También podría gustarte

- WW Idaho Power Co. - Natural Gas Plant Cooling Water Draft PermitDocumento27 páginasWW Idaho Power Co. - Natural Gas Plant Cooling Water Draft PermitMark ReinhardtAún no hay calificaciones

- Patrol LP Scenario03 July2021Documento25 páginasPatrol LP Scenario03 July2021Mark ReinhardtAún no hay calificaciones

- Patrol LP Scenario04 July2021Documento24 páginasPatrol LP Scenario04 July2021Mark ReinhardtAún no hay calificaciones

- MMCP CY2023 Idaho Blue Cross Medicaid ContractDocumento185 páginasMMCP CY2023 Idaho Blue Cross Medicaid ContractMark ReinhardtAún no hay calificaciones

- 20221230final Order No 35651Documento5 páginas20221230final Order No 35651Mark ReinhardtAún no hay calificaciones

- H0001Documento2 páginasH0001Mark ReinhardtAún no hay calificaciones

- Sustainability of Idaho's Direct Care Workforce (Idaho Office of Performance Evaluations)Documento80 páginasSustainability of Idaho's Direct Care Workforce (Idaho Office of Performance Evaluations)Mark ReinhardtAún no hay calificaciones

- A Bill: 116 Congress 2 SDocumento15 páginasA Bill: 116 Congress 2 SMark ReinhardtAún no hay calificaciones

- NIYSTXDocumento19 páginasNIYSTXMark ReinhardtAún no hay calificaciones

- Transitioning Coal Plants To Nuclear PowerDocumento43 páginasTransitioning Coal Plants To Nuclear PowerMark ReinhardtAún no hay calificaciones

- The First Rules of Los Angeles Police DepartmentDocumento1 páginaThe First Rules of Los Angeles Police DepartmentMark ReinhardtAún no hay calificaciones

- Crime Scene Manual Rev3Documento153 páginasCrime Scene Manual Rev3Mark ReinhardtAún no hay calificaciones

- 20200206press Release IPC E 18 15Documento1 página20200206press Release IPC E 18 15Mark ReinhardtAún no hay calificaciones

- A Bill: 117 Congress 1 SDocumento22 páginasA Bill: 117 Congress 1 SMark ReinhardtAún no hay calificaciones

- Affidavit Writing Made EasyDocumento6 páginasAffidavit Writing Made EasyMark ReinhardtAún no hay calificaciones

- Idaho H0098 2021 SessionDocumento4 páginasIdaho H0098 2021 SessionMark ReinhardtAún no hay calificaciones

- Bills 113s987rsDocumento44 páginasBills 113s987rsMark ReinhardtAún no hay calificaciones

- NIYSVADocumento15 páginasNIYSVAMark ReinhardtAún no hay calificaciones

- HJR003Documento1 páginaHJR003Mark ReinhardtAún no hay calificaciones

- NIYSVTDocumento4 páginasNIYSVTMark ReinhardtAún no hay calificaciones

- NIYSUTDocumento4 páginasNIYSUTMark ReinhardtAún no hay calificaciones

- City of Boise Housing Bonus Ordinance and Zoning Code Rewrite MemoDocumento11 páginasCity of Boise Housing Bonus Ordinance and Zoning Code Rewrite MemoMark ReinhardtAún no hay calificaciones

- NIYSTNDocumento5 páginasNIYSTNMark ReinhardtAún no hay calificaciones

- NIYSRIDocumento9 páginasNIYSRIMark ReinhardtAún no hay calificaciones

- NIYSPRDocumento7 páginasNIYSPRMark ReinhardtAún no hay calificaciones

- NIYSWIDocumento8 páginasNIYSWIMark ReinhardtAún no hay calificaciones

- NIYSWADocumento17 páginasNIYSWAMark ReinhardtAún no hay calificaciones

- NIYSSDDocumento4 páginasNIYSSDMark ReinhardtAún no hay calificaciones

- NIYSSCDocumento11 páginasNIYSSCMark ReinhardtAún no hay calificaciones

- NIYSPADocumento8 páginasNIYSPAMark ReinhardtAún no hay calificaciones

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- MYOB Insight For Non Profit OrganisationsDocumento33 páginasMYOB Insight For Non Profit OrganisationsztrinhAún no hay calificaciones

- Lecture 8-Sources of Funding June 2021 PerakDocumento91 páginasLecture 8-Sources of Funding June 2021 PerakKHAIRIEL IZZAT AZMANAún no hay calificaciones

- Fundamental Equity Analysis - Euro Stoxx 50 Index PDFDocumento103 páginasFundamental Equity Analysis - Euro Stoxx 50 Index PDFQ.M.S Advisors LLCAún no hay calificaciones

- MI Service Centres Address.Documento4 páginasMI Service Centres Address.sanchay3090Aún no hay calificaciones

- Bank Practice and Procedures (Acfn2113) : Prepared By: Tewodros EDocumento37 páginasBank Practice and Procedures (Acfn2113) : Prepared By: Tewodros Eመስቀል ኃይላችን ነውAún no hay calificaciones

- Extra Vocabulary: Review Units 7 & 8Documento1 páginaExtra Vocabulary: Review Units 7 & 8Karen CamposAún no hay calificaciones

- Financial InstrumentsDocumento15 páginasFinancial InstrumentsSeo NguyenAún no hay calificaciones

- Financial Accounting ADocumento137 páginasFinancial Accounting AlordAún no hay calificaciones

- BPI v. SuarezDocumento2 páginasBPI v. SuarezReymart-Vin MagulianoAún no hay calificaciones

- Basic Concepts of LoansDocumento23 páginasBasic Concepts of LoansRossel Jane CampilloAún no hay calificaciones

- EziDebit - DDR Form - CompletePTDocumento2 páginasEziDebit - DDR Form - CompletePTAndrewNeilYoungAún no hay calificaciones

- BA Interview QuestionsDocumento2 páginasBA Interview QuestionsespritologyAún no hay calificaciones

- AP AR NettingDocumento7 páginasAP AR NettingytuongAún no hay calificaciones

- Refinitiv WebinarDocumento16 páginasRefinitiv WebinarOthman SouAún no hay calificaciones

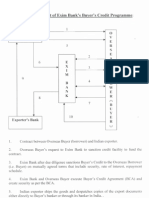

- Procedural Flow Chart of Exim BankDocumento3 páginasProcedural Flow Chart of Exim BankMilan DasAún no hay calificaciones

- Indira Awas YojanaDocumento29 páginasIndira Awas YojanaPradeep KumarAún no hay calificaciones

- Paigum ICP Invoice - ICP 237447Documento1 páginaPaigum ICP Invoice - ICP 237447sonalisabirAún no hay calificaciones

- Internship ReportDocumento13 páginasInternship ReportSuraksha Koirala50% (6)

- SAPM and FRA Prelims With Solutions 201415 PDFDocumento5 páginasSAPM and FRA Prelims With Solutions 201415 PDFPratikChalkeAún no hay calificaciones

- Chapter - I: Profile of TMB Tamilnad Mercantile Bank Limited (TMB) Is A Bank Headquartered atDocumento29 páginasChapter - I: Profile of TMB Tamilnad Mercantile Bank Limited (TMB) Is A Bank Headquartered atPoojaAún no hay calificaciones

- Dealer Application FormDocumento3 páginasDealer Application FormOsama AbouzeadAún no hay calificaciones

- FABM ProblemsDocumento1 páginaFABM ProblemsNeil Gumban40% (5)

- Standard Cipher Code American Railway 1906Documento776 páginasStandard Cipher Code American Railway 1906Max Power100% (1)

- 0452 s11 Ms 22Documento9 páginas0452 s11 Ms 22Athul TomyAún no hay calificaciones

- Final ProposalDocumento6 páginasFinal ProposalSanam_Sam_273780% (10)

- Your Combined Statement: Aisiatou Barry 10740 Guy R Brewer BLVD JAMAICA, NY 11433-2380Documento10 páginasYour Combined Statement: Aisiatou Barry 10740 Guy R Brewer BLVD JAMAICA, NY 11433-2380Ayesha ShaikhAún no hay calificaciones

- 04 - A Comprehensive Study On Financial Analysis of HDFC Bank'Documento92 páginas04 - A Comprehensive Study On Financial Analysis of HDFC Bank'Aman RoyAún no hay calificaciones

- 100 Most Important Banking Awareness QuestionsDocumento9 páginas100 Most Important Banking Awareness QuestionsKing VegetaAún no hay calificaciones

- Statement of Account: No 63 Jalan Seroja 12 Taman Seroja Bandar Baru Salak Tinggi 43900 Sepang, SelangorDocumento2 páginasStatement of Account: No 63 Jalan Seroja 12 Taman Seroja Bandar Baru Salak Tinggi 43900 Sepang, Selangorroro cocoAún no hay calificaciones

- PNB Products1Documento28 páginasPNB Products1aditi anandAún no hay calificaciones