También podría gustarte

- Gov Acc Assignment JohnDocumento5 páginasGov Acc Assignment JohnArvin Glen BeltranAún no hay calificaciones

- Toa 34a-3Documento1 páginaToa 34a-3Arvin Glen BeltranAún no hay calificaciones

- Background InfoDocumento1 páginaBackground InfoArvin Glen BeltranAún no hay calificaciones

- Sec 30-50 (Negotiation)Documento10 páginasSec 30-50 (Negotiation)Arvin Glen BeltranAún no hay calificaciones

- Sec 7, 8, 9Documento2 páginasSec 7, 8, 9Arvin Glen BeltranAún no hay calificaciones

- Acc 5 Course OutlineDocumento7 páginasAcc 5 Course OutlineArvin Glen BeltranAún no hay calificaciones

- Sec 5,6, 11-13Documento3 páginasSec 5,6, 11-13Arvin Glen BeltranAún no hay calificaciones

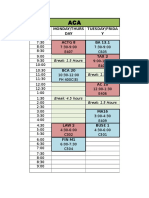

- Break: 1.5 Hours Break: 1.5 Hours Break: 1.5 Hours Break: 1.5 HoursDocumento1 páginaBreak: 1.5 Hours Break: 1.5 Hours Break: 1.5 Hours Break: 1.5 HoursArvin Glen BeltranAún no hay calificaciones

- 3rd Year ScheduleDocumento2 páginas3rd Year ScheduleArvin Glen BeltranAún no hay calificaciones

- Juan Clyne A. Pray Jcba Company Corrales Avenue, Cagayan de Oro City Misamis Oriental, 9000Documento6 páginasJuan Clyne A. Pray Jcba Company Corrales Avenue, Cagayan de Oro City Misamis Oriental, 9000Arvin Glen BeltranAún no hay calificaciones

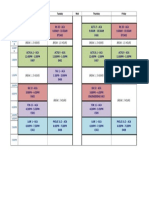

- Time Monday/Thurs DAY Tuesday/Frida Y Actg 8 BA 13.1: Break: 1.5 HoursDocumento3 páginasTime Monday/Thurs DAY Tuesday/Frida Y Actg 8 BA 13.1: Break: 1.5 HoursArvin Glen BeltranAún no hay calificaciones

- De Los Santos vs. de La Cruz (Beltran & Mauna)Documento2 páginasDe Los Santos vs. de La Cruz (Beltran & Mauna)Arvin Glen BeltranAún no hay calificaciones

- Infinity Ex Canon Rock Intermediate Sheetmusic Trade ComDocumento3 páginasInfinity Ex Canon Rock Intermediate Sheetmusic Trade ComivyAún no hay calificaciones

- Teachers, Take A Bow: By: Arvin Glen B. Beltran of 4-VizDocumento1 páginaTeachers, Take A Bow: By: Arvin Glen B. Beltran of 4-VizArvin Glen BeltranAún no hay calificaciones

- Law OutlineDocumento11 páginasLaw OutlineArvin Glen BeltranAún no hay calificaciones

- NBA 2K16 Keyboard MappingDocumento1 páginaNBA 2K16 Keyboard MappingArvin Glen BeltranAún no hay calificaciones

- SilverStrand by The Corrs PDFDocumento1 páginaSilverStrand by The Corrs PDFArvin Glen Beltran100% (1)

- Hidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceDe EverandHidden Figures: The American Dream and the Untold Story of the Black Women Mathematicians Who Helped Win the Space RaceCalificación: 4 de 5 estrellas4/5 (895)

- The Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeDe EverandThe Subtle Art of Not Giving a F*ck: A Counterintuitive Approach to Living a Good LifeCalificación: 4 de 5 estrellas4/5 (5794)

- Shoe Dog: A Memoir by the Creator of NikeDe EverandShoe Dog: A Memoir by the Creator of NikeCalificación: 4.5 de 5 estrellas4.5/5 (537)

- Grit: The Power of Passion and PerseveranceDe EverandGrit: The Power of Passion and PerseveranceCalificación: 4 de 5 estrellas4/5 (588)

- The Yellow House: A Memoir (2019 National Book Award Winner)De EverandThe Yellow House: A Memoir (2019 National Book Award Winner)Calificación: 4 de 5 estrellas4/5 (98)

- The Little Book of Hygge: Danish Secrets to Happy LivingDe EverandThe Little Book of Hygge: Danish Secrets to Happy LivingCalificación: 3.5 de 5 estrellas3.5/5 (400)

- Never Split the Difference: Negotiating As If Your Life Depended On ItDe EverandNever Split the Difference: Negotiating As If Your Life Depended On ItCalificación: 4.5 de 5 estrellas4.5/5 (838)

- Elon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureDe EverandElon Musk: Tesla, SpaceX, and the Quest for a Fantastic FutureCalificación: 4.5 de 5 estrellas4.5/5 (474)

- A Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryDe EverandA Heartbreaking Work Of Staggering Genius: A Memoir Based on a True StoryCalificación: 3.5 de 5 estrellas3.5/5 (231)

- Rise of ISIS: A Threat We Can't IgnoreDe EverandRise of ISIS: A Threat We Can't IgnoreCalificación: 3.5 de 5 estrellas3.5/5 (137)

- The Emperor of All Maladies: A Biography of CancerDe EverandThe Emperor of All Maladies: A Biography of CancerCalificación: 4.5 de 5 estrellas4.5/5 (271)

- Devil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaDe EverandDevil in the Grove: Thurgood Marshall, the Groveland Boys, and the Dawn of a New AmericaCalificación: 4.5 de 5 estrellas4.5/5 (266)

- The Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersDe EverandThe Hard Thing About Hard Things: Building a Business When There Are No Easy AnswersCalificación: 4.5 de 5 estrellas4.5/5 (345)

- On Fire: The (Burning) Case for a Green New DealDe EverandOn Fire: The (Burning) Case for a Green New DealCalificación: 4 de 5 estrellas4/5 (74)

- The World Is Flat 3.0: A Brief History of the Twenty-first CenturyDe EverandThe World Is Flat 3.0: A Brief History of the Twenty-first CenturyCalificación: 3.5 de 5 estrellas3.5/5 (2259)

- Team of Rivals: The Political Genius of Abraham LincolnDe EverandTeam of Rivals: The Political Genius of Abraham LincolnCalificación: 4.5 de 5 estrellas4.5/5 (234)

- The Unwinding: An Inner History of the New AmericaDe EverandThe Unwinding: An Inner History of the New AmericaCalificación: 4 de 5 estrellas4/5 (45)

- The Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreDe EverandThe Gifts of Imperfection: Let Go of Who You Think You're Supposed to Be and Embrace Who You AreCalificación: 4 de 5 estrellas4/5 (1090)

- The Sympathizer: A Novel (Pulitzer Prize for Fiction)De EverandThe Sympathizer: A Novel (Pulitzer Prize for Fiction)Calificación: 4.5 de 5 estrellas4.5/5 (121)

- The Perks of Being a WallflowerDe EverandThe Perks of Being a WallflowerCalificación: 4.5 de 5 estrellas4.5/5 (2104)

- Her Body and Other Parties: StoriesDe EverandHer Body and Other Parties: StoriesCalificación: 4 de 5 estrellas4/5 (821)