También podría gustarte

- Sensex (34916) / Nifty (10302) : Exhibit 1: Nifty Daily ChartDocumento5 páginasSensex (34916) / Nifty (10302) : Exhibit 1: Nifty Daily ChartbbaalluuAún no hay calificaciones

- 0 / 1 Pts 1 / 1 PTS: Question 1 Question 2Documento28 páginas0 / 1 Pts 1 / 1 PTS: Question 1 Question 2Ceej DalipeAún no hay calificaciones

- Installment Sales Nov 2017#1Documento3 páginasInstallment Sales Nov 2017#1Angel Alejo AcobaAún no hay calificaciones

- Wesleyan University - Philippines Accounting for Special Transactions Franchise Proposal for Pugad CompanyDocumento9 páginasWesleyan University - Philippines Accounting for Special Transactions Franchise Proposal for Pugad CompanyChristine Angeli AritaAún no hay calificaciones

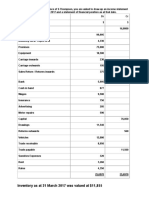

- Inventory As at 31 March 2017 Was Valued at $11,855Documento2 páginasInventory As at 31 March 2017 Was Valued at $11,855Shoaib AslamAún no hay calificaciones

- Sensex (34732) / Nifty (10244) : Exhibit 1: Nifty Daily ChartDocumento5 páginasSensex (34732) / Nifty (10244) : Exhibit 1: Nifty Daily ChartbbaalluuAún no hay calificaciones

- Lab 8 Intercompany Profit Transaction - BondsDocumento2 páginasLab 8 Intercompany Profit Transaction - BondsFatharaniAún no hay calificaciones

- IFRS 15 and Franchising Ppt. ReferenceDocumento19 páginasIFRS 15 and Franchising Ppt. ReferenceKate NuevaAún no hay calificaciones

- Shareholders Equity Part 2Documento15 páginasShareholders Equity Part 2Aira Rhialyn MangubatAún no hay calificaciones

- Managing Journal Entries for PT Kharisma DigitalDocumento92 páginasManaging Journal Entries for PT Kharisma DigitalChoyingOOying80% (25)

- Nfjpia Cup - Auditing Problems SGV & Co. Easy Question #1: Answer: P126,816Documento18 páginasNfjpia Cup - Auditing Problems SGV & Co. Easy Question #1: Answer: P126,816Merliza Jusayan100% (1)

- Financial Accounting and Reporting: IFRS - 2016 June QPDocumento11 páginasFinancial Accounting and Reporting: IFRS - 2016 June QPMarchella LukitoAún no hay calificaciones

- Sensex (38493) / Nifty (11301) : Exhibit 1: Nifty Daily ChartDocumento5 páginasSensex (38493) / Nifty (11301) : Exhibit 1: Nifty Daily ChartbbaalluuAún no hay calificaciones

- E4 5Documento3 páginasE4 5Andrew ChowAún no hay calificaciones

- ASSIGNMENT 4 - QuestionDocumento3 páginasASSIGNMENT 4 - QuestionThemba Patrick Molefe0% (1)

- Consolidated Statements of Changes in EquityDocumento1 páginaConsolidated Statements of Changes in EquityJudith DelRosario De RoxasAún no hay calificaciones

- ACC 4041 Tutorial - Business Income and ExpensesDocumento5 páginasACC 4041 Tutorial - Business Income and ExpensesAyekurik0% (1)

- Sensex (34911) / Nifty (10311) : Exhibit 1: Nifty Daily ChartDocumento5 páginasSensex (34911) / Nifty (10311) : Exhibit 1: Nifty Daily ChartbbaalluuAún no hay calificaciones

- Cash Flow Session With ExamplesDocumento9 páginasCash Flow Session With ExamplesPAVAN KUMAR GUDAVALLETIAún no hay calificaciones

- From The Following Information, Prepare A Cash Flow StatementDocumento2 páginasFrom The Following Information, Prepare A Cash Flow StatementAgAAún no hay calificaciones

- Assignment - QuestionDocumento3 páginasAssignment - QuestionWang Hon YuenAún no hay calificaciones

- Leone Lumber Company Trial Balance As of December 31 Debit CreditDocumento3 páginasLeone Lumber Company Trial Balance As of December 31 Debit CreditMaitaAún no hay calificaciones

- Advanced Accounting Quiz 9 - Installment Sales (Part 2 of 2)Documento6 páginasAdvanced Accounting Quiz 9 - Installment Sales (Part 2 of 2)guardian saintsAún no hay calificaciones

- Tugas Akun 3Documento16 páginasTugas Akun 3Latifah KhalisyahAún no hay calificaciones

- Reg. No.Documento4 páginasReg. No.madhumithaAún no hay calificaciones

- Small Engineering Firm Financial StatementsDocumento1 páginaSmall Engineering Firm Financial StatementsDana SpencerAún no hay calificaciones

- Fundamentals of Accounting Suggested Answer Attempt All Questions. Working Notes Should Form Part of The AnswerDocumento28 páginasFundamentals of Accounting Suggested Answer Attempt All Questions. Working Notes Should Form Part of The AnsweralchemistAún no hay calificaciones

- Sensex (34869) / Nifty (10305) : Exhibit 1: Nifty Daily ChartDocumento5 páginasSensex (34869) / Nifty (10305) : Exhibit 1: Nifty Daily ChartbbaalluuAún no hay calificaciones

- Tutorial MFRS 101 Presentation Financial StatementDocumento4 páginasTutorial MFRS 101 Presentation Financial StatementashabalqisAún no hay calificaciones

- QQAA GREEN TECH Comprehensive ExampleDocumento7 páginasQQAA GREEN TECH Comprehensive ExampleZulhelmy NazriAún no hay calificaciones

- Ap Problems 2016Documento26 páginasAp Problems 2016Christian QuintansAún no hay calificaciones

- SEC B1 Income Statement and Statement of Financial PositionDocumento3 páginasSEC B1 Income Statement and Statement of Financial PositionKəmalə AslanzadəAún no hay calificaciones

- Accounting Week13 Lec01 & Lec02 NotesDocumento3 páginasAccounting Week13 Lec01 & Lec02 NotesABUBAKAR FawadAún no hay calificaciones

- Fam - Session ViiiDocumento4 páginasFam - Session ViiiMukund kelaAún no hay calificaciones

- TABANI’S SCHOOL OF ACCOUNTANCY MOCK EXAMDocumento5 páginasTABANI’S SCHOOL OF ACCOUNTANCY MOCK EXAMBilal ShaikhAún no hay calificaciones

- Company Accounts QuestionsDocumento5 páginasCompany Accounts QuestionsNipuni PereraAún no hay calificaciones

- Problem 7.2Documento4 páginasProblem 7.2Ayesha SidiqAún no hay calificaciones

- Prepare financial statements including provisionsDocumento4 páginasPrepare financial statements including provisionsTendy WatoAún no hay calificaciones

- Seatworks 01 and 02 Audit of EquityDocumento6 páginasSeatworks 01 and 02 Audit of EquityPola PolzAún no hay calificaciones

- Soal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Documento9 páginasSoal Mojakoe-UTS Akuntansi Keuangan 1 Ganjil 2020-2021Vincenttio le CloudAún no hay calificaciones

- CVP Analysis and Decision Making - ExamDocumento9 páginasCVP Analysis and Decision Making - ExamBAún no hay calificaciones

- Adjusting entries and financial statements for Flawless IncDocumento4 páginasAdjusting entries and financial statements for Flawless IncRocel Avery SacroAún no hay calificaciones

- Tutorial Question: Learning Management SystemDocumento4 páginasTutorial Question: Learning Management SystemYee Sin MeiAún no hay calificaciones

- Tax WrokingDocumento1 páginaTax Wrokingdjkaka12Aún no hay calificaciones

- Summarizing (Trial Balance) : (Go Through The Reference Books For Details)Documento6 páginasSummarizing (Trial Balance) : (Go Through The Reference Books For Details)sujitAún no hay calificaciones

- CPA Ireland Financial Accounting 2015-18Documento161 páginasCPA Ireland Financial Accounting 2015-18Ahmed Raza Tanveer100% (1)

- Financial Accounting: Formation 2 Examination - April 2015Documento23 páginasFinancial Accounting: Formation 2 Examination - April 2015Ashura ShaibAún no hay calificaciones

- Acc 305 Capital Gains TaxDocumento18 páginasAcc 305 Capital Gains TaxOnalenna MdongoAún no hay calificaciones

- Payback AnalysisDocumento14 páginasPayback Analysisrabbit_39Aún no hay calificaciones

- Enterprises - Profit and Loss Account13042016Documento4 páginasEnterprises - Profit and Loss Account13042016jelachajelenaAún no hay calificaciones

- Cash Flow QuestionsDocumento5 páginasCash Flow QuestionssigiryaAún no hay calificaciones

- Solution - Audit of InvestmentDocumento4 páginasSolution - Audit of InvestmentMJ YaconAún no hay calificaciones

- Brilliant Cosmetics 2017 financial statement adjustmentsDocumento3 páginasBrilliant Cosmetics 2017 financial statement adjustmentsVilma Tayum100% (1)

- 50 MARKS Accounts Paper CTC ClassesDocumento4 páginas50 MARKS Accounts Paper CTC ClassesMohit SharmaAún no hay calificaciones

- f2 Financial Accounting April 2016Documento20 páginasf2 Financial Accounting April 2016Edson Jorge MandlateAún no hay calificaciones

- International Accounting TranslationDocumento7 páginasInternational Accounting TranslationTrujillo Velázquez BeyanyAún no hay calificaciones

- Soal M. JurnalDocumento36 páginasSoal M. JurnalDKTAún no hay calificaciones

- Tutorial 2 A192 QuestionDocumento9 páginasTutorial 2 A192 QuestionMastura Abd HamidAún no hay calificaciones

- 360digiTMG - Certificate Course On Data Science - CurriculumDocumento12 páginas360digiTMG - Certificate Course On Data Science - CurriculummanjushreeAún no hay calificaciones

- Damodaran IntroductionDocumento2 páginasDamodaran IntroductionmanjushreeAún no hay calificaciones

- Regulatory Capture: Regulatory Capture Refers To The Phenomenon of Government Agencies, Created InitiallyDocumento2 páginasRegulatory Capture: Regulatory Capture Refers To The Phenomenon of Government Agencies, Created InitiallymanjushreeAún no hay calificaciones

- International Environmental ForcesDocumento4 páginasInternational Environmental ForcesmanjushreeAún no hay calificaciones

- NSE Co-Location Case Explained: SEBI's Order and its ImpactDocumento2 páginasNSE Co-Location Case Explained: SEBI's Order and its ImpactmanjushreeAún no hay calificaciones

- Job Analysis Work, Job, TaskDocumento15 páginasJob Analysis Work, Job, TaskmanjushreeAún no hay calificaciones

- Ilfs and Ethical AccountingDocumento4 páginasIlfs and Ethical AccountingmanjushreeAún no hay calificaciones

- A Fine Balance - The DPDA and Data Localization - India Corporate LawDocumento7 páginasA Fine Balance - The DPDA and Data Localization - India Corporate LawmanjushreeAún no hay calificaciones

- Scam in India 2022: Relevance: The Editorial Analysis - DHFL Scam - : The Scam Faultline Is Damaging Indian BankingDocumento3 páginasScam in India 2022: Relevance: The Editorial Analysis - DHFL Scam - : The Scam Faultline Is Damaging Indian BankingmanjushreeAún no hay calificaciones

- Recent Cases of Regulatory Laxity in Indian Banking SystemDocumento2 páginasRecent Cases of Regulatory Laxity in Indian Banking SystemmanjushreeAún no hay calificaciones

- CCI Auto Spares OEMDocumento5 páginasCCI Auto Spares OEMmanjushreeAún no hay calificaciones

- 360digiTMG - Certificate Course On Data Science - CurriculumDocumento12 páginas360digiTMG - Certificate Course On Data Science - CurriculummanjushreeAún no hay calificaciones

- India Trade Unions and Collective BargainingDocumento27 páginasIndia Trade Unions and Collective BargainingRamkrishna MondalAún no hay calificaciones

- X-Bar & R Chart Template RevDocumento8 páginasX-Bar & R Chart Template RevmanjushreeAún no hay calificaciones

- Lebs209 PDFDocumento30 páginasLebs209 PDFmanjushreeAún no hay calificaciones

- BA Estimation Furniture Shop Draft IDocumento21 páginasBA Estimation Furniture Shop Draft ImanjushreeAún no hay calificaciones

- Top 4 Theories of Capital StructureDocumento12 páginasTop 4 Theories of Capital StructuremanjushreeAún no hay calificaciones

- Advertisements Consistent With Societal Marketing Concept Advertisement # 1Documento6 páginasAdvertisements Consistent With Societal Marketing Concept Advertisement # 1manjushreeAún no hay calificaciones

- HR Score Card: Submitted by Manjushree Gupta PNR: 16020848004 Semester 3, EMBA 2016-19 SIBM, BengaluruDocumento5 páginasHR Score Card: Submitted by Manjushree Gupta PNR: 16020848004 Semester 3, EMBA 2016-19 SIBM, BengalurumanjushreeAún no hay calificaciones

- HR Score Card: Submitted by Manjushree Gupta PNR: 16020848004 Semester 3, EMBA 2016-19 SIBM, BengaluruDocumento5 páginasHR Score Card: Submitted by Manjushree Gupta PNR: 16020848004 Semester 3, EMBA 2016-19 SIBM, BengalurumanjushreeAún no hay calificaciones

- SWOT N PORTER 5 Forces - Indian PahrmaDocumento21 páginasSWOT N PORTER 5 Forces - Indian Pahrmabhupendraa97% (35)

- Pharma SuggestionsDocumento7 páginasPharma SuggestionsmanjushreeAún no hay calificaciones

- Business Plan Project - Ice Cream ShopDocumento17 páginasBusiness Plan Project - Ice Cream ShopmanjushreeAún no hay calificaciones

- Executive SummaryDocumento7 páginasExecutive SummarymanjushreeAún no hay calificaciones

- ABC Analysis WorksheetDocumento16 páginasABC Analysis WorksheetmanjushreeAún no hay calificaciones

- Corporate Governance at L&TDocumento5 páginasCorporate Governance at L&TmanjushreeAún no hay calificaciones

- Performance Appraisal MethodsDocumento50 páginasPerformance Appraisal Methodsmanjushree0% (1)

- Introduction To Financial StatementsDocumento21 páginasIntroduction To Financial StatementsmanjushreeAún no hay calificaciones

- Manjushreegupta Cge 16020848004Documento4 páginasManjushreegupta Cge 16020848004manjushreeAún no hay calificaciones

- Corporate Governace in InfosysDocumento44 páginasCorporate Governace in InfosyshvnirpharakeAún no hay calificaciones

- Global Depositary Receipt - GDRDocumento12 páginasGlobal Depositary Receipt - GDRSankesh SatputeAún no hay calificaciones

- In 30302854036156Documento2 páginasIn 30302854036156mallikaAún no hay calificaciones

- PLDT v. NTC: Stock Dividends Basis for SRFDocumento1 páginaPLDT v. NTC: Stock Dividends Basis for SRFRobert QuiambaoAún no hay calificaciones

- Finance A Ethics Enron Hyacynthia KesumaDocumento1 páginaFinance A Ethics Enron Hyacynthia KesumaCynthia KesumaAún no hay calificaciones

- Aa2e Hal SM Ch09Documento19 páginasAa2e Hal SM Ch09Jay BrockAún no hay calificaciones

- Ac2301 - Principles of TaxationDocumento13 páginasAc2301 - Principles of TaxationjwinlynAún no hay calificaciones

- BCB Holdings Limited Announces Results For The Second Quarter Ended September 30, 2013Documento4 páginasBCB Holdings Limited Announces Results For The Second Quarter Ended September 30, 2013Ricardo TorresAún no hay calificaciones

- Juan Pedro Sánchez Ballesta, Emma García Meca, 2005 Audit Qualifications and CorporateDocumento17 páginasJuan Pedro Sánchez Ballesta, Emma García Meca, 2005 Audit Qualifications and CorporateMuhammad ApriantoAún no hay calificaciones

- MFS Quality & ValueDocumento4 páginasMFS Quality & ValueJeffrey WilliamsAún no hay calificaciones

- FIN5FMA Tutorial Assessment Task 4 - PracticeDocumento4 páginasFIN5FMA Tutorial Assessment Task 4 - Practicemitul tamakuwalaAún no hay calificaciones

- Chapter Four: Ethics and Social ResponsibilityDocumento40 páginasChapter Four: Ethics and Social ResponsibilityHananie NanieAún no hay calificaciones

- Behavioral Aspects of Cost Management PDFDocumento43 páginasBehavioral Aspects of Cost Management PDFAshutosh PandeyAún no hay calificaciones

- BPI VS SARABIA DigestDocumento2 páginasBPI VS SARABIA Digestchenny abellaAún no hay calificaciones

- Tire City Spreadsheet SolutionDocumento6 páginasTire City Spreadsheet Solutionalmasy99100% (1)

- Uichico Vs NLRC - Officers LiableDocumento2 páginasUichico Vs NLRC - Officers LiableCarl MontemayorAún no hay calificaciones

- FINDocumento10 páginasFINAnbang XiaoAún no hay calificaciones

- ICICI BOM Merger Case StudyDocumento12 páginasICICI BOM Merger Case StudyDeepa Phansikar KakadeAún no hay calificaciones

- Summary of Project Assumptions: Construction CostsDocumento5 páginasSummary of Project Assumptions: Construction CostsjowacocoAún no hay calificaciones

- Kazar Slaven - Chartered Accountants & Insolvency PractitionersDocumento14 páginasKazar Slaven - Chartered Accountants & Insolvency PractitionersKazar SlavenAún no hay calificaciones

- Joint Venture - Beams Ch. 11Documento27 páginasJoint Venture - Beams Ch. 11saskiaAún no hay calificaciones

- Mitsubishi Heavy Industries Business OverviewDocumento156 páginasMitsubishi Heavy Industries Business OverviewMohammed HanafiAún no hay calificaciones

- 9-1c PT Primer, PT Sekunder, PT HoldingDocumento4 páginas9-1c PT Primer, PT Sekunder, PT HoldingToys AdventureAún no hay calificaciones

- Corrections Volume II Chapters 12-19Documento2 páginasCorrections Volume II Chapters 12-19xxxxxxxxxAún no hay calificaciones

- Assignment # 6Documento9 páginasAssignment # 6Ahtsham Ilyas RajputAún no hay calificaciones

- Separation of Ownership and Management in Large CorporationsDocumento5 páginasSeparation of Ownership and Management in Large Corporationscoco100% (5)

- Chapter 2 - Shareholder's Equity MCDocumento19 páginasChapter 2 - Shareholder's Equity MCJoshua AbanalesAún no hay calificaciones

- Stock Valuation and Required Rate of Return ConceptsDocumento3 páginasStock Valuation and Required Rate of Return ConceptsAntonette YapAún no hay calificaciones

- Newsletters 2003 - AVTDocumento7 páginasNewsletters 2003 - AVTAna VellegalAún no hay calificaciones

- B34 - Nautica Canning Corp. V YumulDocumento2 páginasB34 - Nautica Canning Corp. V YumulRap SantosAún no hay calificaciones