También podría gustarte

- Inventory Part2Documento13 páginasInventory Part2Elai grace Fernandez100% (3)

- Intercompany Sales - Inventories ProblemsDocumento13 páginasIntercompany Sales - Inventories ProblemsMhelka Tiodianco100% (2)

- Chapter 16Documento27 páginasChapter 16Red Christian Palustre100% (1)

- P2 06Documento9 páginasP2 06Herald Gangcuangco33% (3)

- Quiz - 3 ABC Problem SolvingDocumento6 páginasQuiz - 3 ABC Problem SolvingAngelito Mamersonal0% (1)

- Business Combination Problem SetDocumento6 páginasBusiness Combination Problem SetbigbaekAún no hay calificaciones

- ADV2 Chapter12 QADocumento4 páginasADV2 Chapter12 QAMa Alyssa DelmiguezAún no hay calificaciones

- Business Combination NotesDocumento3 páginasBusiness Combination NotesKenneth Calzado67% (3)

- Consolidated StatementsDocumento4 páginasConsolidated StatementsRyan Joseph Agluba Dimacali100% (1)

- Business Combi - SubsequentDocumento5 páginasBusiness Combi - Subsequentnaser100% (2)

- YowDocumento35 páginasYowJane Michelle Eman100% (1)

- Long Quiz 2Documento8 páginasLong Quiz 2CattleyaAún no hay calificaciones

- 09 Separate and Consolidated Financial StatementsDocumento17 páginas09 Separate and Consolidated Financial StatementsJAY AUBREY PINEDA0% (1)

- HOBADocumento4 páginasHOBAHannah YnciertoAún no hay calificaciones

- Corporate LiquidationDocumento7 páginasCorporate LiquidationJemarie Alamon100% (1)

- Review MCQDocumento2 páginasReview MCQKrista FloresAún no hay calificaciones

- 09 Additional NotesDocumento4 páginas09 Additional NotesMelody GumbaAún no hay calificaciones

- HO, B & A AcctgDocumento15 páginasHO, B & A AcctgCarolina Fortez Dacanay71% (7)

- Adv AFARDocumento145 páginasAdv AFARDvcLouisAún no hay calificaciones

- Intercompany (Inventories)Documento6 páginasIntercompany (Inventories)Ma Hadassa O. FolienteAún no hay calificaciones

- Sample Problems For Joint Venture and ConsignmentDocumento1 páginaSample Problems For Joint Venture and ConsignmentChristine Jane RamosAún no hay calificaciones

- Polytechnic University of The PhilippinesDocumento12 páginasPolytechnic University of The PhilippinesKyla Dane P. Prado0% (1)

- Consolidated FS Subsequent To Date of AcquisitionDocumento50 páginasConsolidated FS Subsequent To Date of AcquisitionJasmine Marie Ng Cheong60% (5)

- CPA Board Examination Operation - Advance Accounting: Page 1 of 11Documento11 páginasCPA Board Examination Operation - Advance Accounting: Page 1 of 11Janella Patrizia0% (1)

- C Par First Pre Board 2008 ADocumento17 páginasC Par First Pre Board 2008 AJaylord Pido100% (1)

- Business CombinationDocumento10 páginasBusiness CombinationCloudKielGuiang0% (1)

- Business CombinationDocumento3 páginasBusiness Combinationlov3m3Aún no hay calificaciones

- Advanced Accounting Baker Test Bank - Chap020Documento31 páginasAdvanced Accounting Baker Test Bank - Chap020donkazotey100% (2)

- Chapter 8: Home Office, Branch, and Agency AccountingDocumento32 páginasChapter 8: Home Office, Branch, and Agency Accountingjammy Agno50% (2)

- Abc Stock AcquisitionDocumento13 páginasAbc Stock AcquisitionMary Joy AlbandiaAún no hay calificaciones

- AC11 - Chaapter 7Documento34 páginasAC11 - Chaapter 7anon_467190796100% (1)

- C. The Results of Operations, Cash Flow, and The Balance Sheet As If The Parent and Subsidiary Were A Single EntityDocumento13 páginasC. The Results of Operations, Cash Flow, and The Balance Sheet As If The Parent and Subsidiary Were A Single EntityAlijah MercadoAún no hay calificaciones

- Activity Ans KeyDocumento2 páginasActivity Ans KeyJuly LumantasAún no hay calificaciones

- Midterm Exams - Pract 2 (1st Sem 2012-2013)Documento13 páginasMidterm Exams - Pract 2 (1st Sem 2012-2013)jjjjjjjjjjjjjjjAún no hay calificaciones

- Partnership & Business CombinationDocumento32 páginasPartnership & Business CombinationJason Bautista100% (1)

- Corporate LiquidationDocumento7 páginasCorporate LiquidationNathallie CabalunaAún no hay calificaciones

- Advanced Accounting Drill ProblemsDocumento6 páginasAdvanced Accounting Drill ProblemsiajycAún no hay calificaciones

- AFAR Final Preboard 2018 PDFDocumento22 páginasAFAR Final Preboard 2018 PDFcardos cherryAún no hay calificaciones

- Practical Accounting Problem 2Documento18 páginasPractical Accounting Problem 2JimmyChao100% (2)

- Advance Accounting 2 by GuerreroDocumento13 páginasAdvance Accounting 2 by Guerreromarycayton100% (7)

- Consolidated FS & Intercompany TransactionsDocumento5 páginasConsolidated FS & Intercompany TransactionsJalieha MahmodAún no hay calificaciones

- Chapter 7Documento17 páginasChapter 7Kurt dela TorreAún no hay calificaciones

- Long-Term Construction Contracts (Special Revenue Recognition) JLM Illustrative Problems Problem 1Documento5 páginasLong-Term Construction Contracts (Special Revenue Recognition) JLM Illustrative Problems Problem 1Divine Cuasay100% (1)

- p2 - Guerrero Ch9Documento49 páginasp2 - Guerrero Ch9JerichoPedragosa72% (36)

- Ch4 Test BankDocumento70 páginasCh4 Test Bank斌王Aún no hay calificaciones

- Business Combination Subsequent To Date of AcquisitionDocumento1 páginaBusiness Combination Subsequent To Date of AcquisitionAdrian MontemayorAún no hay calificaciones

- Advnce - fin.Acc.&Repprac 2Documento17 páginasAdvnce - fin.Acc.&Repprac 2Jerry Licayan0% (1)

- Uloc Answer Key Let's Check: A. Contingent ConsiderationsDocumento2 páginasUloc Answer Key Let's Check: A. Contingent Considerationszee abadillaAún no hay calificaciones

- Acctg Changes, Error Correction, Prior ErrorDocumento3 páginasAcctg Changes, Error Correction, Prior ErrorLayJohn LacadenAún no hay calificaciones

- Name: DEC. 17, 2020 Buscom ScoreDocumento4 páginasName: DEC. 17, 2020 Buscom ScoreErica DaprosaAún no hay calificaciones

- Intercompany TransactionsDocumento7 páginasIntercompany TransactionsJulie Mae Caling MalitAún no hay calificaciones

- Multiple Choices - Computational Answer KeyDocumento4 páginasMultiple Choices - Computational Answer KeyAleah kay BalontongAún no hay calificaciones

- Seatwork - Module 1Documento5 páginasSeatwork - Module 1Alyanna Alcantara100% (1)

- Quiz AppliedDocumento12 páginasQuiz AppliedLharissa Ballesteros100% (1)

- Business Combination and Consolidated FS 2020 PDFDocumento22 páginasBusiness Combination and Consolidated FS 2020 PDFAPO 0005100% (1)

- QUIZ AKL (D4-FEB Unpad)Documento2 páginasQUIZ AKL (D4-FEB Unpad)Laksmi Banowati Sadmoko HadiAún no hay calificaciones

- Buscom Subsequent MeasurementDocumento6 páginasBuscom Subsequent MeasurementCarmela BautistaAún no hay calificaciones

- Practical Accounting 1Documento8 páginasPractical Accounting 1Mina Bianca AutencioAún no hay calificaciones

- Exercise 4.1Documento2 páginasExercise 4.1Nicole Anne Santiago SibuloAún no hay calificaciones

- While Preparing Its 2016 Financial StatementsDocumento1 páginaWhile Preparing Its 2016 Financial Statementsdagohoy kennethAún no hay calificaciones

- Opinion PNP Clearance RequirementDocumento2 páginasOpinion PNP Clearance RequirementCattleyaAún no hay calificaciones

- Sample Affidavit of No Land HoldingDocumento1 páginaSample Affidavit of No Land HoldingCattleyaAún no hay calificaciones

- Demand LetterDocumento1 páginaDemand LetterCattleyaAún no hay calificaciones

- People Vs SitonDocumento13 páginasPeople Vs SitonCattleya100% (1)

- Sample Demand LetterDocumento1 páginaSample Demand LetterCattleyaAún no hay calificaciones

- Case - Article 4 of RPCDocumento8 páginasCase - Article 4 of RPCCattleyaAún no hay calificaciones

- Republic Act No 7080 PlunderDocumento32 páginasRepublic Act No 7080 PlunderCattleyaAún no hay calificaciones

- The CaseDocumento173 páginasThe CaseCattleyaAún no hay calificaciones

- House of Representatives Electoral Tribunal and Teodoro C. CRUZ, RespondentsDocumento9 páginasHouse of Representatives Electoral Tribunal and Teodoro C. CRUZ, RespondentsCattleyaAún no hay calificaciones

- PD 483Documento4 páginasPD 483CattleyaAún no hay calificaciones

- Digest - Article 4 of RPCDocumento1 páginaDigest - Article 4 of RPCCattleyaAún no hay calificaciones

- Arbitral Tribunal of The International Tribunal For The Law of The SeaDocumento7 páginasArbitral Tribunal of The International Tribunal For The Law of The SeaCattleyaAún no hay calificaciones

- RepublicDocumento5 páginasRepublicCattleyaAún no hay calificaciones

- MELLIZA Vs CITY OF ILOILO (23 SCRA 477) Case Digest Facts: Juliana Melliza During Her Lifetime Owned, Among Other Properties, 3 Parcels ofDocumento12 páginasMELLIZA Vs CITY OF ILOILO (23 SCRA 477) Case Digest Facts: Juliana Melliza During Her Lifetime Owned, Among Other Properties, 3 Parcels ofCattleyaAún no hay calificaciones

- An Overview of Laudato SiDocumento7 páginasAn Overview of Laudato SiCattleyaAún no hay calificaciones

- CASE DIGEST: Teodoro Acap Vs CA, Edy Delos Reyes G.R. No. 118114 December 7, 1995 (251 SCRA 30) (Yellow Pad Digest)Documento10 páginasCASE DIGEST: Teodoro Acap Vs CA, Edy Delos Reyes G.R. No. 118114 December 7, 1995 (251 SCRA 30) (Yellow Pad Digest)CattleyaAún no hay calificaciones

- Manongson Vs EstimoDocumento5 páginasManongson Vs EstimoCattleyaAún no hay calificaciones

- Case 3 - Pangasinan Transportation Co. Vs Public Service Commission, June 24, 1940Documento6 páginasCase 3 - Pangasinan Transportation Co. Vs Public Service Commission, June 24, 1940CattleyaAún no hay calificaciones

- Legal Ethics BAR NotesDocumento9 páginasLegal Ethics BAR NotesCattleyaAún no hay calificaciones

- Digest 3 - Kuroda vs. Jalandoni, March 26, 1949Documento1 páginaDigest 3 - Kuroda vs. Jalandoni, March 26, 1949CattleyaAún no hay calificaciones

- Digest 11 - Fonacier Vs CA, January 28, 1955Documento1 páginaDigest 11 - Fonacier Vs CA, January 28, 1955CattleyaAún no hay calificaciones

- Basic Rights of WorkersDocumento15 páginasBasic Rights of WorkersCattleyaAún no hay calificaciones

- Fisher, Dewitt, Perkins and Brady For Appellant. Attorney-General Villa-Real For AppelleeDocumento14 páginasFisher, Dewitt, Perkins and Brady For Appellant. Attorney-General Villa-Real For AppelleeCattleyaAún no hay calificaciones

- Article 1 To 10 RPCDocumento2 páginasArticle 1 To 10 RPCCattleyaAún no hay calificaciones

- Agency Theory - PresentationDocumento14 páginasAgency Theory - PresentationSaeed AhmadAún no hay calificaciones

- Financial Statement Analysis Lenovo Final 1Documento18 páginasFinancial Statement Analysis Lenovo Final 1api-32197850550% (2)

- 2018 BNCDocumento478 páginas2018 BNCsarrraAún no hay calificaciones

- What Is The Meaning of Book Value Per Share?Documento6 páginasWhat Is The Meaning of Book Value Per Share?Emely Grace YanongAún no hay calificaciones

- MINI CASE Capital DecisionsDocumento2 páginasMINI CASE Capital DecisionsHassham Yousuf0% (1)

- Capital Structure, The Determinants and FeaturesDocumento5 páginasCapital Structure, The Determinants and FeaturesRianto StgAún no hay calificaciones

- Prelim Exam On CrpGov, BussEthiDocumento3 páginasPrelim Exam On CrpGov, BussEthiddddddaaaaeeeeAún no hay calificaciones

- Computation of DividendsDocumento29 páginasComputation of DividendsGela Blanca SantiagoAún no hay calificaciones

- Imron Sahid NugrohoDocumento7 páginasImron Sahid NugrohoAnanda LukmanAún no hay calificaciones

- Bar Exam Questions Asked by Justice HernandoDocumento8 páginasBar Exam Questions Asked by Justice HernandoElla CardenasAún no hay calificaciones

- Company Law Unit 3Documento54 páginasCompany Law Unit 3athought60Aún no hay calificaciones

- IIM Calcutta - Job Description Form - Summer Placements'19: White Oak Capital ManagementDocumento2 páginasIIM Calcutta - Job Description Form - Summer Placements'19: White Oak Capital ManagementVaishnaviRaviAún no hay calificaciones

- Ipo RHP RategainDocumento614 páginasIpo RHP Rategaing_sivakumarAún no hay calificaciones

- Chapter 26 - Fundamentals of Corporate Finance 9th Edition - Test BankDocumento23 páginasChapter 26 - Fundamentals of Corporate Finance 9th Edition - Test BankKellyGibbons100% (3)

- Welcome To Our Presentation: Presentation On Audit ReportDocumento9 páginasWelcome To Our Presentation: Presentation On Audit ReportIubianAún no hay calificaciones

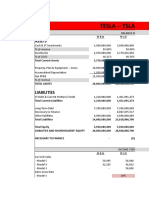

- Tesla ForecastDocumento6 páginasTesla ForecastDanikaLiAún no hay calificaciones

- MLBI Annual Report 2015Documento216 páginasMLBI Annual Report 2015tiffanyAún no hay calificaciones

- Quiz 1Documento7 páginasQuiz 1qwertyuiopAún no hay calificaciones

- Ringkasan Performa Perusahaan Tercatat BTEKDocumento3 páginasRingkasan Performa Perusahaan Tercatat BTEKMonalisa FajiraAún no hay calificaciones

- No. 3 Mercantile Bar 2017Documento2 páginasNo. 3 Mercantile Bar 2017Venice SantibanezAún no hay calificaciones

- Seagate QuestionsDocumento2 páginasSeagate QuestionsCoolminded Coolminded50% (2)

- Corporate RestructuringDocumento19 páginasCorporate RestructuringVaibhav KaushikAún no hay calificaciones

- Reliance Infrastructure 091113 01Documento4 páginasReliance Infrastructure 091113 01Vishakha KhannaAún no hay calificaciones

- KKR Investor UpdateDocumento8 páginasKKR Investor Updatepucci23Aún no hay calificaciones

- Financial Modeling & ValuationDocumento71 páginasFinancial Modeling & ValuationKoray Çelik67% (3)

- Corporate Governance and Foreign InvestmentDocumento10 páginasCorporate Governance and Foreign InvestmentGagan KauraAún no hay calificaciones

- Agreement HSIIDCDocumento15 páginasAgreement HSIIDCGirish Sharma50% (4)

- Fsa 2012 16Documento190 páginasFsa 2012 16Muhammad Shahzad IjazAún no hay calificaciones

- Financial Forecasting Numericals RK-1Documento1 páginaFinancial Forecasting Numericals RK-1Akshay DalviAún no hay calificaciones

- Warrants and ConvertiblesDocumento13 páginasWarrants and ConvertiblesJanelle ChinAún no hay calificaciones

- 12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurDe Everand12 Months to $1 Million: How to Pick a Winning Product, Build a Real Business, and Become a Seven-Figure EntrepreneurCalificación: 4.5 de 5 estrellas4.5/5 (3)

- To Pixar and Beyond: My Unlikely Journey with Steve Jobs to Make Entertainment HistoryDe EverandTo Pixar and Beyond: My Unlikely Journey with Steve Jobs to Make Entertainment HistoryCalificación: 4 de 5 estrellas4/5 (26)

- The Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeDe EverandThe Millionaire Fastlane, 10th Anniversary Edition: Crack the Code to Wealth and Live Rich for a LifetimeCalificación: 4.5 de 5 estrellas4.5/5 (90)

- Secrets of the Millionaire Mind: Mastering the Inner Game of WealthDe EverandSecrets of the Millionaire Mind: Mastering the Inner Game of WealthCalificación: 4.5 de 5 estrellas4.5/5 (1027)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)De EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Calificación: 4.5 de 5 estrellas4.5/5 (14)

- Having It All: Achieving Your Life's Goals and DreamsDe EverandHaving It All: Achieving Your Life's Goals and DreamsCalificación: 4.5 de 5 estrellas4.5/5 (65)

- SYSTEMology: Create time, reduce errors and scale your profits with proven business systemsDe EverandSYSTEMology: Create time, reduce errors and scale your profits with proven business systemsCalificación: 5 de 5 estrellas5/5 (48)

- Every Tool's a Hammer: Life Is What You Make ItDe EverandEvery Tool's a Hammer: Life Is What You Make ItCalificación: 4.5 de 5 estrellas4.5/5 (249)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDe EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindCalificación: 5 de 5 estrellas5/5 (231)

- Summary of Zero to One: Notes on Startups, or How to Build the FutureDe EverandSummary of Zero to One: Notes on Startups, or How to Build the FutureCalificación: 4.5 de 5 estrellas4.5/5 (100)

- Summary of The Subtle Art of Not Giving A F*ck: A Counterintuitive Approach to Living a Good Life by Mark Manson: Key Takeaways, Summary & Analysis IncludedDe EverandSummary of The Subtle Art of Not Giving A F*ck: A Counterintuitive Approach to Living a Good Life by Mark Manson: Key Takeaways, Summary & Analysis IncludedCalificación: 4.5 de 5 estrellas4.5/5 (38)

- Cryptocurrency for Beginners: A Complete Guide to Understanding the Crypto Market from Bitcoin, Ethereum and Altcoins to ICO and Blockchain TechnologyDe EverandCryptocurrency for Beginners: A Complete Guide to Understanding the Crypto Market from Bitcoin, Ethereum and Altcoins to ICO and Blockchain TechnologyCalificación: 4.5 de 5 estrellas4.5/5 (300)

- Brand Identity Breakthrough: How to Craft Your Company's Unique Story to Make Your Products IrresistibleDe EverandBrand Identity Breakthrough: How to Craft Your Company's Unique Story to Make Your Products IrresistibleCalificación: 4.5 de 5 estrellas4.5/5 (48)

- Summary of The Four Agreements: A Practical Guide to Personal Freedom (A Toltec Wisdom Book) by Don Miguel RuizDe EverandSummary of The Four Agreements: A Practical Guide to Personal Freedom (A Toltec Wisdom Book) by Don Miguel RuizCalificación: 4.5 de 5 estrellas4.5/5 (112)

- The Master Key System: 28 Parts, Questions and AnswersDe EverandThe Master Key System: 28 Parts, Questions and AnswersCalificación: 5 de 5 estrellas5/5 (62)

- 24 Assets: Create a digital, scalable, valuable and fun business that will thrive in a fast changing worldDe Everand24 Assets: Create a digital, scalable, valuable and fun business that will thrive in a fast changing worldCalificación: 5 de 5 estrellas5/5 (20)

- The Science of Positive Focus: Live Seminar: Master Keys for Reaching Your Next LevelDe EverandThe Science of Positive Focus: Live Seminar: Master Keys for Reaching Your Next LevelCalificación: 5 de 5 estrellas5/5 (51)

- ChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveDe EverandChatGPT Side Hustles 2024 - Unlock the Digital Goldmine and Get AI Working for You Fast with More Than 85 Side Hustle Ideas to Boost Passive Income, Create New Cash Flow, and Get Ahead of the CurveAún no hay calificaciones

- Getting to Yes: How to Negotiate Agreement Without Giving InDe EverandGetting to Yes: How to Negotiate Agreement Without Giving InCalificación: 4 de 5 estrellas4/5 (652)

- Summary of The E-Myth Revisited: Why Most Small Businesses Don't Work and What to Do About It by Michael E. GerberDe EverandSummary of The E-Myth Revisited: Why Most Small Businesses Don't Work and What to Do About It by Michael E. GerberCalificación: 5 de 5 estrellas5/5 (39)

- Your Next Five Moves: Master the Art of Business StrategyDe EverandYour Next Five Moves: Master the Art of Business StrategyCalificación: 5 de 5 estrellas5/5 (802)

- Take Your Shot: How to Grow Your Business, Attract More Clients, and Make More MoneyDe EverandTake Your Shot: How to Grow Your Business, Attract More Clients, and Make More MoneyCalificación: 5 de 5 estrellas5/5 (22)

- The E-Myth Revisited: Why Most Small Businesses Don't Work andDe EverandThe E-Myth Revisited: Why Most Small Businesses Don't Work andCalificación: 4.5 de 5 estrellas4.5/5 (709)

- Entrepreneurial You: Monetize Your Expertise, Create Multiple Income Streams, and ThriveDe EverandEntrepreneurial You: Monetize Your Expertise, Create Multiple Income Streams, and ThriveCalificación: 4.5 de 5 estrellas4.5/5 (89)

- What Self-Made Millionaires Do That Most People Don't: 52 Ways to Create Your Own SuccessDe EverandWhat Self-Made Millionaires Do That Most People Don't: 52 Ways to Create Your Own SuccessCalificación: 4.5 de 5 estrellas4.5/5 (25)

- Summary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisDe EverandSummary: Choose Your Enemies Wisely: Business Planning for the Audacious Few: Key Takeaways, Summary and AnalysisCalificación: 4.5 de 5 estrellas4.5/5 (3)

- Technofeudalism: What Killed CapitalismDe EverandTechnofeudalism: What Killed CapitalismCalificación: 5 de 5 estrellas5/5 (1)

- Think Like Amazon: 50 1/2 Ideas to Become a Digital LeaderDe EverandThink Like Amazon: 50 1/2 Ideas to Become a Digital LeaderCalificación: 4.5 de 5 estrellas4.5/5 (60)