También podría gustarte

- REI Expo - India Solar Market Update - Whitepaper by Mercom IndiaDocumento42 páginasREI Expo - India Solar Market Update - Whitepaper by Mercom IndiaAbhinav GuptaAún no hay calificaciones

- REI Expo - India Solar Market Update - Whitepaper by Mercom IndiaDocumento42 páginasREI Expo - India Solar Market Update - Whitepaper by Mercom IndiaKunalAún no hay calificaciones

- IEEFA - JMK - Rooftop Solar Commercial and Industrial Market - August 2023Documento36 páginasIEEFA - JMK - Rooftop Solar Commercial and Industrial Market - August 2023saikrishna bethaAún no hay calificaciones

- A Study On Customer Acquisition On EcomitramDocumento28 páginasA Study On Customer Acquisition On EcomitramTanvi Rastogi100% (1)

- 933 Gnull BJ21048 Sec A Group 6 MPIT Assignment 2Documento9 páginas933 Gnull BJ21048 Sec A Group 6 MPIT Assignment 2AryanAún no hay calificaciones

- Untapped Opportunities in Indias Rooftop Solar Market - July 2020Documento46 páginasUntapped Opportunities in Indias Rooftop Solar Market - July 2020Arif Khan NabilAún no hay calificaciones

- India Solar Market Update - Whitepaper by Mercom India Research (Sep 2019)Documento32 páginasIndia Solar Market Update - Whitepaper by Mercom India Research (Sep 2019)Vinutha MBAún no hay calificaciones

- DIEM20220566 Tamanna Ulster GBCDocumento15 páginasDIEM20220566 Tamanna Ulster GBCFarhan IsraqAún no hay calificaciones

- India Solar Handbook 2016 PDFDocumento33 páginasIndia Solar Handbook 2016 PDFalkanm750Aún no hay calificaciones

- Vast Potential of Rooftop Solar in IndiaDocumento15 páginasVast Potential of Rooftop Solar in IndiaSumitSinglaAún no hay calificaciones

- Pranav Bhargav ProjectDocumento65 páginasPranav Bhargav ProjectPranav BhargavAún no hay calificaciones

- The Rising Sun GridDocumento40 páginasThe Rising Sun Gridvishaljoshi28Aún no hay calificaciones

- Business Plan-Global - Power - SolutionsDocumento15 páginasBusiness Plan-Global - Power - SolutionsAshwin KumarAún no hay calificaciones

- Rooftop Solar Private Sector Financing Facility Full ReportDocumento41 páginasRooftop Solar Private Sector Financing Facility Full ReportSonal Tripathy100% (1)

- Organisation Design ReportDocumento17 páginasOrganisation Design ReportMilindGuravAún no hay calificaciones

- SM Project - Tata Solar-Competitive Strategy - Group7 (Section A) - EPGDIB 2014-15Documento18 páginasSM Project - Tata Solar-Competitive Strategy - Group7 (Section A) - EPGDIB 2014-15akshaykgAún no hay calificaciones

- Strategic Analysis of Tata Solar Power's Opportunities and ChallengesDocumento39 páginasStrategic Analysis of Tata Solar Power's Opportunities and ChallengesAkshit GuptaAún no hay calificaciones

- Mishra - Tata Solar Power - PranjalDocumento40 páginasMishra - Tata Solar Power - Pranjalajay chahalAún no hay calificaciones

- Economics Project Report A2Documento14 páginasEconomics Project Report A2N SethAún no hay calificaciones

- SWSL: World's Largest Solar EPC Provider Poised for GrowthDocumento13 páginasSWSL: World's Largest Solar EPC Provider Poised for GrowthAbhishek MishraAún no hay calificaciones

- Yashesve Summer Internship Report 2019Documento71 páginasYashesve Summer Internship Report 2019Ankit TiwariAún no hay calificaciones

- Mercom India Cleantech Report Jul2023Documento13 páginasMercom India Cleantech Report Jul2023aakashAún no hay calificaciones

- Guidebook for Utilities-Led Business Models: Way Forward for Rooftop Solar in IndiaDe EverandGuidebook for Utilities-Led Business Models: Way Forward for Rooftop Solar in IndiaAún no hay calificaciones

- ACME Solar - Team 7Documento15 páginasACME Solar - Team 7Pratik DhakeAún no hay calificaciones

- Market Trends: Establishment of Localized Mini-GridsDocumento5 páginasMarket Trends: Establishment of Localized Mini-GridsAkshay KhandelwalAún no hay calificaciones

- All Stories Peruse Our Archives The Morning ContextDocumento1 páginaAll Stories Peruse Our Archives The Morning Contextashu19Aún no hay calificaciones

- Nuetech Solar Systems Private LimitedDocumento71 páginasNuetech Solar Systems Private LimitedPrashanth PB100% (1)

- Energetic MagazineDocumento84 páginasEnergetic MagazineMeghhsAún no hay calificaciones

- 2013 05 03 Preliminary Concept NoteDocumento10 páginas2013 05 03 Preliminary Concept NoteAnmol Ajay ShethAún no hay calificaciones

- Project of Entrepreneurship: Business Plan of A Start-UpDocumento60 páginasProject of Entrepreneurship: Business Plan of A Start-UpMuhammad SaadAún no hay calificaciones

- Utility-Centric Business Models For Rooftop Solar Projects: PACE-D Technical Assistance ProgramDocumento32 páginasUtility-Centric Business Models For Rooftop Solar Projects: PACE-D Technical Assistance Program6092 ANKIT BEDWALAún no hay calificaciones

- Content 5 Days Training ProgramDocumento2 páginasContent 5 Days Training ProgramSamarendu BaulAún no hay calificaciones

- Issues with India's target of 450GW renewable capacityDocumento3 páginasIssues with India's target of 450GW renewable capacityAparajita MarwahAún no hay calificaciones

- Green Trade Project Office News Articles: *為必填欄位/RequiredDocumento3 páginasGreen Trade Project Office News Articles: *為必填欄位/Requiredkalyani dynamicsAún no hay calificaciones

- Assessing Industrial Energy Transition in Pakistan's Textile SectorDocumento37 páginasAssessing Industrial Energy Transition in Pakistan's Textile SectorKamran AhmedAún no hay calificaciones

- Solar Industry Analysis: 1. Key TrendsDocumento2 páginasSolar Industry Analysis: 1. Key Trendsnijit sharmaAún no hay calificaciones

- BRIDGE To INDIA India Solar Handbook 2015 Online 1Documento28 páginasBRIDGE To INDIA India Solar Handbook 2015 Online 1Nithya Susan VargheseAún no hay calificaciones

- India's Energy Storage Market OutlookDocumento4 páginasIndia's Energy Storage Market OutlookbhanuAún no hay calificaciones

- An Analytical Study of LED Lights To Go Green and Being Energy Efficient - Summer Project Report by Akarsh Srivastava, Roll No - 02, PGDM - MarketingDocumento39 páginasAn Analytical Study of LED Lights To Go Green and Being Energy Efficient - Summer Project Report by Akarsh Srivastava, Roll No - 02, PGDM - MarketingAkarsh Srivastava100% (1)

- Business Plan: Kudakwashe Solomon Mavuru Paul Henri Hie Nathan KuchenaDocumento24 páginasBusiness Plan: Kudakwashe Solomon Mavuru Paul Henri Hie Nathan Kuchenakudakwashe4mavuruAún no hay calificaciones

- Wind Market AnalysisDocumento9 páginasWind Market AnalysisRucha ShirudkarAún no hay calificaciones

- Solar Energy Au1910330 AasthagalaniDocumento15 páginasSolar Energy Au1910330 AasthagalaniAastha GalaniAún no hay calificaciones

- Market Intelligence Report: Deadline For BIS Certification of Solar Inverters Extended by Six MonthsDocumento15 páginasMarket Intelligence Report: Deadline For BIS Certification of Solar Inverters Extended by Six MonthsNavneet KaurAún no hay calificaciones

- 7.2022 - Competitive Business Model of Photovoltaic Solar Energy Installers in BrazilDocumento12 páginas7.2022 - Competitive Business Model of Photovoltaic Solar Energy Installers in BrazilWv RbAún no hay calificaciones

- Case Study: SuzlonDocumento6 páginasCase Study: SuzlonVishal BhardwajAún no hay calificaciones

- AbstractDocumento3 páginasAbstractraviAún no hay calificaciones

- WBCSD PPA IndiaDocumento17 páginasWBCSD PPA Indiasidtest kumarAún no hay calificaciones

- Corporate Profile - ReNew PowerDocumento3 páginasCorporate Profile - ReNew PowerYash SamarthAún no hay calificaciones

- 3 India 2007Documento20 páginas3 India 2007pmanikAún no hay calificaciones

- Training Report BbaDocumento51 páginasTraining Report BbaAbhijit GhoshAún no hay calificaciones

- Business Model in Electricity Industry Using Business Model Canvas Approach The Case of Pt. Xyz Ahmad Arief Wicaksono, Rizal Syarief, and Ono SuparnoDocumento12 páginasBusiness Model in Electricity Industry Using Business Model Canvas Approach The Case of Pt. Xyz Ahmad Arief Wicaksono, Rizal Syarief, and Ono SuparnoNgiroAún no hay calificaciones

- TrinaPro Solution Guide BookDocumento17 páginasTrinaPro Solution Guide BookNusrat JahanAún no hay calificaciones

- Suzlon SolutionsDocumento4 páginasSuzlon SolutionsMahendra NutakkiAún no hay calificaciones

- Ijmet: ©iaemeDocumento9 páginasIjmet: ©iaemeIAEME PublicationAún no hay calificaciones

- India Solar Rooftop Guide 2014Documento72 páginasIndia Solar Rooftop Guide 2014Sheik Syed Najmal100% (2)

- Final Report - CLSDocumento16 páginasFinal Report - CLSSadasivuni007Aún no hay calificaciones

- Applied MaterialsDocumento11 páginasApplied MaterialsMd MasoodAún no hay calificaciones

- Guidebook for Demand Aggregation: Way Forward for Rooftop Solar in IndiaDe EverandGuidebook for Demand Aggregation: Way Forward for Rooftop Solar in IndiaAún no hay calificaciones

- Business Development Plan: Model Answer SeriesDe EverandBusiness Development Plan: Model Answer SeriesCalificación: 5 de 5 estrellas5/5 (1)

- CAREC Energy Strategy 2030: Common Borders. Common Solutions. Common Energy Future.De EverandCAREC Energy Strategy 2030: Common Borders. Common Solutions. Common Energy Future.Aún no hay calificaciones

- Budget Why & HowDocumento10 páginasBudget Why & HowManisheel GautamAún no hay calificaciones

- MM III Barista E2Documento2 páginasMM III Barista E2Manisheel GautamAún no hay calificaciones

- HRM E2Documento16 páginasHRM E2Manisheel GautamAún no hay calificaciones

- Ola Cabs' Model of Competitive ExcellenceDocumento5 páginasOla Cabs' Model of Competitive ExcellenceManisheel GautamAún no hay calificaciones

- Manisheel - Consult Club ReportDocumento3 páginasManisheel - Consult Club ReportManisheel GautamAún no hay calificaciones

- Drdo Intern ReportDocumento46 páginasDrdo Intern ReportManisheel GautamAún no hay calificaciones

- Relevance of Job Description in Dynamic Business WorldDocumento12 páginasRelevance of Job Description in Dynamic Business WorldManisheel GautamAún no hay calificaciones

- Decorative Interior IncDocumento12 páginasDecorative Interior IncManisheel GautamAún no hay calificaciones

- Drdo Intern ReportDocumento46 páginasDrdo Intern ReportManisheel GautamAún no hay calificaciones

- Report Part 2Documento27 páginasReport Part 2Manisheel GautamAún no hay calificaciones

- X Inactivation Lecture (Compatibility Mode)Documento18 páginasX Inactivation Lecture (Compatibility Mode)Manisheel GautamAún no hay calificaciones

- ReportDocumento17 páginasReportManisheel GautamAún no hay calificaciones

- First Generation BiofuelsDocumento76 páginasFirst Generation BiofuelsManisheel GautamAún no hay calificaciones

- GautammanisheelDocumento1 páginaGautammanisheelManisheel GautamAún no hay calificaciones

- GrapheneDocumento2 páginasGrapheneManisheel GautamAún no hay calificaciones

- PM. Atlas Copco CompressorDocumento3 páginasPM. Atlas Copco CompressorIqmal WahabAún no hay calificaciones

- Regasification HamworthyDocumento19 páginasRegasification HamworthyMoustapha Seye100% (1)

- Catalogo Car Bur Adores Impco MASTER CATALOG-Low ResolutionDocumento608 páginasCatalogo Car Bur Adores Impco MASTER CATALOG-Low ResolutionOmar Alexander Cañon OrtegonAún no hay calificaciones

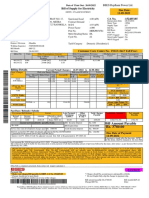

- Bill of Supply For Electricity Due Date: 12-09-2022: BSES Rajdhani Power LTDDocumento1 páginaBill of Supply For Electricity Due Date: 12-09-2022: BSES Rajdhani Power LTDNand KishorAún no hay calificaciones

- 6 Industrial Business Cases 2012Documento71 páginas6 Industrial Business Cases 2012Xavier DiazAún no hay calificaciones

- Bison Guide HCFDocumento68 páginasBison Guide HCFjohnsmith1980Aún no hay calificaciones

- List of Equipments ATDocumento1 páginaList of Equipments ATLa RocaAún no hay calificaciones

- 04 Load DispatchDocumento46 páginas04 Load Dispatchpalamwaranil100% (1)

- The Africa EnigmaDocumento10 páginasThe Africa EnigmaIMANI Center for Policy and EducationAún no hay calificaciones

- Calculadora Bonos en USD OnDocumento198 páginasCalculadora Bonos en USD OnFrann ZanczukAún no hay calificaciones

- Bosch India Corporate PresentationDocumento27 páginasBosch India Corporate PresentationRavi MishraAún no hay calificaciones

- Pump & SystemDocumento84 páginasPump & Systemabs0001Aún no hay calificaciones

- Understanding Transformer Nameplates DOBLEDocumento26 páginasUnderstanding Transformer Nameplates DOBLEsquelcheAún no hay calificaciones

- Bosch Today 2019Documento50 páginasBosch Today 2019Gogul RajaAún no hay calificaciones

- Introduction To en 16001Documento7 páginasIntroduction To en 16001IndrajeetdAún no hay calificaciones

- 3.itp ElectricalDocumento28 páginas3.itp ElectricalJoel Alcantara75% (4)

- Interest and Depreciation For Electrical Power GenerationDocumento7 páginasInterest and Depreciation For Electrical Power GenerationKopi Brisbane100% (1)

- MN - 2014 08 19Documento32 páginasMN - 2014 08 19mooraboolAún no hay calificaciones

- Blue Book 2014Documento112 páginasBlue Book 2014Charles Fernandes100% (1)

- CÁC BÀI BÁO KHOA HỌC VỀ BẢO VỆ VÀ TỰ ĐỘNG HÓA TRONG HỆ THỐNG ĐIỆNDocumento96 páginasCÁC BÀI BÁO KHOA HỌC VỀ BẢO VỆ VÀ TỰ ĐỘNG HÓA TRONG HỆ THỐNG ĐIỆNEngineeringAún no hay calificaciones

- RSE FLY PPT 062015 V 02 EN ScreenDocumento2 páginasRSE FLY PPT 062015 V 02 EN ScreenJose MustafhaAún no hay calificaciones

- VMO Contact ListDocumento1 páginaVMO Contact ListbhuvandesignAún no hay calificaciones

- EASA-TCDS-E.012 Rolls - Royce Plc. RB211 Trent 900 Series Engines-06-11122013Documento10 páginasEASA-TCDS-E.012 Rolls - Royce Plc. RB211 Trent 900 Series Engines-06-11122013Smit PatelAún no hay calificaciones

- The Cost of Wind PowerDocumento9 páginasThe Cost of Wind PowersebascianAún no hay calificaciones

- 2021 Annual ReportDocumento160 páginas2021 Annual ReportPraveen PhilipsAún no hay calificaciones

- Boletin Técnico 06 AditivoDocumento3 páginasBoletin Técnico 06 Aditivojuanmanuel_4615958Aún no hay calificaciones

- An - Intro - To - Design Thinking - EMBA 2 - 1664369569Documento20 páginasAn - Intro - To - Design Thinking - EMBA 2 - 1664369569Qazi AhmedAún no hay calificaciones

- Chapter05 - Temporary Overvoltages Analysis PDFDocumento19 páginasChapter05 - Temporary Overvoltages Analysis PDFEleazar Sierra Espinoza100% (1)

- El Sewedy Transformers (Hatem Tantawy) Presentation10 & 18 Jan 09Documento60 páginasEl Sewedy Transformers (Hatem Tantawy) Presentation10 & 18 Jan 09Lina M. Abd ElSalamAún no hay calificaciones

- Schneider Electric Gulf Provides Complete Energy SolutionsDocumento8 páginasSchneider Electric Gulf Provides Complete Energy SolutionsPMV DeptAún no hay calificaciones