También podría gustarte

- IP EvaluationDocumento33 páginasIP EvaluationAnonymous wA6NGuyklDAún no hay calificaciones

- Soybean Fiber: A Healthy and Comfortable Fibre of the 21st CenturyDocumento12 páginasSoybean Fiber: A Healthy and Comfortable Fibre of the 21st CenturyAnonymous wA6NGuyklDAún no hay calificaciones

- Compare and Contrast Toyotas Manufacturi PDFDocumento1 páginaCompare and Contrast Toyotas Manufacturi PDFAnonymous wA6NGuyklDAún no hay calificaciones

- Balancing Simulation-2008 PDFDocumento12 páginasBalancing Simulation-2008 PDFAnonymous wA6NGuyklDAún no hay calificaciones

- Dyeing soybean fibre with reactive dyesDocumento5 páginasDyeing soybean fibre with reactive dyesAnonymous wA6NGuyklDAún no hay calificaciones

- Make Through Manufacturing MethodsDocumento8 páginasMake Through Manufacturing Methodstheriteshtiwari100% (1)

- Implementation of Lean Manufacturing Principles in FoundriesDocumento5 páginasImplementation of Lean Manufacturing Principles in FoundriesIJMERAún no hay calificaciones

- Fabric Science PDFDocumento18 páginasFabric Science PDFAnonymous wA6NGuyklD100% (3)

- Pengurusan Kualiti Organisasi PendidikanDocumento30 páginasPengurusan Kualiti Organisasi PendidikanKomalah PurusothmanAún no hay calificaciones

- Bemand EdiDocumento19 páginasBemand EdiAnonymous wA6NGuyklDAún no hay calificaciones

- Balancing Simulation-2008 PDFDocumento12 páginasBalancing Simulation-2008 PDFAnonymous wA6NGuyklDAún no hay calificaciones

- Universal Declaration of Human RightsDocumento19 páginasUniversal Declaration of Human RightsHendrik GozaliAún no hay calificaciones

- Continuous Sampling PlanDocumento2 páginasContinuous Sampling PlanAnonymous wA6NGuyklDAún no hay calificaciones

- Apparel Supply ChainDocumento35 páginasApparel Supply ChainAnonymous wA6NGuyklD100% (1)

- Café Moto' Feasibility StudyDocumento9 páginasCafé Moto' Feasibility StudyAnonymous wA6NGuyklDAún no hay calificaciones

- A Journey Over The Innovation of H M-LibreDocumento25 páginasA Journey Over The Innovation of H M-LibreAnonymous wA6NGuyklDAún no hay calificaciones

- Mens Essential NeedsDocumento5 páginasMens Essential NeedsUndercoverJumperAún no hay calificaciones

- Acceptance SamplingDocumento13 páginasAcceptance SamplingAnonymous wA6NGuyklDAún no hay calificaciones

- Working Condition Sewing Floor PDFDocumento6 páginasWorking Condition Sewing Floor PDFAnonymous wA6NGuyklDAún no hay calificaciones

- Lean Manufacturing HandbookDocumento15 páginasLean Manufacturing HandbookZakir Qureshi75% (4)

- Specsheet PDFDocumento2 páginasSpecsheet PDFAnonymous wA6NGuyklDAún no hay calificaciones

- Measuring Production Effeciency of Readymade Garment Firms PDFDocumento12 páginasMeasuring Production Effeciency of Readymade Garment Firms PDFAnonymous wA6NGuyklDAún no hay calificaciones

- Comprehensive Trade and Economic AgreementDocumento3 páginasComprehensive Trade and Economic AgreementAnonymous wA6NGuyklDAún no hay calificaciones

- New Osha300form1!1!04 FormsOnlyDocumento3 páginasNew Osha300form1!1!04 FormsOnlyShabir ShuhoodAún no hay calificaciones

- Supply Chain ManagementDocumento31 páginasSupply Chain ManagementAnonymous wA6NGuyklDAún no hay calificaciones

- Production overviewDocumento2 páginasProduction overviewAnonymous wA6NGuyklDAún no hay calificaciones

- Computerizedmachine 2 PDFDocumento8 páginasComputerizedmachine 2 PDFAnonymous wA6NGuyklDAún no hay calificaciones

- Bossard - Accv12 - Apparel Classification With Style PDFDocumento14 páginasBossard - Accv12 - Apparel Classification With Style PDFAnonymous wA6NGuyklDAún no hay calificaciones

- Hava Arabic English LexiconDocumento928 páginasHava Arabic English LexiconattahiruAún no hay calificaciones

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (265)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (73)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (119)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2099)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- Brake Pedals and ValveDocumento4 páginasBrake Pedals and Valveala17Aún no hay calificaciones

- Brief Summary of The Original COCOMO ModelDocumento5 páginasBrief Summary of The Original COCOMO ModelTirthajit SinhaAún no hay calificaciones

- Geo-Informatics and Nano-Technology For Precision FARMING (AGRO-301) 5 SemesterDocumento5 páginasGeo-Informatics and Nano-Technology For Precision FARMING (AGRO-301) 5 SemesterVinod Vincy67% (3)

- Grant Park Platform Bedroom Set Furniture RowDocumento1 páginaGrant Park Platform Bedroom Set Furniture Rowjyzjz6sr65Aún no hay calificaciones

- JonWeisseBUS450 04 HPDocumento3 páginasJonWeisseBUS450 04 HPJonathan WeisseAún no hay calificaciones

- Industry 4.0 FinaleDocumento25 páginasIndustry 4.0 FinaleFrame UkirkacaAún no hay calificaciones

- Manuel Solaris Ccds1425-St Ccds1425-Dn Ccds1425-Dnx Ccds1425-Dn36en deDocumento42 páginasManuel Solaris Ccds1425-St Ccds1425-Dn Ccds1425-Dnx Ccds1425-Dn36en deAllegra AmiciAún no hay calificaciones

- COSTECH Accelration of Innovation ImbejuDocumento42 páginasCOSTECH Accelration of Innovation Imbejuhamidumajid033Aún no hay calificaciones

- Aesculap: F E S SDocumento28 páginasAesculap: F E S SEcole AcharafAún no hay calificaciones

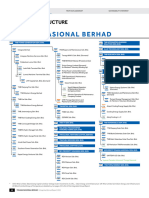

- TNB AR 2022 Corporate StructureDocumento2 páginasTNB AR 2022 Corporate StructureZamzuri P AminAún no hay calificaciones

- SPW3 Manual Rev 5Documento713 páginasSPW3 Manual Rev 5JPYadavAún no hay calificaciones

- Degx1 Dggx1 Us PartsDocumento24 páginasDegx1 Dggx1 Us PartsJeff RussoAún no hay calificaciones

- TN 46Documento23 páginasTN 46Khalil AhmadAún no hay calificaciones

- RCE Unpacking Ebook (Translated by LithiumLi) - UnprotectedDocumento2342 páginasRCE Unpacking Ebook (Translated by LithiumLi) - Unprotecteddryten7507Aún no hay calificaciones

- The Future of Smart Cities and RegionsDocumento20 páginasThe Future of Smart Cities and RegionsChristianAún no hay calificaciones

- POSSIBILITIES OF LOW VOLTAGE DC SYSTEMSDocumento10 páginasPOSSIBILITIES OF LOW VOLTAGE DC SYSTEMSTTaanAún no hay calificaciones

- Environmentally-Friendly LPG Forklift Trucks with Superior Power & PerformanceDocumento5 páginasEnvironmentally-Friendly LPG Forklift Trucks with Superior Power & PerformanceCarlos Miguel Apipilhuasco GonzálezAún no hay calificaciones

- DPWH Standard Specifications for ShotcreteDocumento12 páginasDPWH Standard Specifications for ShotcreteDino Garzon OcinoAún no hay calificaciones

- Automotive Control SystemsDocumento406 páginasAutomotive Control SystemsDenis Martins Dantas100% (3)

- India's Growing Social Media Landscape and Future TrendsDocumento5 páginasIndia's Growing Social Media Landscape and Future Trendspriyaa2688Aún no hay calificaciones

- Admin Interview Questions and Answers - Robert HalfDocumento2 páginasAdmin Interview Questions and Answers - Robert HalfWaqqas AhmadAún no hay calificaciones

- A Polypropylene Film With Excellent Clarity Combined With Avery Dennison Clearcut™ Adhesive Technology and With A Glassine LinerDocumento4 páginasA Polypropylene Film With Excellent Clarity Combined With Avery Dennison Clearcut™ Adhesive Technology and With A Glassine LinerAhmad HaririAún no hay calificaciones

- Module 8 SAHITA ConcreteDocumento11 páginasModule 8 SAHITA ConcreteHarrybfnAún no hay calificaciones

- Selection ToolsDocumento13 páginasSelection ToolsDominador Gaduyon DadalAún no hay calificaciones

- Builder's Greywater Guide Branched DrainDocumento4 páginasBuilder's Greywater Guide Branched DrainGreen Action Sustainable Technology GroupAún no hay calificaciones

- Electronic Ticket Receipt, November 03 For MR ARAYA GEBRESLASSIE BERHEDocumento2 páginasElectronic Ticket Receipt, November 03 For MR ARAYA GEBRESLASSIE BERHEMengstu Gebreslassie50% (2)

- Human Plus Machine A New Era of Automation in ManufacturingDocumento8 páginasHuman Plus Machine A New Era of Automation in ManufacturingDuarte CRosaAún no hay calificaciones

- Rising Stem Ball ValveDocumento6 páginasRising Stem Ball ValveAnupam A. GandhewarAún no hay calificaciones

- Reaction PaperDocumento2 páginasReaction PaperRonald CostalesAún no hay calificaciones