También podría gustarte

- Mapping of Petroleum and Minerals Reserves and Resources Classification SystemsDocumento31 páginasMapping of Petroleum and Minerals Reserves and Resources Classification Systemschu AAún no hay calificaciones

- 04 Sec Booking 2018Documento27 páginas04 Sec Booking 2018mohamedAún no hay calificaciones

- Incorporating Numerical Simulation Into Your Reserves Estimation Process Rietz DeanDocumento31 páginasIncorporating Numerical Simulation Into Your Reserves Estimation Process Rietz DeanManuel SantillanAún no hay calificaciones

- Ryder Scott Canada Reserves ConferenceDocumento34 páginasRyder Scott Canada Reserves ConferencecjAún no hay calificaciones

- Geoscience For Petroleum EngineersDocumento39 páginasGeoscience For Petroleum EngineersStélio SalatielAún no hay calificaciones

- Seminar For Reserves EstimatorsDocumento47 páginasSeminar For Reserves EstimatorsGustavo EspinozaAún no hay calificaciones

- 9 Reserve DefinitionsDocumento35 páginas9 Reserve Definitionsdewatharschinia19Aún no hay calificaciones

- World Oil Reserves For UNHAN 26.07.2012Documento46 páginasWorld Oil Reserves For UNHAN 26.07.2012Jimmy Agung SilitongaAún no hay calificaciones

- Spe/Wpc/Aapg Joint Definitions: Not To ScaleDocumento1 páginaSpe/Wpc/Aapg Joint Definitions: Not To Scalemanish.7417Aún no hay calificaciones

- Valuation Methods Mineral ProjectsDocumento13 páginasValuation Methods Mineral ProjectsAji SuhadiAún no hay calificaciones

- 7merging Prms and CogehDocumento32 páginas7merging Prms and CogehJideSalAún no hay calificaciones

- SPE 90241 Can You Have Probable Without Proved Reserves?: Fig. 1 - SPE/WPC/AAPG Resource ClassificationDocumento6 páginasSPE 90241 Can You Have Probable Without Proved Reserves?: Fig. 1 - SPE/WPC/AAPG Resource ClassificationFIRA AULIASARIAún no hay calificaciones

- 2.clasificación y Categorización de HidrocarburosDocumento45 páginas2.clasificación y Categorización de HidrocarburosjuanAún no hay calificaciones

- 1 - Brand/ Reputation Risk: Risk ID Type of Risk Risk Sub-Type Business RiskDocumento7 páginas1 - Brand/ Reputation Risk: Risk ID Type of Risk Risk Sub-Type Business RiskJb TiscubAún no hay calificaciones

- UTI Flexi Cap Fund - Equity Funds - UTI Mutual FundDocumento22 páginasUTI Flexi Cap Fund - Equity Funds - UTI Mutual FundRinku MishraAún no hay calificaciones

- 5 Resiko & Ketidakpastian SlidesDocumento29 páginas5 Resiko & Ketidakpastian Slidesdina mutia sari100% (1)

- TSX-V: Orc.A, Orc.B For Immediate Release: Orca Announces Independent Natural Gas Resource ReportDocumento8 páginasTSX-V: Orc.A, Orc.B For Immediate Release: Orca Announces Independent Natural Gas Resource ReportHussein BoffuAún no hay calificaciones

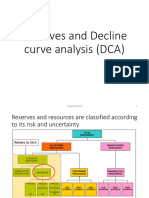

- Reserves and Decline Curve Analysis (DCA) : Azlinda (2017) 1Documento7 páginasReserves and Decline Curve Analysis (DCA) : Azlinda (2017) 1Anthony OnenAún no hay calificaciones

- INWS1DOC10 SoilandDocumento10 páginasINWS1DOC10 SoilandMatsurika Nee ChanAún no hay calificaciones

- Poseidon Brochure - 5pager - 20 10 2017Documento10 páginasPoseidon Brochure - 5pager - 20 10 2017laurent alessioAún no hay calificaciones

- Rbs & Risk Based Internal Audit 22122022Documento73 páginasRbs & Risk Based Internal Audit 22122022Sunny Kumar GuptaAún no hay calificaciones

- UTI Small Cap Fund - Equity Funds - UTI Mutual FundDocumento23 páginasUTI Small Cap Fund - Equity Funds - UTI Mutual FundRinku MishraAún no hay calificaciones

- Day 3-01-Volumetric Reserves Estimates - 1Documento34 páginasDay 3-01-Volumetric Reserves Estimates - 1Haider AshourAún no hay calificaciones

- SCOR 9.0 Quick ReferenceDocumento4 páginasSCOR 9.0 Quick ReferenceRakesh Chandran100% (1)

- Risk Assessment and Risk Controls: Project LocationDocumento3 páginasRisk Assessment and Risk Controls: Project LocationRommel Angelo KirongAún no hay calificaciones

- Proposal Thesis - Thesis FrameworkDocumento2 páginasProposal Thesis - Thesis Frameworkarrizky ayu faradila purnamaAún no hay calificaciones

- Officer Evaluation ReportDocumento32 páginasOfficer Evaluation ReportMark CheneyAún no hay calificaciones

- UTI Large Cap Fund (Formerly UTI Mastershare Unit Scheme)Documento28 páginasUTI Large Cap Fund (Formerly UTI Mastershare Unit Scheme)rinkuparekh13Aún no hay calificaciones

- Saudi Arabian Oil Company: Raw SewageDocumento2 páginasSaudi Arabian Oil Company: Raw SewageAdnanAún no hay calificaciones

- INKED Sales Negotiation Planner Handout 11x17-v6Documento2 páginasINKED Sales Negotiation Planner Handout 11x17-v6Jakub JílekAún no hay calificaciones

- Risk RegisterDocumento11 páginasRisk Registerjoffer idago100% (1)

- Risk / Opportunity Management Register For ProjectDocumento1 páginaRisk / Opportunity Management Register For ProjectnikunjAún no hay calificaciones

- PPPU Prersentation Re EMPO Dec 20, 2022Documento5 páginasPPPU Prersentation Re EMPO Dec 20, 2022Kenneth EnriquezAún no hay calificaciones

- طلبية كاسر الاستحلاب لشركتناDocumento5 páginasطلبية كاسر الاستحلاب لشركتناsara yahyaAún no hay calificaciones

- 4.0 Best Practice - Risk Based InspectionDocumento29 páginas4.0 Best Practice - Risk Based InspectionramuAún no hay calificaciones

- Residual Risk Level Step & Activities Hazard, Env. Aspect Risk, Env. Impacts Resiko DanDocumento1 páginaResidual Risk Level Step & Activities Hazard, Env. Aspect Risk, Env. Impacts Resiko DanIwan RayaAún no hay calificaciones

- Mineral Resource and Reserve Reporting Codes: Why They Are There and Which Ones Apply To Your CompanyDocumento1 páginaMineral Resource and Reserve Reporting Codes: Why They Are There and Which Ones Apply To Your CompanyalokAún no hay calificaciones

- PRMS ClassificationDocumento71 páginasPRMS ClassificationTHE TERMINATORAún no hay calificaciones

- Christie Burger Henk HattinghDocumento28 páginasChristie Burger Henk HattinghSushmit SharmaAún no hay calificaciones

- HIRARC Launching Beam Truss (12561) Contoh ReportDocumento3 páginasHIRARC Launching Beam Truss (12561) Contoh ReportfaizalAún no hay calificaciones

- IC Business Project Risk Assessment Sample 10878Documento4 páginasIC Business Project Risk Assessment Sample 10878sai ramAún no hay calificaciones

- Hiradc ProduksiDocumento156 páginasHiradc ProduksiNur AisyahAún no hay calificaciones

- Building Cybersecurity Capability, Maturity, ResilienceDocumento18 páginasBuilding Cybersecurity Capability, Maturity, ResilienceraAún no hay calificaciones

- 13 Kgopakumar ONGC - IndiaDocumento28 páginas13 Kgopakumar ONGC - Indiapasha khanAún no hay calificaciones

- How To Deal With The Consequences of Earthquakes: Bilal Türkmen TCIP Deputy General SecretaryDocumento22 páginasHow To Deal With The Consequences of Earthquakes: Bilal Türkmen TCIP Deputy General SecretaryChua Chim HueeAún no hay calificaciones

- PROGRAM RELIABILITY IMPROVEMENT IDF UJP IP 2019 Rev2 PDFDocumento35 páginasPROGRAM RELIABILITY IMPROVEMENT IDF UJP IP 2019 Rev2 PDFRizqi Priatna100% (1)

- Presentasi ITDC The Nusa Dua 2018Documento40 páginasPresentasi ITDC The Nusa Dua 2018Rudi Rahmad100% (2)

- Pap Acos Vicnchos 2017.Documento4 páginasPap Acos Vicnchos 2017.jbtenorio6Aún no hay calificaciones

- Accounting For Managerial DecisionDocumento10 páginasAccounting For Managerial DecisionVishal MehtaAún no hay calificaciones

- Spice JetDocumento21 páginasSpice JetSiddhartha Khemka100% (7)

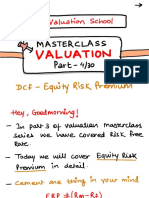

- Valuation Masterclass - 4Documento12 páginasValuation Masterclass - 4shashidhar shindeAún no hay calificaciones

- Reporting Coal Exploration FriederichMDocumento73 páginasReporting Coal Exploration FriederichMDadan100% (1)

- Quality Manual: Process Flow - Liege Belgian Waffle Revision: 06 Document Code: PEGI-HCP-FLO-01 Page 1 of 1Documento1 páginaQuality Manual: Process Flow - Liege Belgian Waffle Revision: 06 Document Code: PEGI-HCP-FLO-01 Page 1 of 1QA PegiwafflesAún no hay calificaciones

- 4a.1 Jairam PDFDocumento47 páginas4a.1 Jairam PDFJaganathan ChokkalingamAún no hay calificaciones

- Explain The First Step Inside This RectangleDocumento1 páginaExplain The First Step Inside This RectangleClint Bryan VirayAún no hay calificaciones

- Calculating Petroleum ReservesDocumento4 páginasCalculating Petroleum ReservesJessica Julien100% (1)

- Website Design Proposal DentistDocumento8 páginasWebsite Design Proposal DentistNamanAún no hay calificaciones

- IOTA Observers Manual All PagesDocumento382 páginasIOTA Observers Manual All PagesMarcelo MartinsAún no hay calificaciones

- 1 - CV - SwarupaGhosh-Solutions Account ManagerDocumento2 páginas1 - CV - SwarupaGhosh-Solutions Account ManagerprabhujainAún no hay calificaciones

- Design Report of STOL Transport AircraftDocumento64 páginasDesign Report of STOL Transport Aircrafthassan wastiAún no hay calificaciones

- BE 503 - Week 1 - Analysis 7.18.11Documento6 páginasBE 503 - Week 1 - Analysis 7.18.11dwoodburyAún no hay calificaciones

- Reglos, DISPUTE FORM 2020Documento2 páginasReglos, DISPUTE FORM 2020Pipoy ReglosAún no hay calificaciones

- Annual Premium Statement: Bhupesh GuptaDocumento1 páginaAnnual Premium Statement: Bhupesh GuptaBhupesh GuptaAún no hay calificaciones

- BasicsDocumento1 páginaBasicsRishi Raj100% (1)

- Matter and Materials (Grade 6 English)Documento80 páginasMatter and Materials (Grade 6 English)Primary Science Programme100% (5)

- 01 Childrenswear Safety Manual 2009 - ClothingDocumento57 páginas01 Childrenswear Safety Manual 2009 - Clothingmorshed_mahamud705538% (8)

- Honeymoon in Vegas Word FileDocumento3 páginasHoneymoon in Vegas Word FileElenaAún no hay calificaciones

- Awareness On Stock MarketDocumento11 páginasAwareness On Stock MarketBharath ReddyAún no hay calificaciones

- Appendix h6 Diffuser Design InvestigationDocumento51 páginasAppendix h6 Diffuser Design InvestigationVeena NageshAún no hay calificaciones

- Model-Checking: A Tutorial Introduction: January 1999Documento26 páginasModel-Checking: A Tutorial Introduction: January 1999Quý Trương QuangAún no hay calificaciones

- Lecture Notes 1 - Finance - Principles of Finance Lecture Notes 1 - Finance - Principles of FinanceDocumento7 páginasLecture Notes 1 - Finance - Principles of Finance Lecture Notes 1 - Finance - Principles of FinanceKim Cristian MaañoAún no hay calificaciones

- Electrochemistry DPP-1Documento2 páginasElectrochemistry DPP-1tarunAún no hay calificaciones

- Ed508-5e-Lesson-Plan-Severe Weather EventsDocumento3 páginasEd508-5e-Lesson-Plan-Severe Weather Eventsapi-526575993Aún no hay calificaciones

- Executing and Releasing Value (V4.0.4.1) - A4Documento27 páginasExecuting and Releasing Value (V4.0.4.1) - A4V100% (1)

- Pega DevOps Release Pipeline OverviewDocumento200 páginasPega DevOps Release Pipeline OverviewArun100% (1)

- Intangible AssetsDocumento16 páginasIntangible Assets566973801967% (3)

- SPE-171076-MS The Role of Asphaltenes in Emulsion Formation For Steam Assisted Gravity Drainage (SAGD) and Expanding Solvent - SAGD (ES-SAGD)Documento14 páginasSPE-171076-MS The Role of Asphaltenes in Emulsion Formation For Steam Assisted Gravity Drainage (SAGD) and Expanding Solvent - SAGD (ES-SAGD)Daniel FelipeAún no hay calificaciones

- ACCA Strategic Business Reporting (SBR) Workbook 2020Documento840 páginasACCA Strategic Business Reporting (SBR) Workbook 2020Azba Nishath0% (1)

- Contemporary Philippine MusicDocumento11 páginasContemporary Philippine MusicmattyuuAún no hay calificaciones

- How To Deliver A Good PresentationDocumento9 páginasHow To Deliver A Good PresentationGhozi Fawwaz Imtiyaazi LabiibaAún no hay calificaciones

- Ev Conversion PDFDocumento2 páginasEv Conversion PDFShannonAún no hay calificaciones

- 16.3 - Precipitation and The Solubility Product - Chemistry LibreTextsDocumento14 páginas16.3 - Precipitation and The Solubility Product - Chemistry LibreTextsThereAún no hay calificaciones

- Department of Accounting and Finances Accounting and Finance ProgramDocumento3 páginasDepartment of Accounting and Finances Accounting and Finance Programwossen gebremariamAún no hay calificaciones

- Axis Bank - Group 4Documento34 páginasAxis Bank - Group 4Deep Ghose DastidarAún no hay calificaciones

- Oleg Losev NegativeDocumento2 páginasOleg Losev NegativeRyan LizardoAún no hay calificaciones

- OMNI OptixDocumento4 páginasOMNI OptixFelipe MoyaAún no hay calificaciones

- The Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsDe EverandThe Black Girl's Guide to Financial Freedom: Build Wealth, Retire Early, and Live the Life of Your DreamsAún no hay calificaciones

- You Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantDe EverandYou Need a Budget: The Proven System for Breaking the Paycheck-to-Paycheck Cycle, Getting Out of Debt, and Living the Life You WantCalificación: 4 de 5 estrellas4/5 (104)

- Budget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.De EverandBudget Management for Beginners: Proven Strategies to Revamp Business & Personal Finance Habits. Stop Living Paycheck to Paycheck, Get Out of Debt, and Save Money for Financial Freedom.Calificación: 5 de 5 estrellas5/5 (91)

- Financial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassDe EverandFinancial Literacy for All: Disrupting Struggle, Advancing Financial Freedom, and Building a New American Middle ClassAún no hay calificaciones

- CDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsDe EverandCDL Study Guide 2022-2023: Everything You Need to Pass Your Exam with Flying Colors on the First Try. Theory, Q&A, Explanations + 13 Interactive TestsCalificación: 4 de 5 estrellas4/5 (4)

- How To Budget And Manage Your Money In 7 Simple StepsDe EverandHow To Budget And Manage Your Money In 7 Simple StepsCalificación: 5 de 5 estrellas5/5 (4)

- Personal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationDe EverandPersonal Finance for Beginners - A Simple Guide to Take Control of Your Financial SituationCalificación: 4.5 de 5 estrellas4.5/5 (18)

- How to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsDe EverandHow to Pay Zero Taxes, 2020-2021: Your Guide to Every Tax Break the IRS AllowsAún no hay calificaciones

- CAPITAL: Vol. 1-3: Complete Edition - Including The Communist Manifesto, Wage-Labour and Capital, & Wages, Price and ProfitDe EverandCAPITAL: Vol. 1-3: Complete Edition - Including The Communist Manifesto, Wage-Labour and Capital, & Wages, Price and ProfitCalificación: 4 de 5 estrellas4/5 (6)

- Swot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessDe EverandSwot analysis in 4 steps: How to use the SWOT matrix to make a difference in career and businessCalificación: 4.5 de 5 estrellas4.5/5 (4)

- The Best Team Wins: The New Science of High PerformanceDe EverandThe Best Team Wins: The New Science of High PerformanceCalificación: 4.5 de 5 estrellas4.5/5 (31)

- The Financial Planning Puzzle: Fitting Your Pieces Together to Create Financial FreedomDe EverandThe Financial Planning Puzzle: Fitting Your Pieces Together to Create Financial FreedomCalificación: 4.5 de 5 estrellas4.5/5 (2)

- The 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)De EverandThe 30-Day Money Cleanse: Take Control of Your Finances, Manage Your Spending, and De-Stress Your Money for Good (Personal Finance and Budgeting Self-Help Book)Calificación: 3.5 de 5 estrellas3.5/5 (9)

- Basic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonDe EverandBasic Python in Finance: How to Implement Financial Trading Strategies and Analysis using PythonCalificación: 5 de 5 estrellas5/5 (9)

- The Money Mentor: How to Pay Off Your Mortgage in as Little as 7 Years Without Becoming a HermitDe EverandThe Money Mentor: How to Pay Off Your Mortgage in as Little as 7 Years Without Becoming a HermitAún no hay calificaciones

- Budgeting: The Ultimate Guide for Getting Your Finances TogetherDe EverandBudgeting: The Ultimate Guide for Getting Your Finances TogetherCalificación: 5 de 5 estrellas5/5 (14)

- Rich Nurse Poor Nurses: The Critical Stuff Nursing School Forgot To Teach YouDe EverandRich Nurse Poor Nurses: The Critical Stuff Nursing School Forgot To Teach YouCalificación: 4 de 5 estrellas4/5 (2)

- Zero To One - Unauthorized 33-Minute SummaryDe EverandZero To One - Unauthorized 33-Minute SummaryCalificación: 5 de 5 estrellas5/5 (1)

- Debt Freedom: A Realistic Guide On How To Eliminate Debt, Including Credit Card Debt ForeverDe EverandDebt Freedom: A Realistic Guide On How To Eliminate Debt, Including Credit Card Debt ForeverCalificación: 3 de 5 estrellas3/5 (2)

- Money Made Easy: How to Budget, Pay Off Debt, and Save MoneyDe EverandMoney Made Easy: How to Budget, Pay Off Debt, and Save MoneyCalificación: 5 de 5 estrellas5/5 (1)

- Radically Simple Accounting: A Way Out of the Dark and Into the ProfitDe EverandRadically Simple Accounting: A Way Out of the Dark and Into the ProfitCalificación: 4.5 de 5 estrellas4.5/5 (9)

- Inflation Hacking: Inflation Investing Techniques to Benefit from High InflationDe EverandInflation Hacking: Inflation Investing Techniques to Benefit from High InflationCalificación: 4.5 de 5 estrellas4.5/5 (5)