También podría gustarte

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- A 20 Point Guide To Passing The Revised Ea ExamDocumento7 páginasA 20 Point Guide To Passing The Revised Ea Exampoet_in_christAún no hay calificaciones

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The SWISSINDO IS PRIVATE & ACTUALLY-ABSOLUTE PDFDocumento16 páginasThe SWISSINDO IS PRIVATE & ACTUALLY-ABSOLUTE PDFWerner Katzbeck91% (11)

- MCQs in MarketingDocumento51 páginasMCQs in MarketingPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- India-The Mother of DemocracyDocumento33 páginasIndia-The Mother of DemocracyPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Posb Manual Volume - 2Documento108 páginasPosb Manual Volume - 2K V Sridharan General Secretary P3 NFPE100% (2)

- Accounting Principle Kieso 8e - Ch01Documento47 páginasAccounting Principle Kieso 8e - Ch01Sania M. JayantiAún no hay calificaciones

- Poa Text BookDocumento548 páginasPoa Text BookSiennaAún no hay calificaciones

- Mubadala Petroleum BrochureDocumento32 páginasMubadala Petroleum BrochureDidiAún no hay calificaciones

- Financing Decisions 2Documento12 páginasFinancing Decisions 2PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Surf Vs NirmaDocumento37 páginasSurf Vs NirmaSudipta BanerjeeAún no hay calificaciones

- Small Business 2 MSME ACT 2020Documento56 páginasSmall Business 2 MSME ACT 2020PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Trade CreditDocumento5 páginasTrade CreditPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- International Business Class 11 CBSEDocumento126 páginasInternational Business Class 11 CBSEPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Aphorism 1Documento21 páginasAphorism 1PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Retained Earnings 3Documento12 páginasRetained Earnings 3PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- MANGLORE To GOA 3Documento53 páginasMANGLORE To GOA 3PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Lease 5Documento16 páginasLease 5PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Mixed Mcqs From CH 4 PlanningDocumento18 páginasMixed Mcqs From CH 4 PlanningPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Factoring Service 2Documento15 páginasFactoring Service 2PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Mixed Mcqs From CH 5 OrganisingDocumento24 páginasMixed Mcqs From CH 5 OrganisingPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Mixed Mcqs From CH 3 Business EnvironmentDocumento17 páginasMixed Mcqs From CH 3 Business EnvironmentPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Mixed Mcqs From CH 6 StaffingDocumento36 páginasMixed Mcqs From CH 6 StaffingPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Mixed Mcqs From CH 8 ControllingDocumento17 páginasMixed Mcqs From CH 8 ControllingPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Mixed Mcqs From CH 7 DirectingDocumento25 páginasMixed Mcqs From CH 7 DirectingPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Case Study On Mass Production - Emerging Modes of BusinessDocumento17 páginasCase Study On Mass Production - Emerging Modes of BusinessPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- OutsourcingDocumento42 páginasOutsourcingPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Benefits of E-CommerceDocumento22 páginasBenefits of E-CommercePUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Business Ethics CH 6Documento18 páginasBusiness Ethics CH 6PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Mixed MCQs From CH 5 XiDocumento70 páginasMixed MCQs From CH 5 XiPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Emerging Modes of Business XI VIVA XI Business StudiesDocumento104 páginasEmerging Modes of Business XI VIVA XI Business StudiesPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- CSR P1 CH 6Documento102 páginasCSR P1 CH 6PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Modes of BusinessDocumento48 páginasModes of BusinessPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

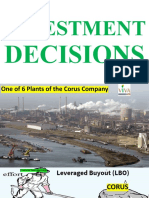

- Investment Decisions 1Documento23 páginasInvestment Decisions 1PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Class 12 Business Studies Chapter 12 MCQ'sDocumento41 páginasClass 12 Business Studies Chapter 12 MCQ'sPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Emerging Modes of Business VIVA BS XIDocumento104 páginasEmerging Modes of Business VIVA BS XIPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Answers To Mcqs CH 10, CHAPTER 10 FINANCIAL MARKETS CBSE XIIDocumento82 páginasAnswers To Mcqs CH 10, CHAPTER 10 FINANCIAL MARKETS CBSE XIIPUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Dividend Decisions3Documento13 páginasDividend Decisions3PUTTU GURU PRASAD SENGUNTHA MUDALIARAún no hay calificaciones

- Caso Europet WordDocumento11 páginasCaso Europet WordvapadabaAún no hay calificaciones

- Career Snapshot (Incase of Work Exp) Career Objective (In Case of Fresher)Documento3 páginasCareer Snapshot (Incase of Work Exp) Career Objective (In Case of Fresher)istadevaAún no hay calificaciones

- Charge Slip BillingDocumento129 páginasCharge Slip BillingMitch Panghilino CandoAún no hay calificaciones

- Costco Comprehensive AnalysisDocumento11 páginasCostco Comprehensive AnalysisAlex GaoAún no hay calificaciones

- Auditing 1 Revisions Chapter 4 To 15 - SEM 2 2012: SolutionDocumento6 páginasAuditing 1 Revisions Chapter 4 To 15 - SEM 2 2012: SolutionBao NguyenAún no hay calificaciones

- Tax ReconDocumento12 páginasTax ReconArah Monica Dela TorreAún no hay calificaciones

- TOS AFAR RevisedDocumento9 páginasTOS AFAR RevisedAdmin ElenaAún no hay calificaciones

- Volt Trucking LLCDocumento1 páginaVolt Trucking LLC9newsAún no hay calificaciones

- Treasurer'S Affidavit: Doc. No. - Page No. - Book No. - Series of 20Documento1 páginaTreasurer'S Affidavit: Doc. No. - Page No. - Book No. - Series of 20Edgar EnriquezAún no hay calificaciones

- US Economic Indicators: Corporate Profits in GDP: Yardeni Research, IncDocumento16 páginasUS Economic Indicators: Corporate Profits in GDP: Yardeni Research, IncJames HeartfieldAún no hay calificaciones

- Stock IndiaDocumento300 páginasStock IndiaNANDKISHORAún no hay calificaciones

- Answer of The Case Questions: 1. Answer: Summary of The CaseDocumento10 páginasAnswer of The Case Questions: 1. Answer: Summary of The Caseনিশীথিনী কুহুরানীAún no hay calificaciones

- Kunci JWB pkt2. 3 PDsuburDocumento45 páginasKunci JWB pkt2. 3 PDsuburSyifa FaAún no hay calificaciones

- 2017 Agm MinutesDocumento6 páginas2017 Agm Minutesapi-248973401Aún no hay calificaciones

- Virginia Agreement With AmazonDocumento25 páginasVirginia Agreement With AmazonFOX 5 NewsAún no hay calificaciones

- Types of Organisational Structures: Their Advantages and Disadvantages!Documento16 páginasTypes of Organisational Structures: Their Advantages and Disadvantages!nitish kumar twariAún no hay calificaciones

- Equity Detail of UniversitiesDocumento5 páginasEquity Detail of UniversitiesThe Wonders EdgeAún no hay calificaciones

- Sahara InidaDocumento5 páginasSahara InidaRicha UmraoAún no hay calificaciones

- Donor's Tax A) Basic Principles, Concept and DefinitionDocumento4 páginasDonor's Tax A) Basic Principles, Concept and DefinitionAnonymous YNTVcDAún no hay calificaciones

- 51 BookReview Venema StormySkies PaulClark WithPrefaceDocumento2 páginas51 BookReview Venema StormySkies PaulClark WithPrefaceW.J. Zondag100% (1)

- Vrio Group ClientDocumento4 páginasVrio Group ClientEkam SurreyAún no hay calificaciones

- History of Insurance Business in BangladeshDocumento3 páginasHistory of Insurance Business in BangladeshBishawnath Roy67% (3)

- Subordinate LegislationDocumento4 páginasSubordinate LegislationHenteLAWcoAún no hay calificaciones