También podría gustarte

- Cornell ComplaintDocumento41 páginasCornell Complaintjspector100% (1)

- Film Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFDocumento8 páginasFilm Tax Credit - Quarterly Report, Calendar Year 2017 2nd Quarter PDFjspectorAún no hay calificaciones

- Joseph Ruggiero Employment AgreementDocumento6 páginasJoseph Ruggiero Employment AgreementjspectorAún no hay calificaciones

- IG LetterDocumento3 páginasIG Letterjspector100% (1)

- State Health CoverageDocumento26 páginasState Health CoveragejspectorAún no hay calificaciones

- 2017 08 18 Constitution OrderDocumento27 páginas2017 08 18 Constitution OrderjspectorAún no hay calificaciones

- Pennies For Charity 2018Documento12 páginasPennies For Charity 2018ZacharyEJWilliamsAún no hay calificaciones

- Federal Budget Fiscal Year 2017 Web VersionDocumento36 páginasFederal Budget Fiscal Year 2017 Web VersionjspectorAún no hay calificaciones

- SNY0517 Crosstabs 052417Documento4 páginasSNY0517 Crosstabs 052417Nick ReismanAún no hay calificaciones

- Abo 2017 Annual ReportDocumento65 páginasAbo 2017 Annual ReportrkarlinAún no hay calificaciones

- Inflation AllowablegrowthfactorsDocumento1 páginaInflation AllowablegrowthfactorsjspectorAún no hay calificaciones

- NYSCrimeReport2016 PrelimDocumento14 páginasNYSCrimeReport2016 PrelimjspectorAún no hay calificaciones

- Opiods 2017-04-20-By Numbers Brief No8Documento17 páginasOpiods 2017-04-20-By Numbers Brief No8rkarlinAún no hay calificaciones

- Teacher Shortage Report 05232017 PDFDocumento16 páginasTeacher Shortage Report 05232017 PDFjspectorAún no hay calificaciones

- 2017 School Bfast Report Online Version 3-7-17 0Documento29 páginas2017 School Bfast Report Online Version 3-7-17 0jspectorAún no hay calificaciones

- 16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsDocumento55 páginas16 273 Amicus Brief of SF NYC and 29 Other JurisdictionsjspectorAún no hay calificaciones

- Hiffa Settlement Agreement ExecutedDocumento5 páginasHiffa Settlement Agreement ExecutedNick Reisman0% (1)

- Class of 2022Documento1 páginaClass of 2022jspectorAún no hay calificaciones

- Siena Poll March 27, 2017Documento7 páginasSiena Poll March 27, 2017jspectorAún no hay calificaciones

- Youth Cigarette and E-Cigs UseDocumento1 páginaYouth Cigarette and E-Cigs UsejspectorAún no hay calificaciones

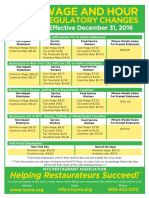

- Wage and Hour Regulatory Changes 2016Documento2 páginasWage and Hour Regulatory Changes 2016jspectorAún no hay calificaciones

- Oag Sed Letter Ice 2-27-17Documento3 páginasOag Sed Letter Ice 2-27-17BethanyAún no hay calificaciones

- Schneiderman Voter Fraud Letter 022217Documento2 páginasSchneiderman Voter Fraud Letter 022217Matthew HamiltonAún no hay calificaciones

- Darweesh Cities AmicusDocumento32 páginasDarweesh Cities AmicusjspectorAún no hay calificaciones

- 2016 Local Sales Tax CollectionsDocumento4 páginas2016 Local Sales Tax CollectionsjspectorAún no hay calificaciones

- Activity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017Documento4 páginasActivity Overview: Key Metrics Historical Sparkbars 1-2016 1-2017 YTD 2016 YTD 2017jspectorAún no hay calificaciones

- Review of Executive Budget 2017Documento102 páginasReview of Executive Budget 2017Nick ReismanAún no hay calificaciones

- p12 Budget Testimony 2-14-17Documento31 páginasp12 Budget Testimony 2-14-17jspectorAún no hay calificaciones

- Voting Report CardDocumento1 páginaVoting Report CardjspectorAún no hay calificaciones

- Pub Auth Num 2017Documento54 páginasPub Auth Num 2017jspectorAún no hay calificaciones

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (73)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2102)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)