4)

- Fun Golf SolicitationDocumento2 páginasFun Golf SolicitationRheneir MoraAún no hay calificaciones

- PAREB AMLC Online Registration System GuideDocumento72 páginasPAREB AMLC Online Registration System GuideRheneir MoraAún no hay calificaciones

- Peach.confirmation.QQ5775Documento3 páginasPeach.confirmation.QQ5775Rheneir MoraAún no hay calificaciones

- Peach.confirmation.EU88X5Documento3 páginasPeach.confirmation.EU88X5Rheneir MoraAún no hay calificaciones

- Talisay Central Eagles ClubDocumento5 páginasTalisay Central Eagles ClubRheneir MoraAún no hay calificaciones

- Certificate SphinxDocumento1 páginaCertificate SphinxRheneir MoraAún no hay calificaciones

- Electronic Ticket Receipt 26MAR For RHENEIR PARAN MORADocumento3 páginasElectronic Ticket Receipt 26MAR For RHENEIR PARAN MORARheneir MoraAún no hay calificaciones

- Or Wiib511710389303Documento1 páginaOr Wiib511710389303Marjorie Unabia HernandoAún no hay calificaciones

- Cebu Pacific Air MoraDocumento4 páginasCebu Pacific Air MoraRheneir MoraAún no hay calificaciones

- SourceTech Consultancy LLCDocumento11 páginasSourceTech Consultancy LLCRheneir MoraAún no hay calificaciones

- Annual Business BudgetDocumento22 páginasAnnual Business BudgetGeisson Martinez GenaoAún no hay calificaciones

- 2019notice New Forms and Pre EvaluationDocumento29 páginas2019notice New Forms and Pre EvaluationRheneir MoraAún no hay calificaciones

- Differences PFRSDocumento11 páginasDifferences PFRSRheneir MoraAún no hay calificaciones

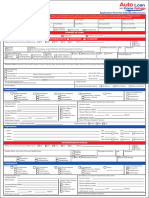

- New Auto-Loan-Application-Form - IndividualDocumento2 páginasNew Auto-Loan-Application-Form - IndividualRheneir MoraAún no hay calificaciones

- MS Call CardsDocumento3 páginasMS Call CardsRheneir MoraAún no hay calificaciones

- 1MSADocumento1 página1MSARheneir MoraAún no hay calificaciones

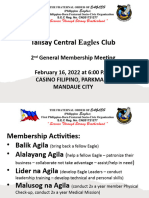

- GMM ProgramDocumento1 páginaGMM ProgramRheneir MoraAún no hay calificaciones

- 77th ANC CebuDocumento7 páginas77th ANC CebuRheneir MoraAún no hay calificaciones

- 49 Insights July 2022Documento41 páginas49 Insights July 2022Rheneir MoraAún no hay calificaciones

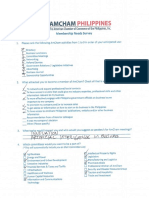

- Amcham Phil. Membership SurveyDocumento2 páginasAmcham Phil. Membership SurveyRheneir Mora100% (1)

- Accreditation of APO and AIPODocumento24 páginasAccreditation of APO and AIPOteguhsunyotoAún no hay calificaciones

- 04 Property PicturesDocumento1 página04 Property PicturesRheneir MoraAún no hay calificaciones

- 03 - List of PropertiesDocumento4 páginas03 - List of PropertiesRheneir MoraAún no hay calificaciones

- Resolution Anti Dengue Clean UpDocumento1 páginaResolution Anti Dengue Clean UpLeei AhrrAún no hay calificaciones

- Brand PT BBIDocumento13 páginasBrand PT BBIapi-3854746Aún no hay calificaciones

- Airline CodesDocumento26 páginasAirline CodesSavita PooniaAún no hay calificaciones

- Vietnam Brochure PDFDocumento6 páginasVietnam Brochure PDFManuel Pinilla CastiblancoAún no hay calificaciones

- Cairo University Chemical Engineering Exam Notes and Solutions 2002-2009Documento95 páginasCairo University Chemical Engineering Exam Notes and Solutions 2002-2009fanus100% (1)

- Business DailyDocumento32 páginasBusiness DailyDennis SegeraAún no hay calificaciones

- ACCT3101 Tutorial 3 SolutionsDocumento4 páginasACCT3101 Tutorial 3 SolutionsAnonymous 7CxwuBUJz3Aún no hay calificaciones

- Chapter 2 Financial Institutions, Financial Intermediaries, and Asset Management FirmsDocumento19 páginasChapter 2 Financial Institutions, Financial Intermediaries, and Asset Management FirmsDavid GreyAún no hay calificaciones

- Report Part 2 ProblemDocumento49 páginasReport Part 2 ProblemMd Khaled NoorAún no hay calificaciones

- Capital Adequacy and Liquidity Risk AnalysisDocumento18 páginasCapital Adequacy and Liquidity Risk AnalysisTural100% (1)

- TQM AssignmentDocumento7 páginasTQM AssignmentGaurav JainAún no hay calificaciones

- 03-28-2013 Agm Minutes RevisedDocumento2 páginas03-28-2013 Agm Minutes Revisedapi-66493924Aún no hay calificaciones

- 12 2 9Documento1 página12 2 9AshleyAún no hay calificaciones

- Calatagan Golf Club v. ClementeDocumento15 páginasCalatagan Golf Club v. ClementeThessaloe B. FernandezAún no hay calificaciones

- M/S. Lavish Ceramics: The Project Cost 1 Cost of ProjectDocumento20 páginasM/S. Lavish Ceramics: The Project Cost 1 Cost of ProjectSabhaya ChiragAún no hay calificaciones

- CV Azhar ArifinDocumento9 páginasCV Azhar ArifinAzhar ArifinAún no hay calificaciones

- Quick Ref Guide: Booking Easyjet Through AmadeusDocumento21 páginasQuick Ref Guide: Booking Easyjet Through AmadeusAkinsanya Adeshina AdewaleAún no hay calificaciones

- Class 11 Cbse Business Studies Syllabus 2012-13Documento4 páginasClass 11 Cbse Business Studies Syllabus 2012-13Sunaina RawatAún no hay calificaciones