También podría gustarte

- Stie Malangkuçeçwara Malang Program Pasca Sarjana Ujian Tengah SemesterDocumento13 páginasStie Malangkuçeçwara Malang Program Pasca Sarjana Ujian Tengah SemesterDwi Merry WijayantiAún no hay calificaciones

- C09 +chap+16 +Capital+Structure+-+Basic+ConceptsDocumento24 páginasC09 +chap+16 +Capital+Structure+-+Basic+Conceptsstanley tsangAún no hay calificaciones

- Resume Cost Accounting #Meeting4Documento4 páginasResume Cost Accounting #Meeting4DoniAún no hay calificaciones

- Corporate FinanceDocumento5 páginasCorporate FinancejahidkhanAún no hay calificaciones

- Dumandan, Kenneth R BSA 302-A Financial Markets P15-1Documento8 páginasDumandan, Kenneth R BSA 302-A Financial Markets P15-1Lorielyn AgoncilloAún no hay calificaciones

- Tugas Cost AccountingDocumento7 páginasTugas Cost AccountingRudy Setiawan KamadjajaAún no hay calificaciones

- Accounting Principles 7Th Canadian Edition Volume 1 by Jerry J. Weygandt, Test BankDocumento95 páginasAccounting Principles 7Th Canadian Edition Volume 1 by Jerry J. Weygandt, Test BankakasagillAún no hay calificaciones

- Many of The Expansionary Periods During The Twentieth Century Occurred During WarsDocumento1 páginaMany of The Expansionary Periods During The Twentieth Century Occurred During WarsMarisa LeeAún no hay calificaciones

- Excel As A Tool in Financial ModellingDocumento5 páginasExcel As A Tool in Financial Modellingnikita bajpaiAún no hay calificaciones

- Environmental Cost Management: Kelompok 1: Hilmy Fauzan Novia Kumala Sari Try SusantiDocumento34 páginasEnvironmental Cost Management: Kelompok 1: Hilmy Fauzan Novia Kumala Sari Try SusantiSeptian RizkyAún no hay calificaciones

- TUGASDocumento13 páginasTUGASAnas SutrinoAún no hay calificaciones

- Question 1Documento11 páginasQuestion 1Jason StevetimmyAún no hay calificaciones

- Nama: Anissa Asyahra NIM: 20.05.51.0253 Mata Kulah: Manajemen Keuangan 2 Tugas Diskusi 2 Manajemen Keuangan 2 SoalDocumento15 páginasNama: Anissa Asyahra NIM: 20.05.51.0253 Mata Kulah: Manajemen Keuangan 2 Tugas Diskusi 2 Manajemen Keuangan 2 SoalAnissa AsyahraAún no hay calificaciones

- Problem Set #1 Solution: Part 1 (Cost of Capital)Documento4 páginasProblem Set #1 Solution: Part 1 (Cost of Capital)Shirley YeungAún no hay calificaciones

- CH 03 Financial Statements ExercisesDocumento39 páginasCH 03 Financial Statements ExercisesJocelyneKarolinaArriagaRangel100% (1)

- Tugas 8 - 24Documento7 páginasTugas 8 - 24Dhany AkbarAún no hay calificaciones

- SDocumento59 páginasSmoniquettnAún no hay calificaciones

- P7Documento2 páginasP7Andreas Brown0% (1)

- B1B121009 Linda Solusi Bab 8Documento7 páginasB1B121009 Linda Solusi Bab 8Aslinda MutmainahAún no hay calificaciones

- Cash Flow Estimation and Risk Analysis: Answers To Selected End-Of-Chapter QuestionsDocumento13 páginasCash Flow Estimation and Risk Analysis: Answers To Selected End-Of-Chapter QuestionsRapitse Boitumelo Rapitse0% (1)

- Anggaran Berdasarkan Fungsi Dan AktivitasDocumento42 páginasAnggaran Berdasarkan Fungsi Dan AktivitasAri SuryadiAún no hay calificaciones

- Case5 Market - Return Variance Covariance and BetaDocumento2 páginasCase5 Market - Return Variance Covariance and BetaKhalil LaamiriAún no hay calificaciones

- Is Increasing The Entrepreneurial Orientation of A Firm Always A Good Thing. or Are There Circumstances or Environments in Which The Further Pursuit of Opportunities Can Diminish Firm Performance?Documento9 páginasIs Increasing The Entrepreneurial Orientation of A Firm Always A Good Thing. or Are There Circumstances or Environments in Which The Further Pursuit of Opportunities Can Diminish Firm Performance?anjuAún no hay calificaciones

- Excel As A Tool in Financial Modelling: Basic Excel in BriefDocumento36 páginasExcel As A Tool in Financial Modelling: Basic Excel in BriefSanyam SinghAún no hay calificaciones

- ch12 PDFDocumento9 páginasch12 PDFEmma Mariz GarciaAún no hay calificaciones

- Financial Statement Analysis ToolsDocumento32 páginasFinancial Statement Analysis ToolsYuli CandraAún no hay calificaciones

- Cma August 2013 SolutionDocumento66 páginasCma August 2013 Solutionফকির তাজুল ইসলামAún no hay calificaciones

- Opdrag: Inhandigingsdatum:: Assignment: Submission DateDocumento5 páginasOpdrag: Inhandigingsdatum:: Assignment: Submission DateVeronica NhlapoAún no hay calificaciones

- Optional ProcessDocumento1 páginaOptional ProcessFitri Yani Rossa SafiraAún no hay calificaciones

- FIN604 - HW03 - Farhan Zubair - 18164052Documento9 páginasFIN604 - HW03 - Farhan Zubair - 18164052ZAún no hay calificaciones

- Dokumen - Tips - Jawaban Soal Akmen Bab 8 PDFDocumento44 páginasDokumen - Tips - Jawaban Soal Akmen Bab 8 PDFSiswo WartoyoAún no hay calificaciones

- Role of Database As A Business ResourceDocumento1 páginaRole of Database As A Business ResourceUma Agrawal100% (1)

- Theory in Action 6.2 Dan 5.2Documento2 páginasTheory in Action 6.2 Dan 5.2zahra zhafiraAún no hay calificaciones

- Hansen AISE IM Ch04 TerjemahanDocumento57 páginasHansen AISE IM Ch04 TerjemahanDaniah Putri ArafatiahAún no hay calificaciones

- MPA703 Management Accounting Semester 2, 2019 AssignmentDocumento21 páginasMPA703 Management Accounting Semester 2, 2019 AssignmentrhagitaanggyAún no hay calificaciones

- Chương 13: LG LGDocumento6 páginasChương 13: LG LGTrinh PhanAún no hay calificaciones

- Activity On Short Run Costs and Output DecisionDocumento5 páginasActivity On Short Run Costs and Output DecisionJane ButterfieldAún no hay calificaciones

- Key IssuesDocumento11 páginasKey IssuesarifulseuAún no hay calificaciones

- Tugas Akuntansi ManajemenDocumento3 páginasTugas Akuntansi ManajemenThera MonicaAún no hay calificaciones

- Shukrullah Assignment No 2Documento4 páginasShukrullah Assignment No 2Shukrullah JanAún no hay calificaciones

- Tugas CH 9 Manajemen KeuanganDocumento5 páginasTugas CH 9 Manajemen KeuanganL RakkimanAún no hay calificaciones

- Mini CaseDocumento9 páginasMini CaseJOBIN VARGHESEAún no hay calificaciones

- Soal Asis Pert 2 - Jordy - PA1Documento1 páginaSoal Asis Pert 2 - Jordy - PA1Jordy TangAún no hay calificaciones

- Capital Structure and Financial Performance: Evidence From IndiaDocumento17 páginasCapital Structure and Financial Performance: Evidence From IndiaanirbanccimAún no hay calificaciones

- Exercises Unit 14 Qam A1Documento7 páginasExercises Unit 14 Qam A1Luis QuinonesAún no hay calificaciones

- Soal Latihan UTS Akuntansi Biaya II-NeracaDocumento3 páginasSoal Latihan UTS Akuntansi Biaya II-NeracamraliyahAún no hay calificaciones

- Chapter 2Documento40 páginasChapter 2Farapple24Aún no hay calificaciones

- Kumpulan Latihan Lab Sesi 12Documento5 páginasKumpulan Latihan Lab Sesi 12ultra oilyAún no hay calificaciones

- Ada Pharmaceutical Company Produces Three Drugs Diomycin HomycDocumento2 páginasAda Pharmaceutical Company Produces Three Drugs Diomycin HomycAmit PandeyAún no hay calificaciones

- Assignment On: Managerial Economics Mid Term and AssignmentDocumento14 páginasAssignment On: Managerial Economics Mid Term and AssignmentFaraz Khoso BalochAún no hay calificaciones

- CAS 530 SamplingDocumento14 páginasCAS 530 SamplingzelcomeiaukAún no hay calificaciones

- Mis Prelim ExamDocumento10 páginasMis Prelim ExamRonald AbletesAún no hay calificaciones

- Tugas 5 Peramalan Bisnis Tri Felbi Rayenra (19134085)Documento6 páginasTugas 5 Peramalan Bisnis Tri Felbi Rayenra (19134085)Muflih TivendoAún no hay calificaciones

- Minggu Ke - 11 - SQL - Entity Relationship ModelingDocumento44 páginasMinggu Ke - 11 - SQL - Entity Relationship ModelingKiky MelaniAún no hay calificaciones

- Chapter 2 Homework Manufacturing Economics and Computation Exercise With SolutionDocumento9 páginasChapter 2 Homework Manufacturing Economics and Computation Exercise With SolutionPhương NguyễnAún no hay calificaciones

- Bell ComputersDocumento3 páginasBell ComputersShameem Khaled0% (1)

- Kunci Jawaban Bab 5 Manajemen Biaya CompressDocumento10 páginasKunci Jawaban Bab 5 Manajemen Biaya Compressrilakkuma6Aún no hay calificaciones

- Activity 2Documento7 páginasActivity 2Mae FerrerAún no hay calificaciones

- Latihan Soal Analysis of Financial StatementDocumento7 páginasLatihan Soal Analysis of Financial StatementCaroline H24Aún no hay calificaciones

- Advance Accounting 2 by GuerreroDocumento13 páginasAdvance Accounting 2 by Guerreromarycayton100% (7)

- Chapter 10 Advance Accounting SolmanDocumento21 páginasChapter 10 Advance Accounting SolmanShiela Gumamela100% (5)

- Multiple Choice Answers and Solutions: PAR Boogie BirdieDocumento19 páginasMultiple Choice Answers and Solutions: PAR Boogie BirdieNelia Mae S. VillenaAún no hay calificaciones

- Multiple Choice Answers and Solutions: PAR Boogie BirdieDocumento19 páginasMultiple Choice Answers and Solutions: PAR Boogie BirdieNelia Mae S. VillenaAún no hay calificaciones

- Rebuilt - chapTER 08Documento6 páginasRebuilt - chapTER 08Marlon A. RodriguezAún no hay calificaciones

- 73594792314-Chapter 09Documento16 páginas73594792314-Chapter 09Marlon A. RodriguezAún no hay calificaciones

- Chapter 7 Advance Accounting Volume 1 2008Documento15 páginasChapter 7 Advance Accounting Volume 1 2008andrewhomil_17199886% (7)

- Multiple Choice Answers and Solutions: Aquino Locsin David HizonDocumento26 páginasMultiple Choice Answers and Solutions: Aquino Locsin David HizonclaudettegasendoAún no hay calificaciones

- Ok Lang AkoDocumento7 páginasOk Lang AkoMarlon A. RodriguezAún no hay calificaciones

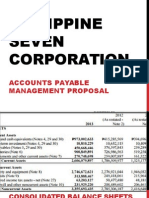

- Philippine Seven Corporation: Accounts Payable Management ProposalDocumento10 páginasPhilippine Seven Corporation: Accounts Payable Management ProposalMarlon A. RodriguezAún no hay calificaciones

- 73594792314-Chapter 09Documento16 páginas73594792314-Chapter 09Marlon A. RodriguezAún no hay calificaciones

- Chapter 02Documento25 páginasChapter 02Mendoza KlariseAún no hay calificaciones

- Chapter 1 Advanced Acctg. SolmanDocumento20 páginasChapter 1 Advanced Acctg. SolmanLaraAún no hay calificaciones

- Accounts Payable Management Proposal Philippine Seven CorporationDocumento5 páginasAccounts Payable Management Proposal Philippine Seven CorporationMarlon A. RodriguezAún no hay calificaciones

- Cost of CapitalDocumento10 páginasCost of CapitalMarlon A. RodriguezAún no hay calificaciones

- Chapter 14 - AnswerDocumento24 páginasChapter 14 - AnswerAgentSkySky100% (1)

- Interest Rates and BondsDocumento7 páginasInterest Rates and BondsMarlon A. RodriguezAún no hay calificaciones

- Time Value of MoneyDocumento7 páginasTime Value of MoneyMarlon A. RodriguezAún no hay calificaciones

- Payout Policy Elements of Payout PolicyDocumento6 páginasPayout Policy Elements of Payout PolicyMarlon A. RodriguezAún no hay calificaciones

- Installment Sales ExercisesDocumento1 páginaInstallment Sales ExercisesMarlon A. RodriguezAún no hay calificaciones

- Chapter01 - Overview of The Audit ProcessDocumento3 páginasChapter01 - Overview of The Audit ProcessCristy Estrella0% (1)

- Chapter 16 - AnswerDocumento14 páginasChapter 16 - AnswerMarlon A. RodriguezAún no hay calificaciones

- Chapter20 - AnswerDocumento7 páginasChapter20 - AnswerRicgie ManaladAún no hay calificaciones

- Chapter 5-Advance Accounting (Guerrero)Documento23 páginasChapter 5-Advance Accounting (Guerrero)Bianca Jane Maaliw63% (8)

- Multiple Choice Answers and Solutions: Aquino Locsin David HizonDocumento26 páginasMultiple Choice Answers and Solutions: Aquino Locsin David HizonclaudettegasendoAún no hay calificaciones

- Chapter01 - Overview of The Audit ProcessDocumento3 páginasChapter01 - Overview of The Audit ProcessCristy Estrella0% (1)

- Chapter 1 Advanced Acctg. SolmanDocumento20 páginasChapter 1 Advanced Acctg. SolmanLaraAún no hay calificaciones

- Chapter 02Documento25 páginasChapter 02Mendoza KlariseAún no hay calificaciones

- Chapter 1 Advanced Acctg. SolmanDocumento20 páginasChapter 1 Advanced Acctg. SolmanLaraAún no hay calificaciones

- Annex II Declaration On de MinimisDocumento5 páginasAnnex II Declaration On de MinimisȘtiri din BanatAún no hay calificaciones

- List OneDocumento7 páginasList OneLinky DooAún no hay calificaciones

- Pestleanalysis2012 Fire ServiceDocumento73 páginasPestleanalysis2012 Fire ServicePeter NavanAún no hay calificaciones

- Grupo NovEnergia, El Referente Internacional de Energía Renovable Dirigido Por Albert Mitjà Sarvisé - Sep2011Documento20 páginasGrupo NovEnergia, El Referente Internacional de Energía Renovable Dirigido Por Albert Mitjà Sarvisé - Sep2011IsabelAún no hay calificaciones

- Atlas ClubDocumento29 páginasAtlas ClubConsumatore InformatoAún no hay calificaciones

- EY Russias Downstream Sector Sights Set On Modernization PDFDocumento28 páginasEY Russias Downstream Sector Sights Set On Modernization PDFKwangsik LeeAún no hay calificaciones

- A. Using The Concept of Net Present Value and Opportunity Cost, Explain When It Is RationalDocumento2 páginasA. Using The Concept of Net Present Value and Opportunity Cost, Explain When It Is RationalLê Thành Danh100% (1)

- Saunders Notes PDFDocumento162 páginasSaunders Notes PDFJana Kryzl DibdibAún no hay calificaciones

- Pharmig 19th Annual Conference November 2011Documento8 páginasPharmig 19th Annual Conference November 2011Tim SandleAún no hay calificaciones

- New Ebook .How To Invest in Private Placement ProgramsDocumento30 páginasNew Ebook .How To Invest in Private Placement ProgramsVicente Piqueras100% (2)

- Safetec Prince ListDocumento3 páginasSafetec Prince ListGaurav MaithilAún no hay calificaciones

- Indicative and Annualized Rates On Deposits W.E .F - 01 .04.2023 To 30 .06.2023 - RateSheetDocumento4 páginasIndicative and Annualized Rates On Deposits W.E .F - 01 .04.2023 To 30 .06.2023 - RateSheetStella ShineAún no hay calificaciones

- Bretton Wood SystemDocumento17 páginasBretton Wood SystemUmesh Gaikwad0% (1)

- Case of Kyrtatos v. GreeceDocumento17 páginasCase of Kyrtatos v. GreeceIrene AlexopoulouAún no hay calificaciones

- PEST Analysis of Spain Q3 2017Documento13 páginasPEST Analysis of Spain Q3 2017mamamomiAún no hay calificaciones

- IFM Notes Full Rudramurthy SirDocumento94 páginasIFM Notes Full Rudramurthy SirSachin PatilAún no hay calificaciones

- EAIF Review 2009Documento33 páginasEAIF Review 2009Marius AngaraAún no hay calificaciones

- SP Indices Tickers ETFDocumento41 páginasSP Indices Tickers ETFBrian ClarkAún no hay calificaciones

- General: Stettin/ Ebenger Camp Topic Con Cards 1Documento39 páginasGeneral: Stettin/ Ebenger Camp Topic Con Cards 1Abraham J. FraifeldAún no hay calificaciones

- Essential of Finance Corporate Chapter 3Documento12 páginasEssential of Finance Corporate Chapter 3Linas Sutkaitis100% (1)

- Deutsche Bank Annual Report 2010 EntireDocumento498 páginasDeutsche Bank Annual Report 2010 Entirekpmgtaxshelter_kpmg tax shelter-kpmg tax shelterAún no hay calificaciones

- Chapter 9 Foreign Exchange MarketsDocumento12 páginasChapter 9 Foreign Exchange MarketsTurki AbdullahAún no hay calificaciones

- M&A of HP-Compaq With Financial ImplicationDocumento51 páginasM&A of HP-Compaq With Financial Implicationhimfu100% (1)

- Relevan CostDocumento24 páginasRelevan CostDolah ChikuAún no hay calificaciones

- S o SpotoptionDocumento8 páginasS o Spotoptionapi-165143782Aún no hay calificaciones

- Tour Highlights - Pedalling in PolandDocumento9 páginasTour Highlights - Pedalling in PolandOana SoareAún no hay calificaciones

- Speculating On Anticipated Exchange RateDocumento9 páginasSpeculating On Anticipated Exchange RatefaisalharaAún no hay calificaciones

- European Monetary IntegrationDocumento32 páginasEuropean Monetary IntegrationFlower Power100% (1)

- CEPS Activities Report 2010-2011Documento40 páginasCEPS Activities Report 2010-2011kathamailAún no hay calificaciones

- 250 Mcqs of mgt503Documento41 páginas250 Mcqs of mgt503Angel Watson0% (1)

- I Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)De EverandI Will Teach You to Be Rich: No Guilt. No Excuses. No B.S. Just a 6-Week Program That Works (Second Edition)Calificación: 4.5 de 5 estrellas4.5/5 (13)

- The Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)De EverandThe Accounting Game: Learn the Basics of Financial Accounting - As Easy as Running a Lemonade Stand (Basics for Entrepreneurs and Small Business Owners)Calificación: 4 de 5 estrellas4/5 (33)

- The Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindDe EverandThe Science of Prosperity: How to Attract Wealth, Health, and Happiness Through the Power of Your MindCalificación: 5 de 5 estrellas5/5 (231)

- Technofeudalism: What Killed CapitalismDe EverandTechnofeudalism: What Killed CapitalismCalificación: 5 de 5 estrellas5/5 (1)

- The ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!De EverandThe ZERO Percent: Secrets of the United States, the Power of Trust, Nationality, Banking and ZERO TAXES!Calificación: 4.5 de 5 estrellas4.5/5 (14)

- Purchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsDe EverandPurchasing, Inventory, and Cash Disbursements: Common Frauds and Internal ControlsCalificación: 5 de 5 estrellas5/5 (1)

- Getting to Yes: How to Negotiate Agreement Without Giving InDe EverandGetting to Yes: How to Negotiate Agreement Without Giving InCalificación: 4 de 5 estrellas4/5 (652)

- The Credit Formula: The Guide To Building and Rebuilding Lendable CreditDe EverandThe Credit Formula: The Guide To Building and Rebuilding Lendable CreditCalificación: 5 de 5 estrellas5/5 (1)

- The E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItDe EverandThe E-Myth Chief Financial Officer: Why Most Small Businesses Run Out of Money and What to Do About ItCalificación: 5 de 5 estrellas5/5 (13)

- Finance Basics (HBR 20-Minute Manager Series)De EverandFinance Basics (HBR 20-Minute Manager Series)Calificación: 4.5 de 5 estrellas4.5/5 (32)

- How to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)De EverandHow to Start a Business: Mastering Small Business, What You Need to Know to Build and Grow It, from Scratch to Launch and How to Deal With LLC Taxes and Accounting (2 in 1)Calificación: 4.5 de 5 estrellas4.5/5 (5)

- The One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyDe EverandThe One-Page Financial Plan: A Simple Way to Be Smart About Your MoneyCalificación: 4.5 de 5 estrellas4.5/5 (37)

- Accounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsDe EverandAccounting 101: From Calculating Revenues and Profits to Determining Assets and Liabilities, an Essential Guide to Accounting BasicsCalificación: 4 de 5 estrellas4/5 (7)

- LLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyDe EverandLLC Beginner's Guide: The Most Updated Guide on How to Start, Grow, and Run your Single-Member Limited Liability CompanyCalificación: 5 de 5 estrellas5/5 (1)

- Excel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetDe EverandExcel for Beginners 2023: A Step-by-Step and Quick Reference Guide to Master the Fundamentals, Formulas, Functions, & Charts in Excel with Practical Examples | A Complete Excel Shortcuts Cheat SheetAún no hay calificaciones

- Warren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageDe EverandWarren Buffett and the Interpretation of Financial Statements: The Search for the Company with a Durable Competitive AdvantageCalificación: 4.5 de 5 estrellas4.5/5 (109)

- A Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineDe EverandA Beginners Guide to QuickBooks Online 2023: A Step-by-Step Guide and Quick Reference for Small Business Owners, Churches, & Nonprofits to Track their Finances and Master QuickBooks OnlineAún no hay calificaciones

- Accounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCDe EverandAccounting For Small Businesses QuickStart Guide: Understanding Accounting For Your Sole Proprietorship, Startup, & LLCCalificación: 5 de 5 estrellas5/5 (1)

- I'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)De EverandI'll Make You an Offer You Can't Refuse: Insider Business Tips from a Former Mob Boss (NelsonFree)Calificación: 4.5 de 5 estrellas4.5/5 (24)

- Tax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesDe EverandTax-Free Wealth: How to Build Massive Wealth by Permanently Lowering Your TaxesAún no hay calificaciones

- Financial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanDe EverandFinancial Intelligence: A Manager's Guide to Knowing What the Numbers Really MeanCalificación: 4.5 de 5 estrellas4.5/5 (79)

- Overcoming Underearning(TM): A Simple Guide to a Richer LifeDe EverandOvercoming Underearning(TM): A Simple Guide to a Richer LifeCalificación: 4 de 5 estrellas4/5 (21)

- 7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelDe Everand7 Financial Models for Analysts, Investors and Finance Professionals: Theory and practical tools to help investors analyse businesses using ExcelAún no hay calificaciones