También podría gustarte

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- 9 StatementOfAccount-September2023Documento3 páginas9 StatementOfAccount-September2023cailinghoneygenAún no hay calificaciones

- The Negotiable Instruments Act, 1881Documento55 páginasThe Negotiable Instruments Act, 1881meghna_mg8780% (5)

- IFRS 9 and ECL Modeling Free ClassDocumento43 páginasIFRS 9 and ECL Modeling Free ClassAbdallah Abdul JalilAún no hay calificaciones

- List of Swift MessagesDocumento50 páginasList of Swift MessageslarefisoftAún no hay calificaciones

- FRM Practice Exam From EdupristineDocumento52 páginasFRM Practice Exam From EdupristineAnish Jagdish LakhaniAún no hay calificaciones

- A 2022 YFC BMC Financials FINAL Rapal Group 1Documento7 páginasA 2022 YFC BMC Financials FINAL Rapal Group 1Rapzkie RapalAún no hay calificaciones

- Invoice KindleDocumento1 páginaInvoice KindleNishant DuggalAún no hay calificaciones

- Multinational Business Finance 14th Edition Eiteman Test BankDocumento36 páginasMultinational Business Finance 14th Edition Eiteman Test Bankrecolletfirework.i9oe100% (23)

- Surya TutoringDocumento4 páginasSurya TutoringAbhishek KumarAún no hay calificaciones

- Government and Not For Profit Accounting Concepts and Practices 6th Edition Granof Solutions ManualDocumento30 páginasGovernment and Not For Profit Accounting Concepts and Practices 6th Edition Granof Solutions ManualJessicaHardysrbxd100% (14)

- Determinants of Capital Structure in TanzaniaDocumento34 páginasDeterminants of Capital Structure in TanzaniaNtogwa Bundala100% (2)

- The Effect of Income and Earnings Management On Firm Value - Empirical Evidence From Indonesia PDFDocumento8 páginasThe Effect of Income and Earnings Management On Firm Value - Empirical Evidence From Indonesia PDFHafiz MamailaoAún no hay calificaciones

- ADM710 - Programa 2011Documento2 páginasADM710 - Programa 2011romlyslesh5736Aún no hay calificaciones

- Financial Analysis of Growth RevisedDocumento17 páginasFinancial Analysis of Growth ReviseddebmatraAún no hay calificaciones

- Ifii 2017Documento53 páginasIfii 2017Gracellyn AlexaAún no hay calificaciones

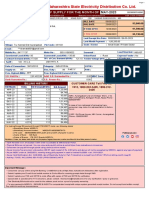

- Bill 670 502039075170 202305Documento5 páginasBill 670 502039075170 202305pravin ghatgeAún no hay calificaciones

- Working Paper Egrement Ika SalinanDocumento1 páginaWorking Paper Egrement Ika Salinanfc BundaAún no hay calificaciones

- Form-1770-Attachment IVDocumento2 páginasForm-1770-Attachment IVrover2010Aún no hay calificaciones

- Chapter 21 SolutionsDocumento3 páginasChapter 21 SolutionsLiana LianaAún no hay calificaciones

- Inflation in Pakistan Economics ReportDocumento15 páginasInflation in Pakistan Economics ReportQanitaZakir75% (16)

- Prospects OF Venturecapital in India: Presented By: Shweta Gupta 10MBA 32Documento21 páginasProspects OF Venturecapital in India: Presented By: Shweta Gupta 10MBA 32shwetajiiAún no hay calificaciones

- 04 Task Performance 1Documento4 páginas04 Task Performance 1Kim JessiAún no hay calificaciones

- 349191compund Intrest Sheet-3 - CrwillDocumento9 páginas349191compund Intrest Sheet-3 - Crwillmadhuknl8674Aún no hay calificaciones

- Form No.15hDocumento2 páginasForm No.15hAmit BhatiAún no hay calificaciones

- Lobj18 0007008 Question Bank of AccountingDocumento223 páginasLobj18 0007008 Question Bank of AccountingMỹ NhiAún no hay calificaciones

- Forign Currency TransactionDocumento31 páginasForign Currency Transactionnik22ydAún no hay calificaciones

- Accounting For ManagersDocumento14 páginasAccounting For ManagersKabo Lucas67% (3)

- Measuring and Evaluating Financial PerformanceDocumento12 páginasMeasuring and Evaluating Financial PerformanceNishtha SisodiaAún no hay calificaciones

- Chapter 1 - Indian Financial System - IntroductionDocumento26 páginasChapter 1 - Indian Financial System - IntroductionsejalAún no hay calificaciones

- First Optima Realty Corporation vs. Securitron Security Services, Inc., 748 SCRA 534, January 28, 2015Documento20 páginasFirst Optima Realty Corporation vs. Securitron Security Services, Inc., 748 SCRA 534, January 28, 2015Mark ReyesAún no hay calificaciones