También podría gustarte

- Zagan UlDocumento4 páginasZagan UlAlexandru ReleaAún no hay calificaciones

- QuotesDocumento2 páginasQuotesAlexandru ReleaAún no hay calificaciones

- Objectives and Target ZaganuDocumento1 páginaObjectives and Target ZaganuAlexandru ReleaAún no hay calificaciones

- InstallationDocumento1 páginaInstallationAlexandru ReleaAún no hay calificaciones

- Research On Effect of Beijing Post-Olympic Sports Industry To China's Economic DevelopmentDocumento6 páginasResearch On Effect of Beijing Post-Olympic Sports Industry To China's Economic DevelopmentAlexandru ReleaAún no hay calificaciones

- JobDocumento1 páginaJobAlexandru ReleaAún no hay calificaciones

- Fatal1ty FM2A88X+ Killer SeriesDocumento77 páginasFatal1ty FM2A88X+ Killer SeriesAlexandru ReleaAún no hay calificaciones

- QuotesDocumento3 páginasQuotesAlexandru ReleaAún no hay calificaciones

- Accounting - Seminar 13 SolutionsDocumento3 páginasAccounting - Seminar 13 SolutionsAlexandru ReleaAún no hay calificaciones

- Economics in One LessonDocumento4 páginasEconomics in One LessonAlexandru ReleaAún no hay calificaciones

- Never Push A Loyal Person To The Point Where They No Longer Give A Fuck! in Times of Peace The Warlike Man Attacks HimselfDocumento1 páginaNever Push A Loyal Person To The Point Where They No Longer Give A Fuck! in Times of Peace The Warlike Man Attacks HimselfAlexandru ReleaAún no hay calificaciones

- Never Push A Loyal Person To The Point Where They No Longer Give A Fuck! in Times of Peace The Warlike Man Attacks HimselfDocumento1 páginaNever Push A Loyal Person To The Point Where They No Longer Give A Fuck! in Times of Peace The Warlike Man Attacks HimselfAlexandru ReleaAún no hay calificaciones

- Psi Ho LogieDocumento2 páginasPsi Ho LogieAlexandru ReleaAún no hay calificaciones

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (587)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (894)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (399)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (73)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2219)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (265)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2099)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (119)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- Central Bank Act MCQDocumento12 páginasCentral Bank Act MCQJemima LalaweAún no hay calificaciones

- Deutsche Bank IP & ID special transfer SWIFT messageDocumento5 páginasDeutsche Bank IP & ID special transfer SWIFT messagehamid nabizade100% (3)

- IBAN Guide for Correspondent BanksDocumento7 páginasIBAN Guide for Correspondent BanksNe VadimAún no hay calificaciones

- SAP FI Transaction Code List 1Documento33 páginasSAP FI Transaction Code List 1Saurabh ChaplotAún no hay calificaciones

- An Internship Report On Risk Management of Exim Bank BangladeshDocumento64 páginasAn Internship Report On Risk Management of Exim Bank BangladeshSumantra Barai25% (4)

- Project On MCB GCUFDocumento19 páginasProject On MCB GCUFAmna Goher100% (1)

- Davao Del Sur Electric Cooperative, Inc. (Dasureco) Cogon, Digos City, Davao Del SurDocumento1 páginaDavao Del Sur Electric Cooperative, Inc. (Dasureco) Cogon, Digos City, Davao Del SurDASURECOWebTeamAún no hay calificaciones

- QMS ProposalDocumento22 páginasQMS Proposalflawlessy2kAún no hay calificaciones

- Palms Shopping Mall-GuideDocumento1 páginaPalms Shopping Mall-Guidesadiq mohammedAún no hay calificaciones

- Snapdeal 170329070435Documento24 páginasSnapdeal 170329070435Sumon BeraAún no hay calificaciones

- Comparative Analysis of Home Loan in UTI BankDocumento95 páginasComparative Analysis of Home Loan in UTI BankMitesh SonegaraAún no hay calificaciones

- Head Of?ice Management: Treasury Se22lomen2Documento3 páginasHead Of?ice Management: Treasury Se22lomen2Rizwan WaryahAún no hay calificaciones

- Study online at quizlet.com/_1lwdnhDocumento3 páginasStudy online at quizlet.com/_1lwdnhPatriciaAún no hay calificaciones

- Big Data Insurance Case Study PDFDocumento2 páginasBig Data Insurance Case Study PDFVivek SaahilAún no hay calificaciones

- #11Documento2 páginas#11Annabelle Bustamante100% (1)

- Credit Risk Analysis of Rupali Bank LimitedDocumento105 páginasCredit Risk Analysis of Rupali Bank Limitedkhansha ComputersAún no hay calificaciones

- Solutions - LiabilitiesDocumento10 páginasSolutions - LiabilitiesjhobsAún no hay calificaciones

- Nego Table of ContentsDocumento7 páginasNego Table of ContentsSham GaerlanAún no hay calificaciones

- Lousianna Tax InstructionDocumento17 páginasLousianna Tax Instructionchuckhsu1248Aún no hay calificaciones

- The Role of Micro Loans in The Mordern Financial Industry-Dessertation 1st DraftDocumento37 páginasThe Role of Micro Loans in The Mordern Financial Industry-Dessertation 1st DraftManika Gupta100% (1)

- 08580XXX1871 2017jun23 2017jul21 PDFDocumento1 página08580XXX1871 2017jun23 2017jul21 PDFAdenAún no hay calificaciones

- Unit 3 Ledger Posting and Trial Balance PDFDocumento46 páginasUnit 3 Ledger Posting and Trial Balance PDFPankaj VishwakarmaAún no hay calificaciones

- FAR.113 - INVESTMENT PROPERTY With Answer PDFDocumento5 páginasFAR.113 - INVESTMENT PROPERTY With Answer PDFMaeAún no hay calificaciones

- Internship Report AB BankDocumento85 páginasInternship Report AB BankDhoni KhanAún no hay calificaciones

- Top NCD Picks and Analysis for May 2014Documento1 páginaTop NCD Picks and Analysis for May 2014shobhaAún no hay calificaciones

- When Does A Letter of Comfort Becomes A Contract of GuaranteeDocumento11 páginasWhen Does A Letter of Comfort Becomes A Contract of GuaranteeJ Imam100% (3)

- 07 Official Lease Fleece Press ReleaseDocumento3 páginas07 Official Lease Fleece Press ReleaseadamisgoingtoprisonAún no hay calificaciones

- Message Type 200Documento6 páginasMessage Type 200Falokun Martins OluwafemiAún no hay calificaciones

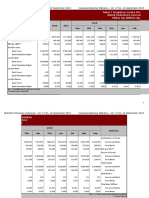

- Indonesia Banking Statistics - Vol. 17 No. 10 September 2019 Table 1.1 Commercial Bank ActivitiesDocumento818 páginasIndonesia Banking Statistics - Vol. 17 No. 10 September 2019 Table 1.1 Commercial Bank ActivitiesDewiAún no hay calificaciones