También podría gustarte

- Introduction of Bajaj Allianz Life Insurance CompanyDocumento13 páginasIntroduction of Bajaj Allianz Life Insurance CompanyGirish Lundwani60% (5)

- HDFC Life InsuranceDocumento56 páginasHDFC Life InsuranceSidharth Gera100% (2)

- A Comparative Study of Public Private Life Insurance Companies in IndiaDocumento5 páginasA Comparative Study of Public Private Life Insurance Companies in IndiaAkansha GoyalAún no hay calificaciones

- Project Lic CompleteDocumento49 páginasProject Lic CompleteGaurav93% (44)

- Marketing of Insurance in ICICI Prudential Life InsuranceDocumento89 páginasMarketing of Insurance in ICICI Prudential Life InsuranceksumitkapoorAún no hay calificaciones

- A Comparative Study of Life Insurance and Private CompanyDocumento16 páginasA Comparative Study of Life Insurance and Private CompanyHarshvardhan RathoreAún no hay calificaciones

- A Study On Sbi Life InsuranceDocumento40 páginasA Study On Sbi Life InsuranceprabhuAún no hay calificaciones

- Bodla, B.S. Garge, M.C. Sigh, K.P. (2004) .Insurance FundamentalsDocumento24 páginasBodla, B.S. Garge, M.C. Sigh, K.P. (2004) .Insurance FundamentalsAjith AjithAún no hay calificaciones

- Project On Reliance Life InsuranceDocumento106 páginasProject On Reliance Life InsuranceAmit DwivediAún no hay calificaciones

- Comparative Performance Analysis of Life Insurance Companies EditedDocumento85 páginasComparative Performance Analysis of Life Insurance Companies EditedSumana Sadhukhan0% (1)

- Tata Aia Talreja Edit56Documento63 páginasTata Aia Talreja Edit56ankitverma9716100% (1)

- Competitive Study of LIC Vs Private Players in Life Insurance SectorDocumento89 páginasCompetitive Study of LIC Vs Private Players in Life Insurance Sectordarshit89% (19)

- Mba Insurance Black BookDocumento59 páginasMba Insurance Black BookleanderAún no hay calificaciones

- Insurance Sector of IndiaDocumento66 páginasInsurance Sector of IndiaVijay94% (36)

- Consumer Perceptions of Life Insurance Policies in 2016Documento97 páginasConsumer Perceptions of Life Insurance Policies in 2016Niyati Sandis100% (1)

- Birla Sun Life Insurance Product Portfolio PROJECT ReportDocumento70 páginasBirla Sun Life Insurance Product Portfolio PROJECT Reportkajal nayakAún no hay calificaciones

- Reliance Life Insurence Projected by Sudhakar Chourasiya MaiharDocumento74 páginasReliance Life Insurence Projected by Sudhakar Chourasiya Maihars89udhakar100% (3)

- Birla Sun Life InsuranceDocumento21 páginasBirla Sun Life Insurancecharu100% (3)

- Reliance Life Insurance ReportDocumento116 páginasReliance Life Insurance ReportTimothy Brown100% (1)

- SBI Life Insurance - Market SegmentationDocumento60 páginasSBI Life Insurance - Market SegmentationKshitiz KadamAún no hay calificaciones

- Birla Sun Life Insurance Co. LTDDocumento92 páginasBirla Sun Life Insurance Co. LTDdknigamAún no hay calificaciones

- ICICI Prudential Life InsuranceDocumento21 páginasICICI Prudential Life Insuranceshahin143100% (4)

- Project Synopsis of Insurance CompanyDocumento4 páginasProject Synopsis of Insurance CompanySamar GhorpadeAún no hay calificaciones

- Bharti Axa Life Insurance ProjectDocumento80 páginasBharti Axa Life Insurance ProjectTripti Srivastava100% (1)

- SBI Life SWOT AnalysisDocumento12 páginasSBI Life SWOT AnalysisSantosh ReddyAún no hay calificaciones

- A Comparative Study On The Offerings of Insurance Products Between LICDocumento26 páginasA Comparative Study On The Offerings of Insurance Products Between LICk b paliwal91% (22)

- Insurance Business Environment in India Project ReportDocumento60 páginasInsurance Business Environment in India Project ReportMonil Chheda100% (1)

- Ratio Analysis of LICDocumento31 páginasRatio Analysis of LICpareekkuldeep0% (1)

- A Summer Training Project Report (Reliance Life Insurance)Documento52 páginasA Summer Training Project Report (Reliance Life Insurance)Bhatzada Zahid Jameel100% (3)

- A Study on Awareness Towards Life InsuranceDocumento94 páginasA Study on Awareness Towards Life InsurancekanujkohliAún no hay calificaciones

- Comparing LIC and HDFC Life InsuranceDocumento63 páginasComparing LIC and HDFC Life InsurancePrabhat Kumar MishraAún no hay calificaciones

- Findings: Planning, Risk Coverage and SecuritiesDocumento3 páginasFindings: Planning, Risk Coverage and SecuritiesManish RavatAún no hay calificaciones

- Executive Summary: M.S.R.C.A.S.C BangaloreDocumento72 páginasExecutive Summary: M.S.R.C.A.S.C BangaloreSubramanya Dg100% (2)

- United India Insurance Company LimitedDocumento38 páginasUnited India Insurance Company Limitedshehzanamujawar100% (6)

- Taxation As A Tool For Selling Life Insurance For IDBI Federal Life Insurance Co LTDDocumento33 páginasTaxation As A Tool For Selling Life Insurance For IDBI Federal Life Insurance Co LTDAbhishek Singh0% (1)

- Icici PrudentialDocumento52 páginasIcici PrudentialDeepak DevaniAún no hay calificaciones

- Company Profile of HDFC LifeDocumento19 páginasCompany Profile of HDFC LifeNazir HussainAún no hay calificaciones

- Project On Bajaj AllianzDocumento70 páginasProject On Bajaj AllianzRanjeet Rajput100% (1)

- SBI Life InsuranceDocumento38 páginasSBI Life InsuranceParth Bhatt50% (2)

- The Conceptual Framework For Indian Insurance IndustryDocumento12 páginasThe Conceptual Framework For Indian Insurance IndustryAbdul Lathif100% (3)

- SbiDocumento55 páginasSbiJaiHanumankiAún no hay calificaciones

- A Project Report On ICICI Prudential Life InsuranceDocumento37 páginasA Project Report On ICICI Prudential Life InsuranceSudha Sandesh Ambekar86% (42)

- Shriram Life InsuranceDocumento31 páginasShriram Life Insurancebhagyashree mohantyAún no hay calificaciones

- A Project Report On Group InsuranceDocumento64 páginasA Project Report On Group Insurancesharinair1393% (15)

- Literature Review (MP)Documento4 páginasLiterature Review (MP)himanshiAún no hay calificaciones

- Project On ULIPDocumento22 páginasProject On ULIPDhaval Lagwankar88% (17)

- Summer Internship Project in Idbi Fedral Life InsuranceDocumento83 páginasSummer Internship Project in Idbi Fedral Life InsuranceHibah Wasif87% (15)

- Role of LIC in Indian InsuranceDocumento61 páginasRole of LIC in Indian Insurancenikita950100% (2)

- Comparative Study of Services Provided by LIC & ICICI Prudential Life InsuranceDocumento34 páginasComparative Study of Services Provided by LIC & ICICI Prudential Life Insurancegagansihala20100% (19)

- Reliance Life Insurance, Koppal: Savings & Investment PlansDocumento70 páginasReliance Life Insurance, Koppal: Savings & Investment PlansPrasanth KumarAún no hay calificaciones

- Presentation 1mmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmDocumento13 páginasPresentation 1mmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmmdeyajitavaAún no hay calificaciones

- Investor Behavior Toward Reliance Life Insurance Child PlanDocumento46 páginasInvestor Behavior Toward Reliance Life Insurance Child PlandeyajitavaAún no hay calificaciones

- Reliance Life Insurance's Journey and AchievementsDocumento7 páginasReliance Life Insurance's Journey and AchievementsPrasanth KumarAún no hay calificaciones

- Reliance Life InsuranceDocumento9 páginasReliance Life InsuranceSwarnadeep SahaAún no hay calificaciones

- Our Founder Reliance InfoDocumento22 páginasOur Founder Reliance Infosagar09Aún no hay calificaciones

- What Is A Pension?: Introduction To Pension PlanDocumento18 páginasWhat Is A Pension?: Introduction To Pension PlanMahesh SatapathyAún no hay calificaciones

- Reliance Life Insurance Products GuideDocumento3 páginasReliance Life Insurance Products GuideAditi ThakurAún no hay calificaciones

- A Survey Report On Consumer Buying Behaviour: Submitted To, MR - Bhavik Shah (Vnsgu)Documento28 páginasA Survey Report On Consumer Buying Behaviour: Submitted To, MR - Bhavik Shah (Vnsgu)Dipak BagsariyaAún no hay calificaciones

- Reliance Life InsuranceDocumento14 páginasReliance Life InsuranceVaibhav MittalAún no hay calificaciones

- Simple Employment ContractDocumento3 páginasSimple Employment ContractJaime Miguel III SantosAún no hay calificaciones

- Matter of Philadelphia Penn Worsted Company, Bankrupt Barney Cramer and Harvey Mencoff, Copartners Trading As Advanced Textile Company, AppellantsDocumento6 páginasMatter of Philadelphia Penn Worsted Company, Bankrupt Barney Cramer and Harvey Mencoff, Copartners Trading As Advanced Textile Company, AppellantsScribd Government DocsAún no hay calificaciones

- 064 Cabarroguis Vs VicenteDocumento2 páginas064 Cabarroguis Vs VicenterbAún no hay calificaciones

- Wheatland Nipple, Elbow& CouplingDocumento9 páginasWheatland Nipple, Elbow& CouplingJaaffer AliAún no hay calificaciones

- Rights and Duties of AgentsDocumento12 páginasRights and Duties of AgentsSejal JainAún no hay calificaciones

- Standar Kontrak Dalam Perspektif Hukum PerlindungaDocumento12 páginasStandar Kontrak Dalam Perspektif Hukum PerlindungaStudent 01Aún no hay calificaciones

- Non Compete Non Disclosure AgreementDocumento2 páginasNon Compete Non Disclosure AgreementJeff Pan100% (4)

- Quiz-No 7Documento5 páginasQuiz-No 7Shiela RengelAún no hay calificaciones

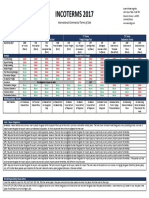

- Incoterms 2017Documento1 páginaIncoterms 2017iogenrAún no hay calificaciones

- Basic Principles of Patent LawDocumento17 páginasBasic Principles of Patent LawTania MajumderAún no hay calificaciones

- Effects of Conditions Precedent in Building ContractsDocumento5 páginasEffects of Conditions Precedent in Building ContractsPameswaraAún no hay calificaciones

- PFRS 17 Insurance Contracts SummaryDocumento32 páginasPFRS 17 Insurance Contracts SummaryVictoria CadizAún no hay calificaciones

- Casualty Insurance NotesDocumento2 páginasCasualty Insurance NotesPauline DgmAún no hay calificaciones

- Secretary's Certificate (AUB)Documento1 páginaSecretary's Certificate (AUB)Gerard Nelson ManaloAún no hay calificaciones

- Tanzania Revenue Authority: Institute of Tax AdministrationDocumento28 páginasTanzania Revenue Authority: Institute of Tax AdministrationMoud KhalfaniAún no hay calificaciones

- Copyright Is A Bundle of RightsDocumento22 páginasCopyright Is A Bundle of RightsMG MaheshBabuAún no hay calificaciones

- Contract Law by A. MatanzaDocumento38 páginasContract Law by A. MatanzaKELVIN A JOHNAún no hay calificaciones

- Model Limited Liability Partnership AgreementDocumento5 páginasModel Limited Liability Partnership AgreementnavinkapilAún no hay calificaciones

- Massachusetts Retainer Agreement 2021-05-11Documento5 páginasMassachusetts Retainer Agreement 2021-05-11Thomas KeelerAún no hay calificaciones

- Benefit Illustration: UIN: 104N118V05 Page 1 of 3Documento3 páginasBenefit Illustration: UIN: 104N118V05 Page 1 of 3Mahesh GediyaAún no hay calificaciones

- Digest Vda de Sindayen V InsularDocumento3 páginasDigest Vda de Sindayen V InsularJannaTolentino0% (1)

- NR12A - ICC Build Target Cost V4.2Documento98 páginasNR12A - ICC Build Target Cost V4.2David WoodhouseAún no hay calificaciones

- Siguan V Lim Case DigestDocumento2 páginasSiguan V Lim Case DigestTivorshio Macabodbod100% (1)

- A. Barque Quilpue LTD V Brown (1904) 2 KB 261Documento2 páginasA. Barque Quilpue LTD V Brown (1904) 2 KB 261Mohamad Faes Bin RosliAún no hay calificaciones

- Motion To Withdraw Petition For ForeclosureDocumento2 páginasMotion To Withdraw Petition For ForeclosureParis Asir100% (2)

- IRDAI Annual Report 2019-20 - ICR - Health - InsurersDocumento1 páginaIRDAI Annual Report 2019-20 - ICR - Health - InsurerslesayAún no hay calificaciones

- (CD) Phoenix Vs United States Lines - GR No L - 24033Documento2 páginas(CD) Phoenix Vs United States Lines - GR No L - 24033The Concerned Lawstudent0% (2)

- Consumer Protection of Product Warranties in Business LawDocumento8 páginasConsumer Protection of Product Warranties in Business LawJoshua LimbongAún no hay calificaciones

- Securities Regulation Outline #1Documento50 páginasSecurities Regulation Outline #1tuyaAún no hay calificaciones

- Hizon Notes - Partnership, Lease and PrescriptionDocumento82 páginasHizon Notes - Partnership, Lease and Prescriptionnikkimaxinevaldez100% (1)