También podría gustarte

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5795)

- Pepsi BCG Matrix With ExampleDocumento2 páginasPepsi BCG Matrix With ExampleMunish PathaniaAún no hay calificaciones

- Concepts and Techniques: Data MiningDocumento54 páginasConcepts and Techniques: Data MiningMunish PathaniaAún no hay calificaciones

- MCS of InfosysDocumento7 páginasMCS of InfosysMunish PathaniaAún no hay calificaciones

- Project Presentation ON: Paper Rock PicturesDocumento18 páginasProject Presentation ON: Paper Rock PicturesMunish PathaniaAún no hay calificaciones

- Import Public Class Public Static Void NullDocumento1 páginaImport Public Class Public Static Void NullMunish PathaniaAún no hay calificaciones

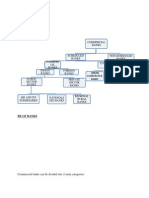

- Structure of Commercial BanksDocumento4 páginasStructure of Commercial BanksMunish PathaniaAún no hay calificaciones

- Human Resource PlanningDocumento14 páginasHuman Resource PlanningMunish Pathania50% (2)

- Presentation On Research Methodology: Coordinated By:-Anjali Amandeep Kaur Jyoti Amita Chandan SinghDocumento11 páginasPresentation On Research Methodology: Coordinated By:-Anjali Amandeep Kaur Jyoti Amita Chandan SinghMunish Pathania100% (1)

- Role of BanksDocumento2 páginasRole of BanksMunish PathaniaAún no hay calificaciones

- Functions of RbiDocumento4 páginasFunctions of RbiMunish PathaniaAún no hay calificaciones

- Hardware and Software ConceptsDocumento21 páginasHardware and Software ConceptsMunish PathaniaAún no hay calificaciones

- Project Report ON Credit RatingDocumento76 páginasProject Report ON Credit RatingMunish Pathania0% (1)

- Enterprise Resource Planning: Management Information Systems by Sahil RajDocumento11 páginasEnterprise Resource Planning: Management Information Systems by Sahil RajMunish PathaniaAún no hay calificaciones

- Perception of Customer Services Provided by Axis BankDocumento45 páginasPerception of Customer Services Provided by Axis BankMunish Pathania100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- The Basic Issue: Population Growth and The Quality of LifeDocumento44 páginasThe Basic Issue: Population Growth and The Quality of LifesaharsaeedAún no hay calificaciones

- TSLA Q4 2023 UpdateDocumento32 páginasTSLA Q4 2023 UpdateSimon AlvarezAún no hay calificaciones

- Capital Budgeting - IIDocumento16 páginasCapital Budgeting - IIVaibhav Pratap Singh BhadouriaAún no hay calificaciones

- CHAPTER 23 Performance Measurement, Compensation, and Multinational ConsiderationsDocumento32 páginasCHAPTER 23 Performance Measurement, Compensation, and Multinational ConsiderationsSierra.Aún no hay calificaciones

- LOVISA V PANDORA FINANCIAL ANALYSIS RATIODocumento30 páginasLOVISA V PANDORA FINANCIAL ANALYSIS RATIOpipahAún no hay calificaciones

- CHAPTER 2 Flexible Budget and Performance AnalysisDocumento47 páginasCHAPTER 2 Flexible Budget and Performance AnalysisNguyễn Thanh MaiAún no hay calificaciones

- IncomeTax Chapter 8Documento17 páginasIncomeTax Chapter 8Marie Frances Sayson50% (2)

- Accounting 9 DCF ModelDocumento1 páginaAccounting 9 DCF ModelRica CatanguiAún no hay calificaciones

- Fine Print Pay Stub 1Documento3 páginasFine Print Pay Stub 1api-584843897Aún no hay calificaciones

- 5capital and Revenue ConceptDocumento4 páginas5capital and Revenue ConceptRojesh BasnetAún no hay calificaciones

- Government Budget and The EconomyDocumento10 páginasGovernment Budget and The EconomyFathimaAún no hay calificaciones

- Kassahun Merawi PDFDocumento58 páginasKassahun Merawi PDFDawit WorkyeAún no hay calificaciones

- Chapter 4Documento12 páginasChapter 4jeo beduaAún no hay calificaciones

- Chetty Et Al. (2011) ,'how Does Your Kindergarten Classroom Effect Your Earnings' PDFDocumento89 páginasChetty Et Al. (2011) ,'how Does Your Kindergarten Classroom Effect Your Earnings' PDFJoe OgleAún no hay calificaciones

- FAPT2009Documento358 páginasFAPT2009zhangAún no hay calificaciones

- Chapter 007Documento143 páginasChapter 007Ganessa Roland67% (3)

- Income StatementDocumento10 páginasIncome StatementAna Valenzuela100% (1)

- Accounting HandbookDocumento42 páginasAccounting Handbookinfoyazid5Aún no hay calificaciones

- Summarized Articles On Economic Globalization, Poverty, and InequalityDocumento4 páginasSummarized Articles On Economic Globalization, Poverty, and InequalityNOOBON100% (1)

- National Income AssignmentDocumento5 páginasNational Income AssignmentSATYAM RANAAún no hay calificaciones

- Document 18Documento6 páginasDocument 18Bernadette Asuncion100% (1)

- ACC 416 Absorption Costing Vs Marginal CostingDocumento6 páginasACC 416 Absorption Costing Vs Marginal CostingNUR IZZATY ALIAH SAMIA'ANAún no hay calificaciones

- Strategic ManagementDocumento2 páginasStrategic ManagementDianna Rose VicoAún no hay calificaciones

- Analysis and Interpretation of Profitability: Operating ExpensesDocumento2 páginasAnalysis and Interpretation of Profitability: Operating ExpensesDavid Rolando García OpazoAún no hay calificaciones

- Nestle Ratio AnalysisDocumento14 páginasNestle Ratio AnalysisSaad Mehmood Qureshi0% (1)

- Business Environment Chapter 2Documento24 páginasBusiness Environment Chapter 2Muneeb SadaAún no hay calificaciones

- Ministry Business School Notes For International Business Management Unit 5 BudgetingDocumento50 páginasMinistry Business School Notes For International Business Management Unit 5 BudgetingNaresh SehdevAún no hay calificaciones

- Brgy. Clearance SampleDocumento5 páginasBrgy. Clearance SampleEdmar De Guzman Jane73% (11)

- Diagnostic Examination (Batch 2020)Documento71 páginasDiagnostic Examination (Batch 2020)KriztleKateMontealtoGelogo75% (4)

- Ultimate Financial ModelDocumento33 páginasUltimate Financial ModelTulay Farra100% (1)