También podría gustarte

- Goods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesDe EverandGoods and Services Tax (GST) Filing Made Easy: Free Software Literacy SeriesAún no hay calificaciones

- Filing of Form 15G Form 15H An AnalysisDocumento5 páginasFiling of Form 15G Form 15H An AnalysisRPNAún no hay calificaciones

- 1040 Exam Prep Module V: Adjustments to Income or DeductionsDe Everand1040 Exam Prep Module V: Adjustments to Income or DeductionsAún no hay calificaciones

- The List of Documents Required For PF and ESI Registration Is Given BelowDocumento63 páginasThe List of Documents Required For PF and ESI Registration Is Given BelowManjinder SinghAún no hay calificaciones

- The Trump Tax Cut: Your Personal Guide to the New Tax LawDe EverandThe Trump Tax Cut: Your Personal Guide to the New Tax LawAún no hay calificaciones

- TDS Intrest IncomeDocumento3 páginasTDS Intrest Incomekashyap_ajAún no hay calificaciones

- Thrift Savings Plan Investor's Handbook for Federal EmployeesDe EverandThrift Savings Plan Investor's Handbook for Federal EmployeesAún no hay calificaciones

- Details For TDS On PF Withdrawal - UAN BasedDocumento3 páginasDetails For TDS On PF Withdrawal - UAN BasedGuru PrasannaAún no hay calificaciones

- 1040 Exam Prep: Module I: The Form 1040 FormulaDe Everand1040 Exam Prep: Module I: The Form 1040 FormulaCalificación: 1 de 5 estrellas1/5 (3)

- Form 15G To Avoid TDS Deduction - Taxguru - inDocumento4 páginasForm 15G To Avoid TDS Deduction - Taxguru - inwhitefieldAún no hay calificaciones

- 1040 Exam Prep: Module II - Basic Tax ConceptsDe Everand1040 Exam Prep: Module II - Basic Tax ConceptsCalificación: 1.5 de 5 estrellas1.5/5 (2)

- Income Slabs Income Tax RateDocumento4 páginasIncome Slabs Income Tax RateSavoir PenAún no hay calificaciones

- GauriDocumento12 páginasGauriRahul MittalAún no hay calificaciones

- Employee's Provident Fund (EPF)Documento2 páginasEmployee's Provident Fund (EPF)rajendra kumarAún no hay calificaciones

- Employees' Provident Fund Scheme: (0.18 %)Documento9 páginasEmployees' Provident Fund Scheme: (0.18 %)Shubhabrata BanerjeeAún no hay calificaciones

- Employee Communication On PF WithdrawalDocumento1 páginaEmployee Communication On PF WithdrawalchaitanyaAún no hay calificaciones

- GST AmendmentDocumento14 páginasGST Amendmentbcomh2103012Aún no hay calificaciones

- Employee Provident Fund (Epf)Documento8 páginasEmployee Provident Fund (Epf)Astha AhujaAún no hay calificaciones

- Guide To Understanding Form 16: Structure and Parts of Form 16 - A Form-16 Part A/Traces Form-16Documento5 páginasGuide To Understanding Form 16: Structure and Parts of Form 16 - A Form-16 Part A/Traces Form-16Priya AnandAún no hay calificaciones

- Contribution Rate Employee (12%)Documento4 páginasContribution Rate Employee (12%)Kiran MettuAún no hay calificaciones

- Taxation Notes 4.1.23 MidtermDocumento11 páginasTaxation Notes 4.1.23 MidtermRaissa Anjela Carman-JardenicoAún no hay calificaciones

- Statutory Compliance - PF and GratuityDocumento11 páginasStatutory Compliance - PF and GratuityHusna SadiyaAún no hay calificaciones

- By Shoba Kanakraj: Mstu, ChennaiDocumento20 páginasBy Shoba Kanakraj: Mstu, ChennaiVasanthAún no hay calificaciones

- FAQ On Form 16 & ITR Submission: Q. What Is Form 16?Documento4 páginasFAQ On Form 16 & ITR Submission: Q. What Is Form 16?n333aroraAún no hay calificaciones

- Artifact 5a - Guidelines For Filling PF Withdrawal Form TCSDocumento3 páginasArtifact 5a - Guidelines For Filling PF Withdrawal Form TCSAmy Brady100% (3)

- TDS & TCSDocumento107 páginasTDS & TCSSANDEEP CHAUREAún no hay calificaciones

- Taxability of Provident FundDocumento3 páginasTaxability of Provident FundRupen ChawlaAún no hay calificaciones

- A Simple Guide To Resolve Your Rejected GST Registration ApplicationDocumento6 páginasA Simple Guide To Resolve Your Rejected GST Registration ApplicationRam ADCAAún no hay calificaciones

- Income From Other SourcesDocumento27 páginasIncome From Other Sourcesanilchavan100% (1)

- Overview of TDS: by C.A. Manish JathliyaDocumento21 páginasOverview of TDS: by C.A. Manish JathliyaHasan Babu KothaAún no hay calificaciones

- GST NotesDocumento39 páginasGST NotesCrick CompactAún no hay calificaciones

- Union Budget 2015 AnalysisDocumento10 páginasUnion Budget 2015 Analysisvenkatesh_financeAún no hay calificaciones

- Amendments in Income Tax Act: Submitted To-Prof. Atul KochharDocumento11 páginasAmendments in Income Tax Act: Submitted To-Prof. Atul KochharKUNAL GUPTAAún no hay calificaciones

- Compliance Under Labour Laws: Presented By: RSPH & Associates CA Hitesh Agrawal Baroda. (O) 02652342932/33 (M) 9998028737Documento57 páginasCompliance Under Labour Laws: Presented By: RSPH & Associates CA Hitesh Agrawal Baroda. (O) 02652342932/33 (M) 9998028737Himanshu ShahAún no hay calificaciones

- 15gh TC - DocumentDocumento2 páginas15gh TC - Documentvighnarthaagency2255Aún no hay calificaciones

- TAMIL NADU GOVERNMENT - CONTRIBUTORY PENSION SCHEME - FAQsDocumento4 páginasTAMIL NADU GOVERNMENT - CONTRIBUTORY PENSION SCHEME - FAQsDr.Sagindar100% (1)

- Terminal Benefit - Nilam ShahDocumento24 páginasTerminal Benefit - Nilam ShahRaghava NarayanaAún no hay calificaciones

- Chapter 4 Income From Salaries: (Sec.15 To 17)Documento32 páginasChapter 4 Income From Salaries: (Sec.15 To 17)kiranshingoteAún no hay calificaciones

- Form 15G & 15H: Save Tds On Interest On FdsDocumento6 páginasForm 15G & 15H: Save Tds On Interest On FdsShreekumarAún no hay calificaciones

- 67.calculation of Relief Under Sections 89 89ADocumento5 páginas67.calculation of Relief Under Sections 89 89ARaghu SNAún no hay calificaciones

- Casual Taxable Person Under GSTDocumento3 páginasCasual Taxable Person Under GSTFiling BuddyAún no hay calificaciones

- Chapter 4 Income From Salaries: (Sec.15 To 17)Documento32 páginasChapter 4 Income From Salaries: (Sec.15 To 17)kiranshingoteAún no hay calificaciones

- P.P.T On Duties - Responsibilities of DDO For GSTDocumento30 páginasP.P.T On Duties - Responsibilities of DDO For GSTBilal A BarbhuiyaAún no hay calificaciones

- Taxiation AssignmentDocumento9 páginasTaxiation AssignmentNoman AreebAún no hay calificaciones

- Provident Fund Act SummaryDocumento10 páginasProvident Fund Act SummaryhemlatauAún no hay calificaciones

- Field Training Report 127411Documento7 páginasField Training Report 127411deepak mauryaAún no hay calificaciones

- Provident Fund - All You Need To KnowDocumento10 páginasProvident Fund - All You Need To KnowBabita SinghAún no hay calificaciones

- State Bank of Patiala Balance Sheet Department Welcomes Participants To SeminarDocumento19 páginasState Bank of Patiala Balance Sheet Department Welcomes Participants To SeminarKunal ParmarAún no hay calificaciones

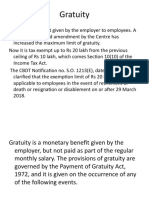

- GratuatyDocumento9 páginasGratuatyAlezAún no hay calificaciones

- Chapter 4 Income From Salaries: (Sec.15 To 17)Documento32 páginasChapter 4 Income From Salaries: (Sec.15 To 17)kiranshingoteAún no hay calificaciones

- EPF For Construction WorkersDocumento10 páginasEPF For Construction WorkersBIJAY KRISHNA DASAún no hay calificaciones

- Process Flow of NominationDocumento2 páginasProcess Flow of NominationMaria ZulfiqarAún no hay calificaciones

- TDS Rates and ReturnsDocumento3 páginasTDS Rates and ReturnsKashishKumarAún no hay calificaciones

- Prerequisites in E-Filing Income Tax Returns: Dr. Kailash KalyaniDocumento62 páginasPrerequisites in E-Filing Income Tax Returns: Dr. Kailash KalyaniRicha KalyaniAún no hay calificaciones

- Central University of South Bihar: Project WorkDocumento17 páginasCentral University of South Bihar: Project WorkPriyaranjan SinghAún no hay calificaciones

- 2017/2018 Year of AssessmentDocumento23 páginas2017/2018 Year of AssessmentSaddhatissa RajawasamAún no hay calificaciones

- GSTDocumento20 páginasGSTSanjaygowda55k100% (2)

- Introduction To Tax Deduction at SourceDocumento9 páginasIntroduction To Tax Deduction at SourceGhanashyam RoyAún no hay calificaciones

- Income Tax2022 GuidelinesDocumento4 páginasIncome Tax2022 GuidelinesSANDEEP SAHUAún no hay calificaciones

- For Tds On SalaryDocumento40 páginasFor Tds On SalarykshitijsaxenaAún no hay calificaciones

- Numpy 1635249967Documento44 páginasNumpy 1635249967cidBookBeeAún no hay calificaciones

- JIRA TutorialDocumento32 páginasJIRA TutorialcidBookBee100% (2)

- 30 BEST DevOps Automation ToolsDocumento27 páginas30 BEST DevOps Automation ToolscidBookBee100% (1)

- SelDocumento4 páginasSelcidBookBeeAún no hay calificaciones

- Python Tutorial For BeginnersDocumento10 páginasPython Tutorial For BeginnerscidBookBee100% (2)

- Instructions For Gathering Required DocumentationDocumento3 páginasInstructions For Gathering Required DocumentationcidBookBeeAún no hay calificaciones

- Frequently Asked QuestionsDocumento2 páginasFrequently Asked QuestionscidBookBeeAún no hay calificaciones

- Links For Document Checklist, Forms & Templates For AffidavitDocumento2 páginasLinks For Document Checklist, Forms & Templates For AffidavitcidBookBeeAún no hay calificaciones

- New Oci Card Application Process For MinorsDocumento4 páginasNew Oci Card Application Process For MinorscidBookBeeAún no hay calificaciones

- NCPre-K Dental Screening Form ENGLISH-3Documento1 páginaNCPre-K Dental Screening Form ENGLISH-3cidBookBeeAún no hay calificaciones

- Conducting A Network Performance Analysis 101: March 24, 2017 1:42pmDocumento16 páginasConducting A Network Performance Analysis 101: March 24, 2017 1:42pmcidBookBeeAún no hay calificaciones

- Role of PT EngineerDocumento153 páginasRole of PT EngineercidBookBeeAún no hay calificaciones

- Loadrunner Testing Cheat Sheet (Version 1.0 - 26/02/2020) : Written by Mark Lilley at Contact: Sales@martkos-It - Co.ukDocumento1 páginaLoadrunner Testing Cheat Sheet (Version 1.0 - 26/02/2020) : Written by Mark Lilley at Contact: Sales@martkos-It - Co.ukcidBookBeeAún no hay calificaciones

- OCT 24, 28, Nov 3 Ginger Ann Dickerson MD: Jeanne A. Rollins, MDDocumento3 páginasOCT 24, 28, Nov 3 Ginger Ann Dickerson MD: Jeanne A. Rollins, MDcidBookBeeAún no hay calificaciones

- Study Guide For The NC DMV Exam: Driver's Handbook DMVDocumento10 páginasStudy Guide For The NC DMV Exam: Driver's Handbook DMVcidBookBee100% (4)

- Zinda Tilismath (Unani Medicine) 100 Herbal and Natural Many Benefits EbayDocumento1 páginaZinda Tilismath (Unani Medicine) 100 Herbal and Natural Many Benefits EbaycidBookBeeAún no hay calificaciones

- PPL Exam Secrets Guide: Aviation Law & Operational ProceduresDe EverandPPL Exam Secrets Guide: Aviation Law & Operational ProceduresCalificación: 4.5 de 5 estrellas4.5/5 (3)

- Drilling Supervisor: Passbooks Study GuideDe EverandDrilling Supervisor: Passbooks Study GuideAún no hay calificaciones

- Note Taking Mastery: How to Supercharge Your Note Taking Skills & Study Like a GeniusDe EverandNote Taking Mastery: How to Supercharge Your Note Taking Skills & Study Like a GeniusCalificación: 3.5 de 5 estrellas3.5/5 (10)

- The Official U.S. Army Survival Guide: Updated Edition: FM 30-05.70 (FM 21-76)De EverandThe Official U.S. Army Survival Guide: Updated Edition: FM 30-05.70 (FM 21-76)Calificación: 4 de 5 estrellas4/5 (1)

- Medical Terminology For Health Professions 4.0: Ultimate Complete Guide to Pass Various Tests Such as the NCLEX, MCAT, PCAT, PAX, CEN (Nursing), EMT (Paramedics), PANCE (Physician Assistants) And Many Others Test Taken by Students in the Medical FieldDe EverandMedical Terminology For Health Professions 4.0: Ultimate Complete Guide to Pass Various Tests Such as the NCLEX, MCAT, PCAT, PAX, CEN (Nursing), EMT (Paramedics), PANCE (Physician Assistants) And Many Others Test Taken by Students in the Medical FieldCalificación: 4.5 de 5 estrellas4.5/5 (2)

- Preclinical Pathology Review 2023: For USMLE Step 1 and COMLEX-USA Level 1De EverandPreclinical Pathology Review 2023: For USMLE Step 1 and COMLEX-USA Level 1Calificación: 5 de 5 estrellas5/5 (1)

- Master the Boards USMLE Step 3 7th Ed.De EverandMaster the Boards USMLE Step 3 7th Ed.Calificación: 4.5 de 5 estrellas4.5/5 (6)

- Nursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASDe EverandNursing School Entrance Exams: HESI A2 / NLN PAX-RN / PSB-RN / RNEE / TEASAún no hay calificaciones

- Outliers by Malcolm Gladwell - Book Summary: The Story of SuccessDe EverandOutliers by Malcolm Gladwell - Book Summary: The Story of SuccessCalificación: 4.5 de 5 estrellas4.5/5 (17)

- Clinical Internal Medicine Review 2023: For USMLE Step 2 CK and COMLEX-USA Level 2De EverandClinical Internal Medicine Review 2023: For USMLE Step 2 CK and COMLEX-USA Level 2Calificación: 3 de 5 estrellas3/5 (1)

- CUNY Proficiency Examination (CPE): Passbooks Study GuideDe EverandCUNY Proficiency Examination (CPE): Passbooks Study GuideAún no hay calificaciones

- NCLEX-RN Exam Prep 2024-2025: 500 NCLEX-RN Test Prep Questions and Answers with ExplanationsDe EverandNCLEX-RN Exam Prep 2024-2025: 500 NCLEX-RN Test Prep Questions and Answers with ExplanationsAún no hay calificaciones

- 2023/2024 ASVAB For Dummies (+ 7 Practice Tests, Flashcards, & Videos Online)De Everand2023/2024 ASVAB For Dummies (+ 7 Practice Tests, Flashcards, & Videos Online)Aún no hay calificaciones

- NCLEX-RN Exam Prep 2024-2025: 500 NCLEX-RN Test Prep Questions and Answers with ExplanationsDe EverandNCLEX-RN Exam Prep 2024-2025: 500 NCLEX-RN Test Prep Questions and Answers with ExplanationsAún no hay calificaciones

- Check Your English Vocabulary for TOEFL: Essential words and phrases to help you maximise your TOEFL scoreDe EverandCheck Your English Vocabulary for TOEFL: Essential words and phrases to help you maximise your TOEFL scoreCalificación: 5 de 5 estrellas5/5 (1)

- Pilot's Handbook of Aeronautical Knowledge (2024): FAA-H-8083-25CDe EverandPilot's Handbook of Aeronautical Knowledge (2024): FAA-H-8083-25CAún no hay calificaciones

- Life Insurance Agent: Passbooks Study GuideDe EverandLife Insurance Agent: Passbooks Study GuideAún no hay calificaciones

- ASVAB Flashcards, Fourth Edition: Up-to-date PracticeDe EverandASVAB Flashcards, Fourth Edition: Up-to-date PracticeAún no hay calificaciones

- LMSW Passing Score: Your Comprehensive Guide to the ASWB Social Work Licensing ExamDe EverandLMSW Passing Score: Your Comprehensive Guide to the ASWB Social Work Licensing ExamCalificación: 5 de 5 estrellas5/5 (1)

- Pass the Bar Exam with Dr. Stipkala's Proven MethodDe EverandPass the Bar Exam with Dr. Stipkala's Proven MethodAún no hay calificaciones

- Certified Professional Coder (CPC): Passbooks Study GuideDe EverandCertified Professional Coder (CPC): Passbooks Study GuideCalificación: 5 de 5 estrellas5/5 (1)

- The Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsDe EverandThe Science of Self-Discipline: The Willpower, Mental Toughness, and Self-Control to Resist Temptation and Achieve Your GoalsCalificación: 4.5 de 5 estrellas4.5/5 (77)