También podría gustarte

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (119)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (265)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (399)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (587)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2219)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (894)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2099)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (73)

- Kyaw Soe Thein Director ASEAN Division Foreign Economic Relations Department Ministry of National Planning and Economic DevelopmentDocumento28 páginasKyaw Soe Thein Director ASEAN Division Foreign Economic Relations Department Ministry of National Planning and Economic DevelopmentMin Chan MoonAún no hay calificaciones

- 001 F 1 F 7441653639019Documento1 página001 F 1 F 7441653639019Prateeksha MishraAún no hay calificaciones

- Business Valuation of Qantas Airways LimitedDocumento4 páginasBusiness Valuation of Qantas Airways LimitedRyanAún no hay calificaciones

- Amazon Development Center India Pvt. LTD: Amount in INRDocumento1 páginaAmazon Development Center India Pvt. LTD: Amount in INRshammas PAAún no hay calificaciones

- Get Singapore e-Visa DetailsDocumento1 páginaGet Singapore e-Visa Detailsankycool100% (1)

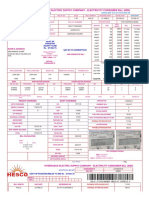

- Hyderabad Electric Supply Company - Electricity Consumer Bill (Mdi)Documento1 páginaHyderabad Electric Supply Company - Electricity Consumer Bill (Mdi)Fahad KhanAún no hay calificaciones

- 3rd Pay Committee Report 2001 (2nd Report)Documento40 páginas3rd Pay Committee Report 2001 (2nd Report)ankycoolAún no hay calificaciones

- Famous QuotesDocumento8 páginasFamous QuotesankycoolAún no hay calificaciones

- GS Strategy Evaluation and ControlDocumento45 páginasGS Strategy Evaluation and ControlankycoolAún no hay calificaciones

- Bru World CaféDocumento7 páginasBru World Caféankycool100% (1)

- Hastra: Information Technology SolutionsDocumento27 páginasHastra: Information Technology SolutionsankycoolAún no hay calificaciones

- Districts of IndiaDocumento48 páginasDistricts of IndiaankycoolAún no hay calificaciones

- Types of Foreign CapitalDocumento18 páginasTypes of Foreign Capitalankycool50% (2)

- Analysis of A Career in Investment BankingDocumento5 páginasAnalysis of A Career in Investment BankingankycoolAún no hay calificaciones

- Finshastra Mid FebDocumento18 páginasFinshastra Mid FebankycoolAún no hay calificaciones

- Regionalism V/s Multilateralism: Presented By: Anuratn Purushottam Sunita AroraDocumento22 páginasRegionalism V/s Multilateralism: Presented By: Anuratn Purushottam Sunita AroraankycoolAún no hay calificaciones

- Hastra: Information Technology SolutionsDocumento9 páginasHastra: Information Technology SolutionsankycoolAún no hay calificaciones

- Information Technology Solutions: Your Finance VocabDocumento7 páginasInformation Technology Solutions: Your Finance VocabankycoolAún no hay calificaciones

- ProtectionismDocumento10 páginasProtectionismankycoolAún no hay calificaciones

- P R A I: Information Technology in ManagementDocumento23 páginasP R A I: Information Technology in Managementankycool100% (1)

- Export MarketingDocumento5 páginasExport MarketingJeLa Cardenas-RamosAún no hay calificaciones

- Banking Industry: by Group 5: Aditya Alok Swati Sinha Abhishek Agarwal Carol KarianDocumento36 páginasBanking Industry: by Group 5: Aditya Alok Swati Sinha Abhishek Agarwal Carol KarianSwati Sinha100% (1)

- Payra Seaport - A Pathfinder To EconomyDocumento3 páginasPayra Seaport - A Pathfinder To EconomyMahadi Hasan75% (4)

- Types of Co-operative and Public Sector Banks in IndiaDocumento4 páginasTypes of Co-operative and Public Sector Banks in IndiaIMPEL Learning SolutionsAún no hay calificaciones

- 雅思 - 寫 - line graphDocumento4 páginas雅思 - 寫 - line graph陳阿醬Aún no hay calificaciones

- For Zomato Limited (Formerly Known As Zomato Private Limited and Zomato Media Private Limited)Documento1 páginaFor Zomato Limited (Formerly Known As Zomato Private Limited and Zomato Media Private Limited)Info Loaded100% (1)

- Tax Invoice: Bill ToDocumento2 páginasTax Invoice: Bill TosuthanrbAún no hay calificaciones

- Global Marketing Management: Chapter 2 Global Economic EnvironmentDocumento28 páginasGlobal Marketing Management: Chapter 2 Global Economic Environmentrameshmba100% (1)

- IMPACT of COVID-19Documento34 páginasIMPACT of COVID-19Sunny SinghAún no hay calificaciones

- IC Markets Funding InstructionsDocumento1 páginaIC Markets Funding Instructionscampur 90Aún no hay calificaciones

- Multiple Choice: Salvatore's International Economics - 12 Edition Test BankDocumento7 páginasMultiple Choice: Salvatore's International Economics - 12 Edition Test BankJuwon ParkAún no hay calificaciones

- Final Lesson Plan TradingDocumento4 páginasFinal Lesson Plan TradingBen Ritche LayosAún no hay calificaciones

- Burmese Corn Exports Rise Despite Pandemic, CoupDocumento6 páginasBurmese Corn Exports Rise Despite Pandemic, CoupSyed Muhammad Rafay AhmedAún no hay calificaciones

- The Dynamic Environment of International Trade: Mcgraw-Hill/IrwinDocumento30 páginasThe Dynamic Environment of International Trade: Mcgraw-Hill/IrwinPassant HanyAún no hay calificaciones

- 2020 Overseas Filipino WorkersDocumento6 páginas2020 Overseas Filipino Workerskilon miniAún no hay calificaciones

- Data analysis and interpretation questionsDocumento8 páginasData analysis and interpretation questionssaieswar4uAún no hay calificaciones

- Intro To Business Taxation: Group 2Documento32 páginasIntro To Business Taxation: Group 2Hardly Dare GonzalesAún no hay calificaciones

- BellonDocumento7 páginasBellonValeria Rendon NoyolaAún no hay calificaciones

- National Branding MexicoDocumento2 páginasNational Branding MexicoLauraLindarteCastroAún no hay calificaciones

- GEC 201 Lesson 2 - The Global EconomyDocumento9 páginasGEC 201 Lesson 2 - The Global EconomyReygie FabrigaAún no hay calificaciones

- 02-19 Dr. Ashfaque H. KhanDocumento32 páginas02-19 Dr. Ashfaque H. KhanBilal ZaidiAún no hay calificaciones

- Create Law SummaryDocumento2 páginasCreate Law SummaryJiza GarciaAún no hay calificaciones

- Singapore PESTLE ANALYSISDocumento7 páginasSingapore PESTLE ANALYSISmonikatatteAún no hay calificaciones

- NAFTA Reforms Mexico LawsDocumento2 páginasNAFTA Reforms Mexico LawsTere Villegas RodriguezAún no hay calificaciones

- Business & International Economy IGCSE Business NotesDocumento5 páginasBusiness & International Economy IGCSE Business NotesHiAún no hay calificaciones