También podría gustarte

- Health InsuranceDocumento21 páginasHealth Insuranceadhitya0% (1)

- Health InsuranceDocumento11 páginasHealth InsurancedishaAún no hay calificaciones

- Introduction to the Indian Health Insurance IndustryDocumento49 páginasIntroduction to the Indian Health Insurance Industrydaman.arneja143Aún no hay calificaciones

- Unit 2 Health Insurance ProductsDocumento25 páginasUnit 2 Health Insurance ProductsShivam YadavAún no hay calificaciones

- Health Insurance Term PaperDocumento4 páginasHealth Insurance Term Paperafdtslawm100% (1)

- MF ProjectDocumento40 páginasMF ProjectAkash ChatterjeeAún no hay calificaciones

- Consumer BehaviourDocumento10 páginasConsumer BehaviourAishwarya GharmalkarAún no hay calificaciones

- Health Insurance OverviewDocumento11 páginasHealth Insurance Overviewmansi_91Aún no hay calificaciones

- SBI General's Health Insurance Policy - Retail: Take Control of Your Family's Health. and Happiness TooDocumento2 páginasSBI General's Health Insurance Policy - Retail: Take Control of Your Family's Health. and Happiness ToobpshuAún no hay calificaciones

- Accidental InsuranceDocumento33 páginasAccidental InsuranceHarinarayan PrajapatiAún no hay calificaciones

- Introduction of Bajaj Allianz Life Insurance CompanyDocumento24 páginasIntroduction of Bajaj Allianz Life Insurance CompanyKarmesh VarshneyAún no hay calificaciones

- Analysis of Indian Insurance IndustryDocumento32 páginasAnalysis of Indian Insurance Industrymayur_rughaniAún no hay calificaciones

- Module 3Documento3 páginasModule 3khushi jaiswalAún no hay calificaciones

- Insurance Company AnalysisDocumento13 páginasInsurance Company AnalysisAyon ImtiazAún no hay calificaciones

- Why Should Health Insurance Be Given Due Consideration?Documento4 páginasWhy Should Health Insurance Be Given Due Consideration?iqbalAún no hay calificaciones

- Introduction of Bajaj Allianz Life Insurance CompanyDocumento13 páginasIntroduction of Bajaj Allianz Life Insurance CompanyGirish Lundwani60% (5)

- Sachu Bhai 1Documento14 páginasSachu Bhai 1ritishsharma290Aún no hay calificaciones

- Introduction On Insurance Fund ManagementDocumento9 páginasIntroduction On Insurance Fund Managementsawariya786Aún no hay calificaciones

- NavdeepDocumento18 páginasNavdeepSnehal LadeAún no hay calificaciones

- Macquarie FutureWiseDocumento80 páginasMacquarie FutureWiseLife Insurance AustraliaAún no hay calificaciones

- Basics of InsuranceDocumento28 páginasBasics of InsuranceSwethaAún no hay calificaciones

- INSURANCEDocumento28 páginasINSURANCEcharuAún no hay calificaciones

- About Tata AigDocumento3 páginasAbout Tata Aigsatishyadav1234Aún no hay calificaciones

- Accidental InsuranceDocumento38 páginasAccidental InsuranceSohail ShaikhAún no hay calificaciones

- Insurance & Risk ManagementDocumento8 páginasInsurance & Risk ManagementJASONM22Aún no hay calificaciones

- Find the Right Life Insurance Policy With Our Expert AgentsDocumento94 páginasFind the Right Life Insurance Policy With Our Expert AgentsSunil RawatAún no hay calificaciones

- Need For Life InsuranceDocumento9 páginasNeed For Life InsuranceDeepak NayakAún no hay calificaciones

- Irm CiaDocumento21 páginasIrm CiaMohammad HaiderAún no hay calificaciones

- Family Health Insurance GuideDocumento16 páginasFamily Health Insurance GuideHarshita DhamijaAún no hay calificaciones

- Introduction To Health InsuranceDocumento45 páginasIntroduction To Health Insurancevinayak tiwariAún no hay calificaciones

- Internship Report FinalDocumento40 páginasInternship Report FinalNeha GaiAún no hay calificaciones

- Insurance Chapter IntroductionDocumento63 páginasInsurance Chapter IntroductionMadhushreeAún no hay calificaciones

- Int Report SreeDocumento56 páginasInt Report Sreesreejithnair611Aún no hay calificaciones

- National Management College: Department of Management StudiesDocumento24 páginasNational Management College: Department of Management StudiesKarina ZetaAún no hay calificaciones

- Importance of Health Insurance in Times of Covid 19Documento110 páginasImportance of Health Insurance in Times of Covid 19Arnav Sharma100% (1)

- Health Insurance Ebook PDFDocumento29 páginasHealth Insurance Ebook PDFPrashant Pote100% (1)

- Health InsuranceDocumento28 páginasHealth InsuranceMajibul Rehman86% (7)

- Topic - Quality in HealthcareDocumento6 páginasTopic - Quality in HealthcareE-TECH SOFTWARE SOLUTIONS PVT L.T.DAún no hay calificaciones

- How To Buy Health InsuranceDocumento3 páginasHow To Buy Health InsurancekalevaishaliAún no hay calificaciones

- Group Presentation on Various Aspects of InsuranceDocumento14 páginasGroup Presentation on Various Aspects of InsuranceHimanshuAún no hay calificaciones

- Comparative Analysis of ULIP PlansDocumento106 páginasComparative Analysis of ULIP PlansJavaid Ahmad MirAún no hay calificaciones

- Insurance and Risk ManagementDocumento6 páginasInsurance and Risk ManagementSolve AssignmentAún no hay calificaciones

- Insurance ....Documento8 páginasInsurance ....SanyaAún no hay calificaciones

- Life InsuranceDocumento55 páginasLife InsuranceNehaAún no hay calificaciones

- Health Insurance Company 1Documento19 páginasHealth Insurance Company 1ankitsapkale12Aún no hay calificaciones

- US HealthcareDocumento3 páginasUS HealthcareRaghu TejaAún no hay calificaciones

- 1.1 Over View: Address: The Summit 'Level 1, Outer Ring RD, Marathahalli, Bengaluru, Karnataka 560037Documento38 páginas1.1 Over View: Address: The Summit 'Level 1, Outer Ring RD, Marathahalli, Bengaluru, Karnataka 560037Lakshmi SinghAún no hay calificaciones

- SYBBI FP ProDocumento9 páginasSYBBI FP ProSudarshan TakAún no hay calificaciones

- Comparison Between Traditional Plan &ULIP's AT ICICIDocumento70 páginasComparison Between Traditional Plan &ULIP's AT ICICIBabasab Patil (Karrisatte)100% (1)

- Himanshu Insurance and Risk Management FinalDocumento25 páginasHimanshu Insurance and Risk Management FinalHarshita DhamijaAún no hay calificaciones

- VINCENT A ROCCHI - TheGuardianLifeInsuranceCompany - Fall2011Documento30 páginasVINCENT A ROCCHI - TheGuardianLifeInsuranceCompany - Fall2011studentATtempleAún no hay calificaciones

- ICICI Prudential Life Insurance Company profileDocumento16 páginasICICI Prudential Life Insurance Company profileAnand ChavanAún no hay calificaciones

- Basic Information About LIC PoliciesDocumento6 páginasBasic Information About LIC PoliciesskumarshopperAún no hay calificaciones

- Product Diversification of LicDocumento17 páginasProduct Diversification of LicSasi KumarAún no hay calificaciones

- Life Insurance Kotak Mahindra Group Old MutualDocumento16 páginasLife Insurance Kotak Mahindra Group Old MutualKanchan khedaskerAún no hay calificaciones

- Icici Prud.Documento82 páginasIcici Prud.Rachit JoshiAún no hay calificaciones

- Insurance DefintionsDocumento6 páginasInsurance DefintionsAbbasLiaqatQureshiAún no hay calificaciones

- Employer Provided Health Insurance - EditedDocumento4 páginasEmployer Provided Health Insurance - EditedSHARMA VISHAL RAKESH 1923236Aún no hay calificaciones

- WElding GuagesDocumento16 páginasWElding Guageshasan099Aún no hay calificaciones

- ELK - 63 - 11 (AMC) Terms & ConditionsDocumento4 páginasELK - 63 - 11 (AMC) Terms & ConditionsKvvPrasadAún no hay calificaciones

- Expansion Joints NOTESDocumento21 páginasExpansion Joints NOTESKvvPrasadAún no hay calificaciones

- Hydrazine DosingDocumento2 páginasHydrazine DosingAnonymous 3HTgMDO100% (1)

- Boiling Heat TansferDocumento33 páginasBoiling Heat TansferVineet K. MishraAún no hay calificaciones

- Complete Spoken EnglishDocumento543 páginasComplete Spoken Englishjastisrinivasulu86% (64)

- Vibration Specs FFT Analyzer SetupDocumento40 páginasVibration Specs FFT Analyzer SetupHemanth Kumar83% (6)

- Hydrazine DosingDocumento2 páginasHydrazine DosingAnonymous 3HTgMDO100% (1)

- New Text DocumentDocumento1 páginaNew Text DocumentKvvPrasadAún no hay calificaciones

- Voith Coupling EngDocumento12 páginasVoith Coupling Engrikumohan100% (1)

- Boiler HouseDocumento2 páginasBoiler HouseKvvPrasadAún no hay calificaciones

- Valve Material EquivalentsDocumento3 páginasValve Material EquivalentsAndre Villegas Romero100% (1)

- Procedures For The Examination of Plans and Inspection of ConstructionDocumento43 páginasProcedures For The Examination of Plans and Inspection of ConstructionKvvPrasadAún no hay calificaciones

- 01 oilOrGreaseDocumento3 páginas01 oilOrGreaseKvvPrasadAún no hay calificaciones

- Section D2Documento249 páginasSection D2KvvPrasadAún no hay calificaciones

- Folle ToDocumento8 páginasFolle ToSaku-Jessy CamposAún no hay calificaciones

- Drum Dryer DesigningDocumento31 páginasDrum Dryer Designingkalyan555Aún no hay calificaciones

- V2.2 Summary DocumentDocumento11 páginasV2.2 Summary DocumentKvvPrasadAún no hay calificaciones

- CALC Altitude Correction SUL-13-210Documento1 páginaCALC Altitude Correction SUL-13-210KvvPrasadAún no hay calificaciones

- Gold Standard Project Timeline GuidelinesDocumento3 páginasGold Standard Project Timeline GuidelinesKvvPrasadAún no hay calificaciones

- Kis 3Documento4 páginasKis 3KvvPrasadAún no hay calificaciones

- Outcomes and Evidence Requirements: Competenz SSB Code 101571 New Zealand Qualifications Authority 2015Documento4 páginasOutcomes and Evidence Requirements: Competenz SSB Code 101571 New Zealand Qualifications Authority 2015KvvPrasadAún no hay calificaciones

- CALC Fluid Carry Over SUL 13 211Documento1 páginaCALC Fluid Carry Over SUL 13 211Francisco RenteriaAún no hay calificaciones

- Actuator Output DrivesDocumento1 páginaActuator Output DrivesKvvPrasadAún no hay calificaciones

- CP Piston CompressorsDocumento7 páginasCP Piston CompressorsKvvPrasadAún no hay calificaciones

- CALC Plant Volume SUL-13-212Documento1 páginaCALC Plant Volume SUL-13-212sauroAún no hay calificaciones

- Calc Power Cost Sul-13-213Documento1 páginaCalc Power Cost Sul-13-213KvvPrasadAún no hay calificaciones

- Assignment PDFDocumento59 páginasAssignment PDFkuththan100% (2)

- BatchPlant PerformanceDocumento1 páginaBatchPlant PerformanceKvvPrasadAún no hay calificaciones

- An Assessment of Pharm Waste in Pharm IndustriesDocumento10 páginasAn Assessment of Pharm Waste in Pharm IndustriesKvvPrasadAún no hay calificaciones

- Weekly Journal Week 2: Ms. Fairuze Chowdhury Lecturer Department of BBA in Marketing & International BusinessDocumento3 páginasWeekly Journal Week 2: Ms. Fairuze Chowdhury Lecturer Department of BBA in Marketing & International BusinessSky PunkerAún no hay calificaciones

- Ratio AnalysisDocumento11 páginasRatio Analysisbhatriyan606Aún no hay calificaciones

- Ac Exam PDF 2019 - Jan To MayDocumento99 páginasAc Exam PDF 2019 - Jan To MayRaj Bharath100% (1)

- LIC's Jeevan Dhara IIDocumento21 páginasLIC's Jeevan Dhara IIpratikwagh112002Aún no hay calificaciones

- Quiz On The Accounting EquationDocumento5 páginasQuiz On The Accounting EquationCeejay MancillaAún no hay calificaciones

- Challan 152582Documento2 páginasChallan 152582kashanAún no hay calificaciones

- Global Bikes IncDocumento8 páginasGlobal Bikes Incjai kunwarAún no hay calificaciones

- Chapter 3 - The Revised Chart of AccountsDocumento3 páginasChapter 3 - The Revised Chart of AccountsMarion LeocarioAún no hay calificaciones

- Paytm Money Limited: Combined Margin Statement For The Day: Apr 22 2021Documento1 páginaPaytm Money Limited: Combined Margin Statement For The Day: Apr 22 2021Lekkalapudi SricharanAún no hay calificaciones

- Repo Market Strategies for Funding, Arbitrage and HedgingDocumento17 páginasRepo Market Strategies for Funding, Arbitrage and HedgingJay KapadiaAún no hay calificaciones

- UTI Mutual FundDocumento77 páginasUTI Mutual FundSuman KumariAún no hay calificaciones

- Chapter 4 Admission of A PartnerDocumento10 páginasChapter 4 Admission of A PartnerHansika SahuAún no hay calificaciones

- Andrea AlciatiDocumento25 páginasAndrea AlciatisarmadfunsolAún no hay calificaciones

- FINMAN 103 Module IIIDocumento26 páginasFINMAN 103 Module IIIAlma Teresa NipaAún no hay calificaciones

- CORPORATE LIQUIDATION & ESTATE ACCOUNTING GUIDEDocumento6 páginasCORPORATE LIQUIDATION & ESTATE ACCOUNTING GUIDEJean Ysrael Marquez100% (1)

- 1.2 Defining Merchant BankingDocumento6 páginas1.2 Defining Merchant BankingGuru SwarupAún no hay calificaciones

- Capital Budgeting FMDocumento25 páginasCapital Budgeting FMAysha RiyaAún no hay calificaciones

- Business combinations overviewDocumento10 páginasBusiness combinations overviewAngelica RubiosAún no hay calificaciones

- 1 Is Madoff S Sentence Too Long 2 Some Sec PersonnelDocumento2 páginas1 Is Madoff S Sentence Too Long 2 Some Sec PersonnelAmit PandeyAún no hay calificaciones

- LRB Consulting Owned by Lennox Bronson Has A December 31 PDFDocumento1 páginaLRB Consulting Owned by Lennox Bronson Has A December 31 PDFLet's Talk With HassanAún no hay calificaciones

- Redacted Version of Exhibits A J To Letter To The Honorable Kathaleen ST J Mccormick From Edward BDocumento151 páginasRedacted Version of Exhibits A J To Letter To The Honorable Kathaleen ST J Mccormick From Edward BKdnAún no hay calificaciones

- Mergers Acquisitions and Other Restructuring Activities 7th Edition Depamphilis Test BankDocumento19 páginasMergers Acquisitions and Other Restructuring Activities 7th Edition Depamphilis Test Banksinapateprear4k100% (33)

- BAFINMAX Handout Introduction To Working Capital ManagementDocumento2 páginasBAFINMAX Handout Introduction To Working Capital ManagementDeo CoronaAún no hay calificaciones

- Senior Investment Strategist Portfolio Manager in Detroit MI Resume Clarence LewisDocumento2 páginasSenior Investment Strategist Portfolio Manager in Detroit MI Resume Clarence LewisClarenceLewisAún no hay calificaciones

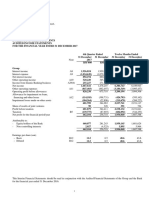

- RHB Bank Berhad 2017 Audited Financial StatementsDocumento75 páginasRHB Bank Berhad 2017 Audited Financial StatementssulizaAún no hay calificaciones

- SBT Ifsc DetailsDocumento125 páginasSBT Ifsc DetailsPanruti S Sathiyavendhan0% (1)

- Protecting Your Income Even Aer Retirement Is Assured: Aditya Birla Sun Life Insurance Vision Lifeincome PlanDocumento6 páginasProtecting Your Income Even Aer Retirement Is Assured: Aditya Birla Sun Life Insurance Vision Lifeincome PlanParmeshwar SinghAún no hay calificaciones

- Aplicatii SeminarDocumento7 páginasAplicatii SeminarAndra CarbunaruAún no hay calificaciones

- Mutual Funds Issues and Challenges-1Documento10 páginasMutual Funds Issues and Challenges-1Rohit TiwariAún no hay calificaciones

- Agrani Bank Final AssignmentDocumento81 páginasAgrani Bank Final AssignmentMojahid Johnny100% (1)