También podría gustarte

- Binary Options Ebook PDFDocumento19 páginasBinary Options Ebook PDFDan ȘtețAún no hay calificaciones

- Seagate 2Documento5 páginasSeagate 2Bruno Peña Jaramillo33% (3)

- Capital Markets OverviewDocumento16 páginasCapital Markets OverviewRavi Chaurasia100% (1)

- Zerda, Jessa Mae P. BSA 202 QuestionsDocumento21 páginasZerda, Jessa Mae P. BSA 202 Questionsjessa mae zerda50% (2)

- IMT CeresDocumento6 páginasIMT CeresDebasish PattanaikAún no hay calificaciones

- Template 2 Task 3 Calculation Worksheet - BSBFIM601Documento17 páginasTemplate 2 Task 3 Calculation Worksheet - BSBFIM601Writing Experts0% (1)

- J.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineDe EverandJ.K. Lasser's Small Business Taxes 2021: Your Complete Guide to a Better Bottom LineAún no hay calificaciones

- AHM13e Chapter 05 Solution To Problems and Key To CasesDocumento21 páginasAHM13e Chapter 05 Solution To Problems and Key To CasesGaurav ManiyarAún no hay calificaciones

- AP-5906 ReceivablesDocumento6 páginasAP-5906 ReceivablesjhouvanAún no hay calificaciones

- Jun18l1-S02pm QaDocumento22 páginasJun18l1-S02pm QajuanAún no hay calificaciones

- AKL Kel 8 - P5-1 P5-4 P5-8 - Eka NisrinaDocumento8 páginasAKL Kel 8 - P5-1 P5-4 P5-8 - Eka NisrinaNur Ayu Mariya100% (2)

- Write Your Answer For Part A HereDocumento9 páginasWrite Your Answer For Part A HereMATHEW JACOBAún no hay calificaciones

- The Supertrend IndicatorDocumento3 páginasThe Supertrend Indicatorpaolo50% (4)

- Using Economic Indicators to Improve Investment AnalysisDe EverandUsing Economic Indicators to Improve Investment AnalysisCalificación: 3.5 de 5 estrellas3.5/5 (1)

- FinQuiz Level2Mock2016Version2JunePMSolutionsDocumento60 páginasFinQuiz Level2Mock2016Version2JunePMSolutionsAjoy RamananAún no hay calificaciones

- Forex Strategy 'Vegas-Wave'Documento5 páginasForex Strategy 'Vegas-Wave'douy2t12geAún no hay calificaciones

- Chapter 3 SolutionsDocumento7 páginasChapter 3 Solutionshassan.murad63% (8)

- Mudarabah and Its Application in Islamic BankingDocumento26 páginasMudarabah and Its Application in Islamic Bankingsaif khanAún no hay calificaciones

- Bajrabarahi Sana Krishi Firm Godavari Municipality - 13, LalitpurDocumento5 páginasBajrabarahi Sana Krishi Firm Godavari Municipality - 13, LalitpurheroAún no hay calificaciones

- Correction of ErrorsDocumento6 páginasCorrection of ErrorsJanjielyn MoralesAún no hay calificaciones

- PROBLEM NO. 1 - Pistons Company: Note: Prepare "T" Accounts Then Post Identified AdjustmentsDocumento13 páginasPROBLEM NO. 1 - Pistons Company: Note: Prepare "T" Accounts Then Post Identified AdjustmentsShiela Mae BautistaAún no hay calificaciones

- AP 59 FinPB - 5.06Documento8 páginasAP 59 FinPB - 5.06Anonymous Lih1laaxAún no hay calificaciones

- ASE2007 Revised Syllabus - Specimen Paper Answers 2008Documento7 páginasASE2007 Revised Syllabus - Specimen Paper Answers 2008WinnieOngAún no hay calificaciones

- Cash Flow AnalysisDocumento4 páginasCash Flow AnalysisMargin Pason RanjoAún no hay calificaciones

- IMT CeresDocumento7 páginasIMT CeresDigvijay Singh RajputAún no hay calificaciones

- FSA Financial StatementsDocumento4 páginasFSA Financial StatementsabidjaysAún no hay calificaciones

- Financial Analysis - Mini Case-Norbrook-Group BDocumento2 páginasFinancial Analysis - Mini Case-Norbrook-Group BErrol ThompsonAún no hay calificaciones

- Ceres Gardening CompanyDocumento6 páginasCeres Gardening Companypallavikotha84Aún no hay calificaciones

- HW On Sinking Fund C Solutions and AnswersDocumento5 páginasHW On Sinking Fund C Solutions and AnswersAmjad Rian MangondatoAún no hay calificaciones

- Audit of Receivables and Sales SolutionsDocumento16 páginasAudit of Receivables and Sales SolutionsNICELLE TAGLEAún no hay calificaciones

- MeharVerma IMT Ceres 240110 163643Documento9 páginasMeharVerma IMT Ceres 240110 163643Mehar VermaAún no hay calificaciones

- 1st-Case-Study - Financial-Statement-Analysis - Group 5Documento18 páginas1st-Case-Study - Financial-Statement-Analysis - Group 5gellie villarinAún no hay calificaciones

- 18PGP238 Indivisual Assignment Group DDocumento4 páginas18PGP238 Indivisual Assignment Group DaaidanrathiAún no hay calificaciones

- Investitionsanalyse - Polar Sports (A)Documento8 páginasInvestitionsanalyse - Polar Sports (A)ScribdTranslationsAún no hay calificaciones

- IMT CeresDocumento11 páginasIMT CeresShivam GuptaAún no hay calificaciones

- Kenjal Store PDFDocumento5 páginasKenjal Store PDFsudhakar ShakyaAún no hay calificaciones

- MI Worksheet Final LectureDocumento3 páginasMI Worksheet Final Lecturethapa_bisAún no hay calificaciones

- MeharVerma IMT CeresDocumento8 páginasMeharVerma IMT CeresMehar VermaAún no hay calificaciones

- Problem16 5acctgDocumento2 páginasProblem16 5acctgAleah kay BalontongAún no hay calificaciones

- Aamir Ali Bba Viii ADocumento9 páginasAamir Ali Bba Viii Aaamir aliAún no hay calificaciones

- Ap 5906 ReceivablesDocumento14 páginasAp 5906 ReceivablesMa. Lou Erika BALITEAún no hay calificaciones

- Answers To PreboardDocumento7 páginasAnswers To PreboardCodeSeekerAún no hay calificaciones

- Excel - Professional Services Inc.: Management Firm of Professional Review and Training Center (PRTC)Documento5 páginasExcel - Professional Services Inc.: Management Firm of Professional Review and Training Center (PRTC)May Grethel Joy Perante100% (1)

- IMT CeresDocumento10 páginasIMT Cerescabmeuk07Aún no hay calificaciones

- UAS PA 2020-2021 Ganjil - JawabanDocumento27 páginasUAS PA 2020-2021 Ganjil - JawabanNuruddin AsyifaAún no hay calificaciones

- IMT - Ceres Case StudyDocumento7 páginasIMT - Ceres Case Studynikitapansare208Aún no hay calificaciones

- Chapter 2Documento40 páginasChapter 2Nisreen Al-shareAún no hay calificaciones

- Kate CheckDocumento2 páginasKate CheckNecky SairahAún no hay calificaciones

- Cash Flow QuestionDocumento2 páginasCash Flow QuestionomairAún no hay calificaciones

- Ivd. Financial StatementDocumento4 páginasIvd. Financial StatementDre AclonAún no hay calificaciones

- Problem Solving 1-4Documento11 páginasProblem Solving 1-4Romina LopezAún no hay calificaciones

- Illustrative Full Set of IFRS For SME Financial StatementsDocumento16 páginasIllustrative Full Set of IFRS For SME Financial StatementsGirma NegashAún no hay calificaciones

- 1st Case Study - Financial Statement AnalysisDocumento6 páginas1st Case Study - Financial Statement AnalysisKimberly SoqueAún no hay calificaciones

- Complete Financial Statements With SCF Direcdt MethodDocumento23 páginasComplete Financial Statements With SCF Direcdt MethodJuja FlorentinoAún no hay calificaciones

- JSW Steel: PrintDocumento2 páginasJSW Steel: PrintSpuran RamtejaAún no hay calificaciones

- Accounts Receivable and AFBDDocumento18 páginasAccounts Receivable and AFBDeia aieAún no hay calificaciones

- Solution To The 1st Deptal (Trade Receivables and Sales)Documento14 páginasSolution To The 1st Deptal (Trade Receivables and Sales)yen claveAún no hay calificaciones

- Ceres Gardening Company Submission TemplateDocumento7 páginasCeres Gardening Company Submission Templatenikitapansare208Aún no hay calificaciones

- UGBS Compiled Past Questions 4 PDFDocumento327 páginasUGBS Compiled Past Questions 4 PDFEbunAún no hay calificaciones

- 8447809Documento11 páginas8447809blackghostAún no hay calificaciones

- Audit RemovalDocumento13 páginasAudit RemovalErika LanezAún no hay calificaciones

- Itsa Excel SheetDocumento7 páginasItsa Excel SheetraheelehsanAún no hay calificaciones

- Answer Key Q2 PDFDocumento6 páginasAnswer Key Q2 PDFNonami AbicoAún no hay calificaciones

- Project ReportDocumento19 páginasProject ReportCA DïvYã PrÁkàsh JäîswãlAún no hay calificaciones

- Cap II Group I RTP Dec2023Documento84 páginasCap II Group I RTP Dec2023pratyushmudbhari340Aún no hay calificaciones

- AP 5905Q InventoriesDocumento3 páginasAP 5905Q Inventoriesaldrin elsisuraAún no hay calificaciones

- Spyder Case Intro: See Templates On Blackboard For WACC and DCF OutputDocumento11 páginasSpyder Case Intro: See Templates On Blackboard For WACC and DCF Outputrock sinhaAún no hay calificaciones

- J.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineDe EverandJ.K. Lasser's Small Business Taxes 2007: Your Complete Guide to a Better Bottom LineAún no hay calificaciones

- AP 59 1stPB - 5.06Documento9 páginasAP 59 1stPB - 5.06Loren Lordwell MoyaniAún no hay calificaciones

- Competitors ProfileDocumento13 páginasCompetitors ProfileLoren Lordwell MoyaniAún no hay calificaciones

- Room "Snooze"Documento2 páginasRoom "Snooze"Loren Lordwell MoyaniAún no hay calificaciones

- BUSINESSDocumento1 páginaBUSINESSLoren Lordwell MoyaniAún no hay calificaciones

- Starbucks FinalDocumento26 páginasStarbucks FinalRICA JOY DELFINAAún no hay calificaciones

- Swet Ganga Hydropower and Construction LTD PDFDocumento58 páginasSwet Ganga Hydropower and Construction LTD PDFAnil KhanalAún no hay calificaciones

- Nama: Sannia Rahma Masrura NIM: 4112001049: Preemptive RightDocumento3 páginasNama: Sannia Rahma Masrura NIM: 4112001049: Preemptive RightSannia Rahma MAún no hay calificaciones

- ADVANCED CORPORATE FINANCE 3rd TermDocumento11 páginasADVANCED CORPORATE FINANCE 3rd TermdixitBhavak DixitAún no hay calificaciones

- Capital Market and SEBIDocumento4 páginasCapital Market and SEBINishant GoyalAún no hay calificaciones

- Investment in Associate ExercisesDocumento7 páginasInvestment in Associate ExercisesJo KeAún no hay calificaciones

- Advanced Accounting: Consolidated Financial Statements-Date of AcquisitionDocumento52 páginasAdvanced Accounting: Consolidated Financial Statements-Date of AcquisitiongoerginamarquezAún no hay calificaciones

- Financial Management and Financial Planning in The OrganizationsDocumento6 páginasFinancial Management and Financial Planning in The OrganizationsJoris IcallaAún no hay calificaciones

- Accounting Principles 8th Edition - Exercises Chapter07Documento9 páginasAccounting Principles 8th Edition - Exercises Chapter07kimkov119Aún no hay calificaciones

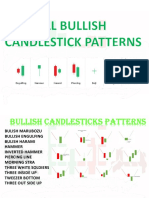

- All Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Documento25 páginasAll Bullish Candlestick Pattern by Optrading00 Telegram Optrading00Samitm TamhankarAún no hay calificaciones

- Lecture 8 - Exercises - SolutionDocumento8 páginasLecture 8 - Exercises - SolutionIsyraf Hatim Mohd TamizamAún no hay calificaciones

- CASE ONE MOTIVATION For Submission OneDocumento7 páginasCASE ONE MOTIVATION For Submission OneFira SyawaliaAún no hay calificaciones

- Unit 2 Prospectus Company LawDocumento9 páginasUnit 2 Prospectus Company LawRanjan BaradurAún no hay calificaciones

- Unit Three Financial AnalysisDocumento56 páginasUnit Three Financial AnalysisHibretAún no hay calificaciones

- Phillip Capital IntroductionDocumento23 páginasPhillip Capital IntroductionSarthakAún no hay calificaciones

- Stocks & BondsDocumento23 páginasStocks & Bondschristian enriquezAún no hay calificaciones

- Equidam Valuation MethodologyDocumento11 páginasEquidam Valuation Methodologydevapps paridAún no hay calificaciones

- AudProb Quiz No. 6 2nd Term SY 2019 2020Documento2 páginasAudProb Quiz No. 6 2nd Term SY 2019 2020Danielle Nicole MarquezAún no hay calificaciones

- The Manner in Which Stakeholders Employ Annual Reports of Companies Listed On The London Stock ExchangeDocumento11 páginasThe Manner in Which Stakeholders Employ Annual Reports of Companies Listed On The London Stock ExchangeNastech ProductionAún no hay calificaciones

- ASR3 Materials - Auditing Equity and Debt InvestmentsDocumento4 páginasASR3 Materials - Auditing Equity and Debt InvestmentsHannah Jane ToribioAún no hay calificaciones

- Focused Hospitality Company Profile Rev8Documento15 páginasFocused Hospitality Company Profile Rev8Komang PriambadaAún no hay calificaciones

- Dispensers California, IncDocumento2 páginasDispensers California, IncRiturajPaulAún no hay calificaciones