También podría gustarte

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- Asm PDFDocumento32 páginasAsm PDFKen PioAún no hay calificaciones

- PDF 1640 PDFDocumento3 páginasPDF 1640 PDFKen PioAún no hay calificaciones

- PHL Country Report PDFDocumento230 páginasPHL Country Report PDFKen PioAún no hay calificaciones

- The Harvard Law Review Association Harvard Law ReviewDocumento15 páginasThe Harvard Law Review Association Harvard Law ReviewKen PioAún no hay calificaciones

- Resume PelegrinoCLEMENCE PDFDocumento1 páginaResume PelegrinoCLEMENCE PDFKen PioAún no hay calificaciones

- Al Bien Christian R. Aculan: Computer SkillsDocumento1 páginaAl Bien Christian R. Aculan: Computer SkillsKen PioAún no hay calificaciones

- Practical Guide Ifrs11 PDFDocumento8 páginasPractical Guide Ifrs11 PDFKen PioAún no hay calificaciones

- Clemence Gil E. Pelegrino: Computer SkillsDocumento1 páginaClemence Gil E. Pelegrino: Computer SkillsKen PioAún no hay calificaciones

- GroupreportGuide2018 PDFDocumento4 páginasGroupreportGuide2018 PDFKen PioAún no hay calificaciones

- Chapter 2 090716 PDFDocumento24 páginasChapter 2 090716 PDFKen PioAún no hay calificaciones

- 2018DormAppSchedule PDFDocumento1 página2018DormAppSchedule PDFKen PioAún no hay calificaciones

- BA129 Outline CigaretteIndustry PDFDocumento2 páginasBA129 Outline CigaretteIndustry PDFKen PioAún no hay calificaciones

- Summary - January 17, 2018Documento4 páginasSummary - January 17, 2018Ken PioAún no hay calificaciones

- Comprehensive Quiz 1Documento11 páginasComprehensive Quiz 1Ken PioAún no hay calificaciones

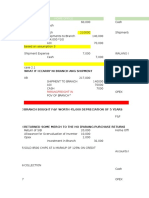

- Advanced Accounting Home and Branch AccountingDocumento14 páginasAdvanced Accounting Home and Branch AccountingKen PioAún no hay calificaciones

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- Free ConsentDocumento2 páginasFree Consentkashif hamidAún no hay calificaciones

- Government of India Ministry of External Affairs CPV Division, DelhiDocumento49 páginasGovernment of India Ministry of External Affairs CPV Division, Delhianu100% (1)

- List of Firms 01 07 19Documento2 páginasList of Firms 01 07 19Umar ArshadAún no hay calificaciones

- Response To Paul Stenhouse's - Islam's Trojan HorseDocumento36 páginasResponse To Paul Stenhouse's - Islam's Trojan HorseNazeer AhmadAún no hay calificaciones

- License Management (5G RAN6.1 - Draft A)Documento75 páginasLicense Management (5G RAN6.1 - Draft A)VVLAún no hay calificaciones

- NY State Official Election ResultsDocumento40 páginasNY State Official Election ResultsBloomberg PoliticsAún no hay calificaciones

- Calculus Early Transcendentals 2nd Edition Briggs Solutions ManualDocumento12 páginasCalculus Early Transcendentals 2nd Edition Briggs Solutions Manualcrenate.bakshish.7ca96100% (28)

- Majestytwelve - MJ12Documento3 páginasMajestytwelve - MJ12Impello_Tyrannis100% (2)

- Social Studies g10 Course Outline and GuidelinesDocumento4 páginasSocial Studies g10 Course Outline and Guidelinesapi-288515796100% (1)

- Module 2 Hindu Intestate SuccessionDocumento17 páginasModule 2 Hindu Intestate SuccessionMamta Navneet SainiAún no hay calificaciones

- Trans PenaDocumento3 páginasTrans Penavivi putriAún no hay calificaciones

- 1 What Is TortDocumento8 páginas1 What Is TortDonasco Casinoo ChrisAún no hay calificaciones

- Agilent G2571-65400 (Tested) - SPW IndustrialDocumento4 páginasAgilent G2571-65400 (Tested) - SPW Industrialervano1969Aún no hay calificaciones

- Global Systems Support: Cobas C 501Documento2 páginasGlobal Systems Support: Cobas C 501Nguyễn PhúAún no hay calificaciones

- 1a Makaleb Crowley My NotesDocumento1 página1a Makaleb Crowley My Notesapi-426853793Aún no hay calificaciones

- Charles Steward Mott Foundation LetterDocumento2 páginasCharles Steward Mott Foundation LetterDave BondyAún no hay calificaciones

- Scratch Your BrainDocumento22 páginasScratch Your BrainTrancemissionAún no hay calificaciones

- Crimea Case StudyDocumento19 páginasCrimea Case StudyNoyonika DeyAún no hay calificaciones

- Subhash Chandra Bose The Untold StoryDocumento9 páginasSubhash Chandra Bose The Untold StoryMrudula BandreAún no hay calificaciones

- ShopFloorControl TG v2014SE EEDocumento112 páginasShopFloorControl TG v2014SE EEpmallikAún no hay calificaciones

- Police Log October 1, 2016Documento10 páginasPolice Log October 1, 2016MansfieldMAPoliceAún no hay calificaciones

- Usage of Word SalafDocumento33 páginasUsage of Word Salafnone0099Aún no hay calificaciones

- Press Release of New Michigan Children's Services Director Herman McCallDocumento2 páginasPress Release of New Michigan Children's Services Director Herman McCallBeverly TranAún no hay calificaciones

- IHub's Memorandum in Opposition To COR's Motion To Compel ProductionDocumento73 páginasIHub's Memorandum in Opposition To COR's Motion To Compel ProductionjaniceshellAún no hay calificaciones

- Duterte Approves Mandatory ROTC Senior HighDocumento1 páginaDuterte Approves Mandatory ROTC Senior HighSteeeeeeeephAún no hay calificaciones

- FIS V Plus ETADocumento14 páginasFIS V Plus ETAHOANG KHANH SONAún no hay calificaciones

- Historical Development of Land Disputes and Their Implications On Social Cohesion in Nakuru County, KenyaDocumento11 páginasHistorical Development of Land Disputes and Their Implications On Social Cohesion in Nakuru County, KenyaInternational Journal of Innovative Science and Research TechnologyAún no hay calificaciones

- MRP Project ReportDocumento82 páginasMRP Project ReportRaneel IslamAún no hay calificaciones

- Division 1 NGODocumento183 páginasDivision 1 NGOAbu Bakkar SiddiqAún no hay calificaciones