También podría gustarte

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5810)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1092)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (844)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (590)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (897)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (540)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (347)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (822)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (122)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (401)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- Lehman Brothers Case StudyDocumento13 páginasLehman Brothers Case StudyIshita BansalAún no hay calificaciones

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- Advertising Agency Agreement ModelDocumento7 páginasAdvertising Agency Agreement ModelIleana MarkuAún no hay calificaciones

- Women Sample ProjectDocumento105 páginasWomen Sample ProjectIshita BansalAún no hay calificaciones

- Applicant Entrance Exam Registration Form: First Name Middle Name Last Name Date of BirthDocumento1 páginaApplicant Entrance Exam Registration Form: First Name Middle Name Last Name Date of BirthIshita BansalAún no hay calificaciones

- Project 2 Nse BseDocumento12 páginasProject 2 Nse BseIshita BansalAún no hay calificaciones

- DQM AdvanceDocumento418 páginasDQM AdvanceSubendu RakshitAún no hay calificaciones

- One Temenggong EbrochureDocumento35 páginasOne Temenggong EbrochureLester SimAún no hay calificaciones

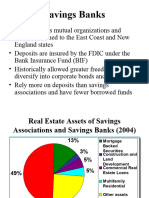

- Savings BanksDocumento7 páginasSavings BanksLara KhanAún no hay calificaciones

- Role of NABARD in Rural BankingDocumento11 páginasRole of NABARD in Rural BankingRamesh MaluAún no hay calificaciones

- Pollock An Essay On Possession in The Common Law 1888Documento268 páginasPollock An Essay On Possession in The Common Law 1888Sh0wtim3Aún no hay calificaciones

- 2013fin MS176Documento3 páginas2013fin MS176nmsusarla999Aún no hay calificaciones

- Chi Ming Tsoi Vs Court of Appeals and Gina LaoDocumento4 páginasChi Ming Tsoi Vs Court of Appeals and Gina Laocarmzy_ela24Aún no hay calificaciones

- Simple Past Tense Jack and The Beanstalk 2Documento1 páginaSimple Past Tense Jack and The Beanstalk 2pepac414100% (6)

- DOLE Citizens CharterDocumento95 páginasDOLE Citizens CharterGemmie Gabriel Punzalan-CaranayAún no hay calificaciones

- EquadorDocumento1 páginaEquadorfroggerrabbitAún no hay calificaciones

- G R - No - 190590 - July-12-2017Documento2 páginasG R - No - 190590 - July-12-2017Francis Coronel Jr.Aún no hay calificaciones

- Vdocuments - MX - Case Digests Atty CabochanDocumento38 páginasVdocuments - MX - Case Digests Atty CabochanRhuejane Gay MaquilingAún no hay calificaciones

- Interstate and Intrastate Transactions Under GSTDocumento11 páginasInterstate and Intrastate Transactions Under GSTD.Naga RajuAún no hay calificaciones

- Non-Ecumenical Caliphates: Ibn Al-Zubayr's Caliphate (684-692)Documento3 páginasNon-Ecumenical Caliphates: Ibn Al-Zubayr's Caliphate (684-692)Najah DaliAún no hay calificaciones

- Project TortsDocumento12 páginasProject Tortsharsh sahuAún no hay calificaciones

- Conan Quickstart - Changes For v3.5Documento6 páginasConan Quickstart - Changes For v3.5Antonio EleuteriAún no hay calificaciones

- Savings Account & Lockers : Terms & Conditions Apply. Kindly Contact Your Nearest Branch For Latest InformationDocumento2 páginasSavings Account & Lockers : Terms & Conditions Apply. Kindly Contact Your Nearest Branch For Latest InformationVipin KumarAún no hay calificaciones

- Lesson 4 Types of IdeologiesDocumento11 páginasLesson 4 Types of IdeologiesSir BenchAún no hay calificaciones

- GoFirst BDY6FKDocumento2 páginasGoFirst BDY6FKDhiraj PalAún no hay calificaciones

- Small BusinessDocumento16 páginasSmall Businessshivamlamba1100% (1)

- Lecture Notes Engineering Society Week 2,3Documento53 páginasLecture Notes Engineering Society Week 2,3Yousab Creator0% (1)

- PromotionsDocumento6 páginasPromotionshydexcust1Aún no hay calificaciones

- Caste or Income Based ReservationDocumento10 páginasCaste or Income Based ReservationSuvasish DasguptaAún no hay calificaciones

- Policy of InsuranceDocumento12 páginasPolicy of InsuranceClarisseAccadAún no hay calificaciones

- Acknowledgement Receipt - 20190331 - 205351Documento1 páginaAcknowledgement Receipt - 20190331 - 205351jay-ar barangay100% (1)

- Compilation in Crim Juris 09Documento206 páginasCompilation in Crim Juris 09Josephine Carbunera Dacayana-Matos100% (3)

- Magnetic Fields: What You Should Know!!!!Documento10 páginasMagnetic Fields: What You Should Know!!!!angelAún no hay calificaciones

- Psychology of GraffitiDocumento8 páginasPsychology of GraffitiMiles Kilometer CentimeterAún no hay calificaciones

- Physics II ProblemsDocumento1 páginaPhysics II ProblemsBOSS BOSSAún no hay calificaciones