También podría gustarte

- RXR/GGV Qualified & Eligible Documents (Final 09.26.22)Documento23 páginasRXR/GGV Qualified & Eligible Documents (Final 09.26.22)RiverheadLOCALAún no hay calificaciones

- Riverhead Town Proposed Battery Energy Storage CodeDocumento10 páginasRiverhead Town Proposed Battery Energy Storage CodeRiverheadLOCALAún no hay calificaciones

- Draft Scope Riverhead Logistics CenterDocumento20 páginasDraft Scope Riverhead Logistics CenterRiverheadLOCALAún no hay calificaciones

- Riverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022Documento30 páginasRiverhead Town Board Comprehensive Plan Status Discussion Feb. 17, 2022RiverheadLOCALAún no hay calificaciones

- Yvette AguiarDocumento10 páginasYvette AguiarRiverheadLOCALAún no hay calificaciones

- 5-10-2022 Budget Hearing Presentation UpdatedDocumento12 páginas5-10-2022 Budget Hearing Presentation UpdatedRiverheadLOCALAún no hay calificaciones

- Riverhead Budget Presentation March 22, 2022Documento14 páginasRiverhead Budget Presentation March 22, 2022RiverheadLOCALAún no hay calificaciones

- Riverhead Comprehensive Plan Update Public Outreach Compendium Feb 16, 2022Documento7 páginasRiverhead Comprehensive Plan Update Public Outreach Compendium Feb 16, 2022RiverheadLOCALAún no hay calificaciones

- N.Y. Downtown Revitalization Initiative Round Five GuidebookDocumento38 páginasN.Y. Downtown Revitalization Initiative Round Five GuidebookRiverheadLOCALAún no hay calificaciones

- 2022 - 03 - 16 - EPCAL Resolution & Letter AgreementDocumento9 páginas2022 - 03 - 16 - EPCAL Resolution & Letter AgreementRiverheadLOCALAún no hay calificaciones

- AKRF Public Outreach Report AttachmentsDocumento126 páginasAKRF Public Outreach Report AttachmentsRiverheadLOCALAún no hay calificaciones

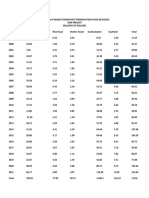

- Peconic Bay Region Community Preservation Fund Revenues 1999-2021Documento1 páginaPeconic Bay Region Community Preservation Fund Revenues 1999-2021RiverheadLOCALAún no hay calificaciones

- 2021 General Election - Suffolk County Sample Ballot BookletDocumento154 páginas2021 General Election - Suffolk County Sample Ballot BookletRiverheadLOCALAún no hay calificaciones

- Kenneth RothwellDocumento5 páginasKenneth RothwellRiverheadLOCALAún no hay calificaciones

- Pediatric Covid-19 Hospitalization ReportDocumento15 páginasPediatric Covid-19 Hospitalization ReportKevin TamponeAún no hay calificaciones

- Aguiar-Kent Campaign Finance Report 32-Day Pre GeneralDocumento2 páginasAguiar-Kent Campaign Finance Report 32-Day Pre GeneralRiverheadLOCALAún no hay calificaciones

- Catherine KentDocumento7 páginasCatherine KentRiverheadLOCALAún no hay calificaciones

- Robert E. KernDocumento3 páginasRobert E. KernRiverheadLOCALAún no hay calificaciones

- Riverhead Town Police Report, January 2021Documento6 páginasRiverhead Town Police Report, January 2021RiverheadLOCALAún no hay calificaciones

- Evelyn Hobson-Womack Campaign Finance DisclosureDocumento3 páginasEvelyn Hobson-Womack Campaign Finance DisclosureRiverheadLOCALAún no hay calificaciones

- League of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsDocumento2 páginasLeague of Women Voters of NYS 2021 Voters Guide: Ballot PropositionsRiverheadLOCAL67% (3)

- Juan Micieli-MartinezDocumento3 páginasJuan Micieli-MartinezRiverheadLOCALAún no hay calificaciones

- Riverhead Town Police Monthly Report July 2021Documento6 páginasRiverhead Town Police Monthly Report July 2021RiverheadLOCALAún no hay calificaciones

- Riverhead Town Police Report, August 2021Documento6 páginasRiverhead Town Police Report, August 2021RiverheadLOCALAún no hay calificaciones

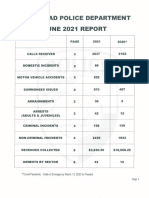

- Riverhead Town Police Monthly Report, June 2021Documento6 páginasRiverhead Town Police Monthly Report, June 2021RiverheadLOCALAún no hay calificaciones

- NYSED Health and Safety Guide For The 2021 2022 School YearDocumento21 páginasNYSED Health and Safety Guide For The 2021 2022 School YearNewsChannel 9100% (2)

- Riverhead Town Police Report, March 2021Documento6 páginasRiverhead Town Police Report, March 2021RiverheadLOCALAún no hay calificaciones

- "The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PEDocumento10 páginas"The Case of The DIsappering Landfill, or To Mine or Not To Mine" by Carl E. Fritz JR., PERiverheadLOCALAún no hay calificaciones

- Old Steeple Church Time CapsuleDocumento4 páginasOld Steeple Church Time CapsuleRiverheadLOCALAún no hay calificaciones

- Navy Environmental Concerns Survey For CalvertonDocumento3 páginasNavy Environmental Concerns Survey For CalvertonRiverheadLOCALAún no hay calificaciones

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5783)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (890)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (399)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (587)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (265)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (72)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (344)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2219)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (119)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2099)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- Session II GIRISH NADKARNI Avendus AdvisorsDocumento7 páginasSession II GIRISH NADKARNI Avendus AdvisorsGKGuideAún no hay calificaciones

- Securities and Exchange Board of India: Chapter 4 - Comprehensive Risk Management For Cash Market and Debt SegmentDocumento26 páginasSecurities and Exchange Board of India: Chapter 4 - Comprehensive Risk Management For Cash Market and Debt Segmentpradeep.jaganathanAún no hay calificaciones

- National University Syllabus Provides Detailed Finance Course OutlineDocumento9 páginasNational University Syllabus Provides Detailed Finance Course OutlineRifat Ul HaqueAún no hay calificaciones

- Golden Axis State WorldDocumento38 páginasGolden Axis State WorldChris Vlachos100% (2)

- 2020 Q 1 ReleaseDocumento4 páginas2020 Q 1 ReleasentAún no hay calificaciones

- EBA Interactive Dashboard - Q4 2019Documento13 páginasEBA Interactive Dashboard - Q4 2019staline03Aún no hay calificaciones

- Financial Markets OverviewDocumento50 páginasFinancial Markets OverviewclaytongarryAún no hay calificaciones

- Icici Bank ProjectDocumento70 páginasIcici Bank ProjectSonu Dhangar100% (2)

- Alternative InvestmentsDocumento6 páginasAlternative InvestmentsAravind MAún no hay calificaciones

- Stipulation and OrderDocumento28 páginasStipulation and OrderlegalmattersAún no hay calificaciones

- Dividend Declaration: Frequently Asked QuestionsDocumento1 páginaDividend Declaration: Frequently Asked QuestionsRhiz Jm KaelAún no hay calificaciones

- Warehouse Line of Credit Agreement - Example - Uamc & Eagle Home Mortgage and Residential Funding CorporationDocumento92 páginasWarehouse Line of Credit Agreement - Example - Uamc & Eagle Home Mortgage and Residential Funding Corporation83jjmackAún no hay calificaciones

- Introduction To Financial ManagementDocumento13 páginasIntroduction To Financial ManagementParveen Dahiya100% (1)

- Hybrid Financial InstrumentDocumento56 páginasHybrid Financial InstrumentChetan Godambe100% (5)

- Daily TradesDocumento116 páginasDaily Tradescmcnulty9Aún no hay calificaciones

- Lupin (LPC IN) : Event UpdateDocumento6 páginasLupin (LPC IN) : Event UpdateanjugaduAún no hay calificaciones

- Introduction To Financial ManagementDocumento18 páginasIntroduction To Financial Managementcopy smartAún no hay calificaciones

- DSPBRIM-Mutual Fund Basics and SIP Presentation NewDocumento45 páginasDSPBRIM-Mutual Fund Basics and SIP Presentation NewavinashmunnuAún no hay calificaciones

- MF QuestionnaireDocumento5 páginasMF QuestionnaireVINEETA KAPOORAún no hay calificaciones

- Abhijeet Power - DRHPDocumento538 páginasAbhijeet Power - DRHPsheetal_incAún no hay calificaciones

- FI - Fall 2020 - PPT Slides - IntroductionDocumento27 páginasFI - Fall 2020 - PPT Slides - IntroductionBabar MairajAún no hay calificaciones

- ESRI Investor PresentationDocumento39 páginasESRI Investor PresentationDougAún no hay calificaciones

- Balance Sheet2006Documento50 páginasBalance Sheet2006malikzai777Aún no hay calificaciones

- Sasseur Real Estate Investment Trust Prospectus Dated 21 March 2018Documento748 páginasSasseur Real Estate Investment Trust Prospectus Dated 21 March 2018David ElefantAún no hay calificaciones

- SMPG Corporate Actions Events Templates - SR2021: DisclaimerDocumento233 páginasSMPG Corporate Actions Events Templates - SR2021: Disclaimershivank tiwariAún no hay calificaciones

- Financial Markets in Korea (F)Documento167 páginasFinancial Markets in Korea (F)anonymousAún no hay calificaciones

- Permits For Energy Generation in Philippines - DOEDocumento12 páginasPermits For Energy Generation in Philippines - DOESundeep SahaAún no hay calificaciones

- DBB2104 Unit-09Documento24 páginasDBB2104 Unit-09anamikarajendran441998Aún no hay calificaciones

- Global Offering: China Tower Corporation LimitedDocumento540 páginasGlobal Offering: China Tower Corporation Limitedsilver lauAún no hay calificaciones

- ICM - Mutual Fund Distributors (Study and Reference Guide-January 2013)Documento150 páginasICM - Mutual Fund Distributors (Study and Reference Guide-January 2013)Umar Sarfraz KhanAún no hay calificaciones