También podría gustarte

- CIMA P3 Notes - Performance Strategy - Chapter 13Documento8 páginasCIMA P3 Notes - Performance Strategy - Chapter 13Suresh Madhusanka Rodrigo50% (2)

- Cima P3 DumpsDocumento6 páginasCima P3 DumpsKatty Steve100% (1)

- CIMA P3 Notes - Performance Strategy - Chapter 8Documento6 páginasCIMA P3 Notes - Performance Strategy - Chapter 8Mark Horance Hawking100% (1)

- 01 CIMA E3 Notes - Enterprise Strategy - Chapters 1 & 2 PDFDocumento28 páginas01 CIMA E3 Notes - Enterprise Strategy - Chapters 1 & 2 PDFpiyalhassanAún no hay calificaciones

- Corporate Finance Crasher 1Documento116 páginasCorporate Finance Crasher 1Arpita PatraAún no hay calificaciones

- SCS MAY_AUG22: E3 APPLIEDDocumento61 páginasSCS MAY_AUG22: E3 APPLIEDSanjay MehrotraAún no hay calificaciones

- CIMA E3 Study Text - 2017Documento21 páginasCIMA E3 Study Text - 2017Ottone Chipara NdlelaAún no hay calificaciones

- CIMA F2 2020 NotesDocumento140 páginasCIMA F2 2020 NotesJonathan Gill100% (1)

- Cima p3 Nov201Documento28 páginasCima p3 Nov201Rony BanikAún no hay calificaciones

- Cima F2Documento1 páginaCima F2Sruthi RadhakrishnanAún no hay calificaciones

- CIMA E3 Notes - Enterprise Strategy - Chapter 4 PDFDocumento17 páginasCIMA E3 Notes - Enterprise Strategy - Chapter 4 PDFLuzuko Terence NelaniAún no hay calificaciones

- CFITS BrochureDocumento6 páginasCFITS BrochureSiddhartha GaikwadAún no hay calificaciones

- FRM N2018 Brochure SchweserDocumento8 páginasFRM N2018 Brochure SchweserYawAún no hay calificaciones

- SCS FamiliarisationDocumento26 páginasSCS FamiliarisationKAH MENG KAMAún no hay calificaciones

- Get More Past Papers FromDocumento110 páginasGet More Past Papers FromRehman Muzaffar100% (1)

- CIMA P3 - May 2012Documento130 páginasCIMA P3 - May 2012mrshami7754100% (1)

- CIMA F3 Notes - Financial Strategy - Chapter 7Documento25 páginasCIMA F3 Notes - Financial Strategy - Chapter 7Sajid AliAún no hay calificaciones

- DocumentCIMA P3 Course NotesDocumento11 páginasDocumentCIMA P3 Course Notesjony test0% (1)

- E3 Cima Workbook Q PDFDocumento54 páginasE3 Cima Workbook Q PDFgrandoverall100% (1)

- Valid F2 CIMA Braindumps - F2 Dumps PDF Exam Questions CimaDumpsDocumento9 páginasValid F2 CIMA Braindumps - F2 Dumps PDF Exam Questions CimaDumpsCarly MartinAún no hay calificaciones

- CIMA P3 Notes - Performance Strategy - Chapter 1Documento14 páginasCIMA P3 Notes - Performance Strategy - Chapter 1Mark Horance HawkingAún no hay calificaciones

- Entrepreneurship: Successfully Launching New Ventures: Feasibility AnalysisDocumento5 páginasEntrepreneurship: Successfully Launching New Ventures: Feasibility Analysisziyad albednah100% (1)

- E2 SummaryDocumento152 páginasE2 SummaryPablo Ruibal100% (1)

- R48 Derivative Markets and InstrumentsDocumento179 páginasR48 Derivative Markets and InstrumentsAaliyan Bandealy100% (1)

- CIMA P3 Notes - Chapters 1 and 2Documento27 páginasCIMA P3 Notes - Chapters 1 and 2Jon Loh Soon WengAún no hay calificaciones

- Exam and Question Tutorial Operational Case Study 2019 CIMA Professional QualificationDocumento61 páginasExam and Question Tutorial Operational Case Study 2019 CIMA Professional QualificationMyDustbin2010100% (1)

- Corporate FinanceDocumento4 páginasCorporate FinanceMogul Dodger Kevin100% (1)

- E3 Cima Workbook Q & A PDFDocumento100 páginasE3 Cima Workbook Q & A PDFJerome ChettyAún no hay calificaciones

- Citg Materials CombinedDocumento779 páginasCitg Materials CombinedHubert AnipaAún no hay calificaciones

- CIMA P3 2020 NotesDocumento96 páginasCIMA P3 2020 NotesJonathan Gill100% (2)

- CFA Preparation RecommendationsDocumento3 páginasCFA Preparation RecommendationsShynara MuzapbarovaAún no hay calificaciones

- CFA Level 2 FSADocumento3 páginasCFA Level 2 FSA素直和夫Aún no hay calificaciones

- F2 Revision SummariesDocumento97 páginasF2 Revision Summarieswakomoli100% (2)

- Astranti MCS (E, F, P Pillars)Documento331 páginasAstranti MCS (E, F, P Pillars)isuri abeykoonAún no hay calificaciones

- CFA BrochureDocumento11 páginasCFA Brochuremohammad10000Aún no hay calificaciones

- SFM QbookDocumento366 páginasSFM QbookKaran KashyapAún no hay calificaciones

- Premium Version With AnswerDocumento87 páginasPremium Version With Answermuhammad bilalAún no hay calificaciones

- Derivatives CfaDocumento3 páginasDerivatives CfavAún no hay calificaciones

- CIMA Management Case Study Analysis PDFDocumento33 páginasCIMA Management Case Study Analysis PDFAli RaziAún no hay calificaciones

- CIMA F3 Notes - Financial Strategy - Chapter 3Documento11 páginasCIMA F3 Notes - Financial Strategy - Chapter 3athancox5837100% (2)

- BPP P3 Step 6 AnswersDocumento29 páginasBPP P3 Step 6 AnswersRavi Pall100% (1)

- Concepts of Financial Management 2014Documento9 páginasConcepts of Financial Management 2014blokeyesAún no hay calificaciones

- Cima E2 NotesDocumento102 páginasCima E2 Notesbanra89Aún no hay calificaciones

- ACCA P6 (FA17) Course NotesDocumento414 páginasACCA P6 (FA17) Course NotesVinay NaiduAún no hay calificaciones

- CIMA E3 Notes - Enterprise Strategy - Chapter 3 PDFDocumento14 páginasCIMA E3 Notes - Enterprise Strategy - Chapter 3 PDFLuzuko Terence Nelani100% (1)

- CIMA P3 2019 Notes PDFDocumento132 páginasCIMA P3 2019 Notes PDFJoe BurnsAún no hay calificaciones

- 2024 l1 Topics CombinedDocumento27 páginas2024 l1 Topics CombinedShaitan LadkaAún no hay calificaciones

- CFA Level 1 - Section 2 QuantitativeDocumento81 páginasCFA Level 1 - Section 2 Quantitativeapi-376313867% (3)

- ETHICS AND PROFESSIONAL STANDARDS IN FINANCEDocumento144 páginasETHICS AND PROFESSIONAL STANDARDS IN FINANCESimran SangwanAún no hay calificaciones

- Time Saving Tips!: Wiley © 2015Documento4 páginasTime Saving Tips!: Wiley © 2015CMAún no hay calificaciones

- Cfa QaDocumento21 páginasCfa QaM Fani MalikAún no hay calificaciones

- E2 PasscardDocumento144 páginasE2 PasscardCecilia Mfene SekubuwaneAún no hay calificaciones

- eFRM CompleteDocumento5 páginaseFRM CompletePhindile MvelaseAún no hay calificaciones

- CFA Level 1Documento2 páginasCFA Level 1beta3737100% (4)

- Cima E1 Notes Organisational ManagementDocumento120 páginasCima E1 Notes Organisational ManagementLamar BrownAún no hay calificaciones

- Akin SecurityAnalysisPresentation2014 1p80bskDocumento50 páginasAkin SecurityAnalysisPresentation2014 1p80bskgarych72Aún no hay calificaciones

- Cfa Level2 ExamDocumento74 páginasCfa Level2 ExamLynn Hollenbeck BreindelAún no hay calificaciones

- Interpretation and Application of International Standards on AuditingDe EverandInterpretation and Application of International Standards on AuditingAún no hay calificaciones

- CFA Level I Exam Companion: The 7city / Wiley Study Guide to Getting the Most Out of the CFA Institute CurriculumDe EverandCFA Level I Exam Companion: The 7city / Wiley Study Guide to Getting the Most Out of the CFA Institute CurriculumAún no hay calificaciones

- CIMA P3 Notes - Performance Strategy - Chapter 1Documento14 páginasCIMA P3 Notes - Performance Strategy - Chapter 1Mark Horance HawkingAún no hay calificaciones

- Learn about random text documentDocumento1 páginaLearn about random text documentMark Horance HawkingAún no hay calificaciones

- Citation Guide - IEEE StyleDocumento6 páginasCitation Guide - IEEE StyleMark Horance HawkingAún no hay calificaciones

- My SchoolDocumento1 páginaMy SchoolSuresh Madhusanka RodrigoAún no hay calificaciones

- My School and Country With VillageDocumento1 páginaMy School and Country With VillageMark Horance HawkingAún no hay calificaciones

- My Cat Is Pet. He Is Very Innocent and Play With Me Every TimeDocumento1 páginaMy Cat Is Pet. He Is Very Innocent and Play With Me Every TimeMark Horance HawkingAún no hay calificaciones

- IHM HCI2001PanelPatternsPapDocumento3 páginasIHM HCI2001PanelPatternsPapMark Horance HawkingAún no hay calificaciones

- CEO email IDs in Android app developmentDocumento1 páginaCEO email IDs in Android app developmentIshanku BorahAún no hay calificaciones

- 7-Business Ethics & Corporate Governance.Documento15 páginas7-Business Ethics & Corporate Governance.sheetaljerryAún no hay calificaciones

- Fauji Cement PDFDocumento96 páginasFauji Cement PDFtahirAún no hay calificaciones

- King ReportDocumento254 páginasKing ReportMavy MauAún no hay calificaciones

- Shareholder Primacy, ControllingDocumento23 páginasShareholder Primacy, ControllinganonymouseAún no hay calificaciones

- Quasem Industries Limited - Annual Report 2019Documento122 páginasQuasem Industries Limited - Annual Report 2019JayedAún no hay calificaciones

- Fair Value Measurement - December 2020Documento182 páginasFair Value Measurement - December 2020HammadAún no hay calificaciones

- BAT AR20 F 2018 Financial StatementsDocumento138 páginasBAT AR20 F 2018 Financial StatementsK DonovichAún no hay calificaciones

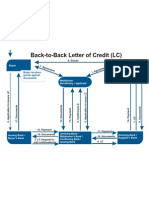

- Back To Back LCDocumento1 páginaBack To Back LCJayant Nair0% (1)

- Strategic Management: Creating Competitive Advantages: True / False QuestionsDocumento80 páginasStrategic Management: Creating Competitive Advantages: True / False QuestionsmichaelliangAún no hay calificaciones

- Hexaware Sustainability ReportDocumento72 páginasHexaware Sustainability ReportMAún no hay calificaciones

- The Failure of Corporate Governance at Infrastructure Leasing and Financial Services Limited: Lessons LearntDocumento14 páginasThe Failure of Corporate Governance at Infrastructure Leasing and Financial Services Limited: Lessons LearntGaurav GuptaAún no hay calificaciones

- HSBC Who Is The BossDocumento7 páginasHSBC Who Is The BossT FaizAún no hay calificaciones

- BMW Group Corporate GovernanceDocumento23 páginasBMW Group Corporate GovernanceAmeya Dalal0% (1)

- EASTERN SILK ANNUAL REPORTDocumento30 páginasEASTERN SILK ANNUAL REPORTNaveen KumarAún no hay calificaciones

- Business Environment and Concepts - Version 1 NotesDocumento27 páginasBusiness Environment and Concepts - Version 1 Notesaffy714Aún no hay calificaciones

- DRM Quiz2 AnswersDocumento4 páginasDRM Quiz2 Answersde4thm0ng3rAún no hay calificaciones

- Minutes of General Meeting of Shareholders TemplateDocumento5 páginasMinutes of General Meeting of Shareholders TemplatewhatevernameAún no hay calificaciones

- CH 11Documento34 páginasCH 11PetersonAún no hay calificaciones

- Maruti Udyog LTDDocumento21 páginasMaruti Udyog LTDsamyashamimAún no hay calificaciones

- Compiled Mailing List - IoT WebinarDocumento476 páginasCompiled Mailing List - IoT WebinarGirish GuptaAún no hay calificaciones

- AFM Passcard BPP PDFDocumento161 páginasAFM Passcard BPP PDFAzeez100% (1)

- Social Responsibility and Financial Performance - The Role of Good Corporate GovernanceDocumento15 páginasSocial Responsibility and Financial Performance - The Role of Good Corporate GovernanceRiyan Ramadhan100% (1)

- Derivatives Project PaperDocumento2 páginasDerivatives Project Paperirfan sururiAún no hay calificaciones

- Executive Assistant Office in Toronto Canada Resume Diane KearneyDocumento2 páginasExecutive Assistant Office in Toronto Canada Resume Diane KearneyDianeKearneyAún no hay calificaciones

- Corporate Governance and Firms Financial Performance in The United KingdomDocumento15 páginasCorporate Governance and Firms Financial Performance in The United KingdomYoung On Top BaliAún no hay calificaciones

- Strategic Case Study Paper 3.4 July 2023Documento42 páginasStrategic Case Study Paper 3.4 July 2023johny SahaAún no hay calificaciones

- WNISEF Experience in UkraineDocumento21 páginasWNISEF Experience in UkraineVitaliy HamuhaAún no hay calificaciones

- Syllabus-CORPORATE GOVERNANCEDocumento3 páginasSyllabus-CORPORATE GOVERNANCEshaleena chameriAún no hay calificaciones

- MIA Competency Framework Exposure DraftDocumento58 páginasMIA Competency Framework Exposure DraftLuqman HakimAún no hay calificaciones