También podría gustarte

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (120)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (399)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- Benefit Verification Letter: Social Security AdministrationDocumento2 páginasBenefit Verification Letter: Social Security AdministrationPeter MouldenAún no hay calificaciones

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2101)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Benefit Verification LetterMichaelPunter 1Documento4 páginasBenefit Verification LetterMichaelPunter 1DianaCarolinaCastaneda100% (1)

- Understanding MedicareDocumento4 páginasUnderstanding Medicare1224adhAún no hay calificaciones

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- Rejoice The Lord Church 681 Mckenzie ST Lewisville, TX 75057Documento6 páginasRejoice The Lord Church 681 Mckenzie ST Lewisville, TX 75057dae ChoAún no hay calificaciones

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (73)

- Benefit Verification Letter: Social Security AdministrationDocumento2 páginasBenefit Verification Letter: Social Security AdministrationNathan Rubus100% (7)

- Benefit Verification LetterDocumento4 páginasBenefit Verification LetterDonna BridgesAún no hay calificaciones

- Updated Medicare AEP Ebook 2022-2023Documento14 páginasUpdated Medicare AEP Ebook 2022-2023Sandra Amaya EscobarAún no hay calificaciones

- Authorization For Reimbursement of Interim Assistance Initial Claim or Posteligibility Case SSP 14Documento2 páginasAuthorization For Reimbursement of Interim Assistance Initial Claim or Posteligibility Case SSP 14Harry TajyarAún no hay calificaciones

- What You Need To Know: Influenza (Flu) Vaccine (Live, Intranasal)Documento2 páginasWhat You Need To Know: Influenza (Flu) Vaccine (Live, Intranasal)mpersiAún no hay calificaciones

- Polio Vaccine:: What You Need To KnowDocumento2 páginasPolio Vaccine:: What You Need To KnowmpersiAún no hay calificaciones

- Hep BDocumento2 páginasHep Bapi-435620975Aún no hay calificaciones

- Vaccine: What You Need To Know: Haemophilus Influenzae Type B (Hib)Documento2 páginasVaccine: What You Need To Know: Haemophilus Influenzae Type B (Hib)mpersiAún no hay calificaciones

- Hep ADocumento2 páginasHep AArdityaAún no hay calificaciones

- What You Need To Know: HPV (Human Papillomavirus) VaccineDocumento2 páginasWhat You Need To Know: HPV (Human Papillomavirus) VaccinempersiAún no hay calificaciones

- Clinical Significance of A High SARS-CoV-2 Viral Load in The Saliva Yoon JKorMedSci 25may2020Documento6 páginasClinical Significance of A High SARS-CoV-2 Viral Load in The Saliva Yoon JKorMedSci 25may2020mpersiAún no hay calificaciones

- Cholera Vaccine:: What You Need To KnowDocumento2 páginasCholera Vaccine:: What You Need To KnowmpersiAún no hay calificaciones

- Influenza (Flu) Vaccine (Inactivated or Recombinant) : What You Need To KnowDocumento2 páginasInfluenza (Flu) Vaccine (Inactivated or Recombinant) : What You Need To KnowereiuyereyAún no hay calificaciones

- Adenovirus Vaccine:: What You Need To KnowDocumento2 páginasAdenovirus Vaccine:: What You Need To KnowmpersiAún no hay calificaciones

- Anthrax Vaccine:: What You Need To KnowDocumento2 páginasAnthrax Vaccine:: What You Need To KnowThadAún no hay calificaciones

- Coronavirus Symptoms (COVID-19) Worldometer 31mar2020Documento10 páginasCoronavirus Symptoms (COVID-19) Worldometer 31mar2020mpersiAún no hay calificaciones

- Dtap (Diphtheria, Tetanus, Pertussis) Vaccine: What You Need To KnowDocumento2 páginasDtap (Diphtheria, Tetanus, Pertussis) Vaccine: What You Need To KnowmpersiAún no hay calificaciones

- Complement System Wiki 10may2020Documento11 páginasComplement System Wiki 10may2020mpersiAún no hay calificaciones

- Airborne Transmission of SARS-CoV-2 Klompas JAMA 04aug2020Documento2 páginasAirborne Transmission of SARS-CoV-2 Klompas JAMA 04aug2020mpersiAún no hay calificaciones

- Influ Symptoms MMWR 2001 50 (44) 984-6Documento32 páginasInflu Symptoms MMWR 2001 50 (44) 984-6mpersiAún no hay calificaciones

- Population 2012 Statistical Abstract US CensusDocumento3 páginasPopulation 2012 Statistical Abstract US CensusmpersiAún no hay calificaciones

- Brief Review On COVID-19 The 2020 Pandemic Caused by SARS-CoV-2 Valencia Cureus 24mar2020Documento14 páginasBrief Review On COVID-19 The 2020 Pandemic Caused by SARS-CoV-2 Valencia Cureus 24mar2020mpersiAún no hay calificaciones

- CD4 T Helper Cells Subsets Immunology BioRad 10may2020Documento4 páginasCD4 T Helper Cells Subsets Immunology BioRad 10may2020mpersiAún no hay calificaciones

- Characterization of SARS-CoV Spike Glycoprotein-Medicated Viral Entry Simmons PNAS 23mar2004Documento6 páginasCharacterization of SARS-CoV Spike Glycoprotein-Medicated Viral Entry Simmons PNAS 23mar2004mpersiAún no hay calificaciones

- ACE2 Molecular Bridge Between Epi Clinical Features of COVID-19 Picano CanJCard26Mar2020Documento2 páginasACE2 Molecular Bridge Between Epi Clinical Features of COVID-19 Picano CanJCard26Mar2020mpersiAún no hay calificaciones

- ACE2 at The Centre of COVID-19 From Paucisymptomatic Infections To Severe PneumoniaDocumento4 páginasACE2 at The Centre of COVID-19 From Paucisymptomatic Infections To Severe PneumoniaharyatiAún no hay calificaciones

- COVID-19 Ventilation Resources Healthcare Coalition 12may2020Documento16 páginasCOVID-19 Ventilation Resources Healthcare Coalition 12may2020mpersiAún no hay calificaciones

- Civet Wiki 08may2020Documento5 páginasCivet Wiki 08may2020mpersiAún no hay calificaciones

- Betacoronavirus Wiki 16apr2020Documento6 páginasBetacoronavirus Wiki 16apr2020mpersiAún no hay calificaciones

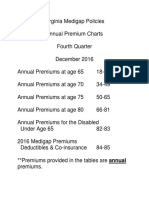

- MediGAP Charts VA 2016 30mar2017Documento70 páginasMediGAP Charts VA 2016 30mar2017mpersiAún no hay calificaciones

- Virginia Medigap Policies Premium Comparison Guide: Prepared by Commonwealth of Virginia State Corporation CommissionDocumento28 páginasVirginia Medigap Policies Premium Comparison Guide: Prepared by Commonwealth of Virginia State Corporation CommissionmpersiAún no hay calificaciones

- Complete 34434Documento6 páginasComplete 34434api-309082881Aún no hay calificaciones

- Adhdfactsheetenglish PDFDocumento1 páginaAdhdfactsheetenglish PDFLyka CorcueraAún no hay calificaciones

- Complete 34434Documento6 páginasComplete 34434api-309082881Aún no hay calificaciones

- H.B. 1725Documento24 páginasH.B. 1725Anthony WarrenAún no hay calificaciones

- 16-20 SOCIAL SECURITY NUMBER REQUIREMENT (1) - NQwjuxl (2) .pdf6502326d1291b53320Documento13 páginas16-20 SOCIAL SECURITY NUMBER REQUIREMENT (1) - NQwjuxl (2) .pdf6502326d1291b53320ElfawizzyAún no hay calificaciones

- BT 2023141Documento2 páginasBT 2023141Indiana Family to FamilyAún no hay calificaciones

- 11036Documento28 páginas11036api-309082881Aún no hay calificaciones

- Sbo - Health Insurance Rates Fy17.18Documento1 páginaSbo - Health Insurance Rates Fy17.18maria31691Aún no hay calificaciones

- 2016 Renewing Medicare Shared Savings Program ACOsDocumento27 páginas2016 Renewing Medicare Shared Savings Program ACOsiggybauAún no hay calificaciones

- Healthcare Common Procedural Coding SystemDocumento4 páginasHealthcare Common Procedural Coding SystemTherese WilliamsAún no hay calificaciones

- Medicaid and Medicare Savings Program 65+ (New York Health Access)Documento3 páginasMedicaid and Medicare Savings Program 65+ (New York Health Access)philip198Aún no hay calificaciones

- Required, They Should Be Sent To Our National Document Center at P.O. Box 258806, Oklahoma City, OK 73125-8806Documento3 páginasRequired, They Should Be Sent To Our National Document Center at P.O. Box 258806, Oklahoma City, OK 73125-8806Theo HerspergerAún no hay calificaciones

- AWI Waterfall - Back To PP - NO ECD: Screen PrintsDocumento45 páginasAWI Waterfall - Back To PP - NO ECD: Screen Printspat2abrugarAún no hay calificaciones

- COVID-19 Report 2023Documento11 páginasCOVID-19 Report 2023Donna BeardsleyAún no hay calificaciones

- Benefit Verification LetterDocumento2 páginasBenefit Verification LetterJoel PerezAún no hay calificaciones

- ICRC DSNP Issues OptionsDocumento40 páginasICRC DSNP Issues OptionsWill Blueotter AndersonAún no hay calificaciones

- Finding and Keeping A Job 2011 - Somali PDFDocumento35 páginasFinding and Keeping A Job 2011 - Somali PDFAbdirahman Ibnu AdamAún no hay calificaciones

- Medicaid Edit CodesDocumento79 páginasMedicaid Edit CodesNeil GilstrapAún no hay calificaciones

- Timely Filing Limit Guide Part 2Documento12 páginasTimely Filing Limit Guide Part 2NandhaAún no hay calificaciones

- MedicareMedicaid PDFDocumento4 páginasMedicareMedicaid PDFAlexanderAún no hay calificaciones

- En 05 10500Documento1 páginaEn 05 10500Shannon KinneyAún no hay calificaciones

- Payroll 2005Documento20 páginasPayroll 2005api-3740993Aún no hay calificaciones

- Mms Geographies Overview National Medical and Pharmacy 202201 212534 1689848522Documento30 páginasMms Geographies Overview National Medical and Pharmacy 202201 212534 1689848522Manish SinghAún no hay calificaciones

- Medicare Enrollment CodesDocumento15 páginasMedicare Enrollment CodesHarishAún no hay calificaciones

- Rule: Medicare and Medicaid: Medicare Advantage ProgramDocumento155 páginasRule: Medicare and Medicaid: Medicare Advantage ProgramJustia.comAún no hay calificaciones