También podría gustarte

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- Defensive Investor Newsletter (February 28, 2010)Documento7 páginasDefensive Investor Newsletter (February 28, 2010)Alfred AngeliciAún no hay calificaciones

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- By: Alfred L. AngeliciDocumento7 páginasBy: Alfred L. AngeliciAlfred AngeliciAún no hay calificaciones

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- Financial Freedom: A Strategy For Building Personal WealthDocumento13 páginasFinancial Freedom: A Strategy For Building Personal WealthAlfred AngeliciAún no hay calificaciones

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- Benchmarking FolliesDocumento5 páginasBenchmarking FolliesAlfred AngeliciAún no hay calificaciones

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Bs#982371 - Antipolo City Hall Oct2021Documento3 páginasBs#982371 - Antipolo City Hall Oct2021Perla EscresaAún no hay calificaciones

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- Commissioner of Customs VDocumento16 páginasCommissioner of Customs VJefferson NunezaAún no hay calificaciones

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- 26 Republic v. HeraDocumento1 página26 Republic v. HeraBasil MaguigadAún no hay calificaciones

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Income Tax Singhania Student EditionDocumento1002 páginasIncome Tax Singhania Student Editionsangita92% (13)

- Billing Address: Tax InvoiceDocumento1 páginaBilling Address: Tax InvoicePriyanka MahajanAún no hay calificaciones

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Full Download Test Bank For Health Economics and Policy 5th Edition James W Henderson Download PDF Full ChapterDocumento36 páginasFull Download Test Bank For Health Economics and Policy 5th Edition James W Henderson Download PDF Full Chapterjakraging7odbt100% (19)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

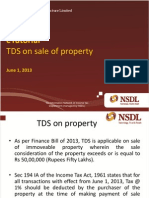

- Etutorial - TDS On PropertyDocumento20 páginasEtutorial - TDS On PropertyarunkumarsundarAún no hay calificaciones

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- R PosDocumento3 páginasR Posavinashrodrigues2002Aún no hay calificaciones

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- Global Fraud-Global Hope by Paul HellyerDocumento14 páginasGlobal Fraud-Global Hope by Paul HellyerChristopher Porter100% (1)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- 2modules 1 and 2 - Taxation 1Documento6 páginas2modules 1 and 2 - Taxation 1Gerard Relucio OroAún no hay calificaciones

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- Charitable Trusts: What Are The Advantages?Documento3 páginasCharitable Trusts: What Are The Advantages?Derek FoldsAún no hay calificaciones

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Vodafone Taxation Case StudyDocumento20 páginasVodafone Taxation Case Studygauravtu06Aún no hay calificaciones

- Yamane Vs BA Lepanto DIGESTDocumento1 páginaYamane Vs BA Lepanto DIGESTJazem Ansama100% (1)

- G.R. No. L-19707Documento6 páginasG.R. No. L-19707Jo DevisAún no hay calificaciones

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- Overview of Heads of income-MTS-2022Documento197 páginasOverview of Heads of income-MTS-2022GauravAún no hay calificaciones

- Notes To Financial Statements: Note 1 - ProfileDocumento37 páginasNotes To Financial Statements: Note 1 - ProfileKathleen Mae Amada - TorresAún no hay calificaciones

- Less: COGS: Selling Expense Administrative ExpenseDocumento13 páginasLess: COGS: Selling Expense Administrative ExpenseNAVID ANJUM KHANAún no hay calificaciones

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- 2004 Birmingham Business License CodeDocumento325 páginas2004 Birmingham Business License CodeJeffrey RobbinsAún no hay calificaciones

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- Gallagher 5e.c4Documento27 páginasGallagher 5e.c4Stacy LanierAún no hay calificaciones

- Ration Analysis of M&SDocumento72 páginasRation Analysis of M&SRashid JalalAún no hay calificaciones

- Consolidated Profit CanarabankDocumento1 páginaConsolidated Profit CanarabankMadhav LuthraAún no hay calificaciones

- 2000-DST Jan 2018 FinalDocumento3 páginas2000-DST Jan 2018 FinalClark GuilasAún no hay calificaciones

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- Promotion of Life Skills: Problem Is Something That Is Difficult To Deal With or To UnderstandDocumento55 páginasPromotion of Life Skills: Problem Is Something That Is Difficult To Deal With or To UnderstandPAMAJAAún no hay calificaciones

- Dami SB Agrinutrition ProposalDocumento14 páginasDami SB Agrinutrition ProposalGianluca LucchinAún no hay calificaciones

- CR Ma 21Documento22 páginasCR Ma 21Sharif MahmudAún no hay calificaciones

- EWT On ReimbursementDocumento3 páginasEWT On ReimbursementMonica SorianoAún no hay calificaciones

- Canada Tax SetupDocumento41 páginasCanada Tax SetupRajendran SureshAún no hay calificaciones

- Word in Season Vol. 6 - R. J. RushdoonyDocumento160 páginasWord in Season Vol. 6 - R. J. RushdoonyChalcedon Foundation100% (4)

- Declaration of Covenants & Restrictions 1977Documento14 páginasDeclaration of Covenants & Restrictions 1977PAAWS2Aún no hay calificaciones

- Philippines - OMNIBUS INVESTMENTS CODE OF 1987Documento16 páginasPhilippines - OMNIBUS INVESTMENTS CODE OF 1987sopheayem168Aún no hay calificaciones

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)